No doubt about it: at some point we’re neither semi-retired, findependent or fully retired. We’re out there in a retirement community or retirement home, and maybe for a few years near the end of this incarnation, some time to reflect on it all in a nursing home. Our Longevity & Aging category features our own unique blog posts, as well as blog feeds from Mark Venning’s ChangeRangers.com and other experts.

MoneySense.ca: Photo created by senivpetro – www.freepik.com

My latest MoneySense Retired Money column has just been published and looks at CPP survivorship issues. Tucked in there I reveal for the first time my personal decision to take the Canada Pension Plan at age 66, which I did last summer a few months after reaching that

It was more of a cash flow issue in light of the fact that just prior to this, my wife had left her full-time and well-paid job in the transportation industry. But I mention another consideration: the quirky CPP survivorship rules. Now I realize most couples in their 60s don’t dwell on our mortality much if they are in good health and keep care of themselves. And bear in mind my decision was long before the Coronavirus pandemic, which disproportionately affects seniors.

Normally, those ready to retire contact Service Canada to get a record of past CPP contributions. They send you benefit estimates (both for CPP and OAS) some months before you turn 65 but you can also obtain this information before or after by visiting Canada.ca. There you can find a CPP/OAS calculator provided by Ottawa, providing an estimate of expected sources of income.

Doug Runchey and David Field team up on a new CPP calculator

While OAS is straightforward, optimizing CPP is surprisingly complicated, so much so that Doug Runchey (one of the country’s preeminent experts on both programs) provides calculation services to help individuals make optimal decisions on timing the start of benefits. Runchey used to be at Service Canada, so is intimately familiar with the ins and outs of the timing of receipt of these programs. Continue Reading…

Empty park benches… waiting for YOU to fill them up!

By Billy and Akaisha Kaderli, RetireEarlyLifestyle.com

Special to the Financial Independence Hub

I’m a little troubled.

Twice now in the last year, two friends of almost four decades have confided in me that they no longer have an interest in making new friendships. The man said “It’s too much work” and the other, a woman, said she is “without enthusiasm or desire for it.”

Couple that with the fact that my friends and I are all proceeding to the milestone age of 70.

Articles abound on how loneliness is an epidemic and adds to our health problems. Loneliness feeds on itself creating terrible self-talk (what do I have to offer? What would I talk about, anyway? It’s not safe to express an opinion, and besides I’m not up on the news …) that keeps us housebound.

A recent article about a study in the UK says hundreds of thousands of people often go a week without speaking to a single person. Nearly half of all the seniors interviewed said they’d feel more confident to head out each day if they knew their neighbors. This begs the question … why don’t we know our neighbours?

Why aren’t we looking into the eyes of people we live next to and giving them a smile? Or talking about the roses in their gardens, or the pup they walk daily?

Are we just so afraid of each other that we cannot afford to make small talk anymore? I have lived outside the US for many years now, and forgive me for asking … But is this chatting up a stranger considered impolite these days? Or hazardous?

Two more first-hand experiences

Some years back I witnessed two of my relatives in curious circumstances. One elderly aunt said “I don’t need any more friends. I have my husband, my church group, children and grandchildren. Why would I need more?”

To myself I responded “Do we have so many friends that we can’t squeeze in another one? Someone who can make us laugh, or teach us something? Who in the world has too many friends?”

Another elderly relative, on the way to breakfast after church, had a well-dressed gentleman say hello to her and something about “what a nice day it was” — and she was aghast.

She responded, “Do I know you? Why are you talking to me?”

To me this situation was incomprehensible. It seemed obvious that the man meant no harm and he was actually on the way to his car in the restaurant parking lot – right where we were – after finishing his morning meal.

Heads up here

If loneliness is the epidemic disaster that health studies say it is, then maybe we could prepare for this ahead of time.

Ask yourself how might we be part of our own problem here? Or if you are inclined to take action, I have a couple of suggestions below which you might find useful. Continue Reading…

Most of us have been given medical advice to eat healthier and get regular exercise, and there are certainly daily benefits to these choices, like feeling more energetic, having a better mood, and experiencing less pain. But we don’t always consider the financial benefits of a healthier lifestyle.

Although spending more money upfront on things like organic food and gym memberships or other fitness activities might seem like it doesn’t fit into a frugal financial lifestyle, the money you’ll save both in your monthly spending and in the long run makes the initial costs well worth it.

1.) Cheaper insurance later in life

When you get older, you may need life or burial insurance (if you don’t have it already), and being healthy will help you get better rates for your policy. Living in an unhealthy way may lead to health problems down the line. Although it’s still possible to get it, it can be more difficult to get funeral insurance for pre-existing conditions (also known as “final expense” and “burial” insurance). For instance, if smokers need insurance, but they now have lung cancer, it may be hard for them to find a policy, and if they do, it may cost them more.

2.) Lower health care costs

Health care companies often charge higher premiums for people with pre-existing conditions or chronic health problems such as hypertension and diabetes, and sometimes also for smokers. Beyond that, if you have a chronic health condition, you’ll need to pay more out of pocket for prescriptions, doctor visits, and medical treatments. While not all such conditions are preventable through healthy living, many common ones — diabetes, heart disease, certain types of cancers, and osteoporotic hip fractures, to name a few — are.

The World Health Organization found that “physically active individuals in the USA save an estimated $500 per year in health care costs.” That’s based on data from 20 years ago, so savings are even higher today.

unsplash

3.) Less spending on filler foods

Choosing whole foods over packaged, processed foods like chips and other snacks means you’re getting more nutrition for your dollars. Changing your snacking habits can help you do this. And adjusting portion sizes to meet what your own body needs will also help shave down your spending on food.

What’s more, cutting out other indulgences many people regularly consume, such as tobacco and alcohol, will save money each year that you can redirect to retirement savings or other investments. Healthier eating habits and reduced substance use will affect your budget now, and your health care costs later. Continue Reading…

The following is a guest post by financial planner, author and pension expert Alexandra Macqueen, which originally ran on Dale Roberts’ Cutthecrapinvesting blog on Feb. 26, 2020. Because they both consider it such an important subject, they have given us permission to re-publish on the Hub. While an overview, it can serve as the ultimate guide to defined benefit pension planning. And mostly, Alexandra outlines the pitfalls and the importance of finding a true and qualified pension expert.

By Alexandra Macqueen, CFP

Special to the Financial Independence Hub

If you’re a Canadian facing a decision about staying in or leaving your defined-benefit pension plan, it might be one of the highest-stakes choices you’ll ever make: the amounts you’re considering can be high – worth as much as your house, or even more – the timeline short, the tax consequences significant, the details complex, and the outcome irreversible.

Over the course of my financial planning career, I’ve encountered, unfortunately, more than one pension decision gone wrong. Just how many ways can a pension decision go off the rails? Here are five “pension pitfalls,” drawn from real-live cases that have crossed my desk in the last year or so, along with the lessons Canadians who are facing this decision can glean.

Pitfall Number 1: Unbalanced advice

It is widely understood that defined-benefit pension plans cover what’s called, in the financial planning world, “longevity risk” – or the chance of living longer, even much longer, than you expect. Defined-benefit pension plans protect against the risk of living very long by providing lifetime income.

In exchange for covering off this risk, however, if you die sooner than expected, the pension payments may stop (depending on whether you have a surviving spouse or other beneficiary, and whether your plan provides guaranteed payments for a specified term).

Image by Gerd Altmann from Pixabay

One of the most misleading financial plans I ever encountered – it was just one page, and written in Comic Sans font – outlined the “pros and cons” of staying in a defined-benefit plan. Under “cons,” the planner had listed “mortality risk,” which they defined as the risk of dying relatively shortly after starting to receive monthly pension income.

Here’s what they meant by “mortality risk:” Let’s say you’re facing a pension decision between, say, receiving a lump sum of $750,000 if you “commuted” your entitlement under the plan today, versus $3,500 per month for as long as you’re alive – and you’re wondering about what happens if you die a few years after starting the pension. (“Commuting” your pension entitlement means taking the assets out of the plan as a lump sum today, typically to manage on your own.)

In this situation, and with “mortality risk” presented by the advisor in this way – as equally balanced with the probability of living a long time – it can be very tempting to think that the best option is to “take your money and run.” Maybe you’ll die “early,” you might think – and if you do, you’ll leave an estate!

However, this “financial plan” simply listed “pros and cons” of staying in the defined-benefit plan, without considering the probability of either outcome. If we use the projection assumptions provided for Certified Financial Planners® to reference in preparing financial plans, we can see that a woman aged 65 today has a 50% chance of living to age 91, and a 25% chance of living to age 97, while a man aged 65 today has a 50% chance of living to age 89, and a 25% chance of living to age 91 (see page 13 of the linked document).

Longevity risk vs mortality risk.

Instead of this guidance, however, in this plan the chance of “living” (longevity risk) and “dying” (mortality risk, although you won’t be able find anyone else using this term in the way this advisor did) were presented as equally-weighted possibilities, with no discussion of the likelihood of living to an advanced age.

While a discussion of the impact of dying “early” on pension outcomes is appropriate, this probability should be contextualized – not simply listed as a “con” of staying in a defined-benefit plan, and implicitly characterized as “just as likely” as living to an advanced age.

Pitfall Number 2: Inexpert advice

In this case, a member of a “gold-plated” pension plan (think large sponsoring organization and top-of-the-line pension plan features, such as inflation protection) was going through a divorce, and needed to find a way to equalize assets with a soon-to-be-ex-spouse.

As is not unusual for members of defined-benefit pension plans, the member didn’t have significant other assets. In order to meet his financial obligations, and guided by a financial advisor, he decided to commute his plan entitlement and use the freed-up cash to make an “equalization payment” to his ex.

Unfortunately, neither he nor the advisor really understood the tax consequences of this choice. Because of the size of the plan’s commuted value, the client was unable to shelter much of the paid-out lump sum from immediate taxation, meaning he had a very significant tax bill when tax time rolled around. (That’s because the amount of the commuted value was well in excess of the Maximum Transfer Value set by the Income Tax Act, which specifies how much of that commuted value can be sheltered from immediate taxation.) Continue Reading…

What is Coronavirus and why is it so scary for life insurers?

The entire insurance business is based on risks and the ability to evaluate them. At the same time, life insurance companies do not like situations where they do not have enough information and statistics about risks related to their potential customers. People who have or had Coronavirus (also called COVID-19) represent this case.

The current outbreak of Coronavirus has already infected over 70,000 worldwide resulting, so far, in over 1,800 deaths. The majority of cases are taking place in China. Nevertheless, it has already spread across more than 25 other countries and is growing. The world’s knowledge about this virus is still fairly limited, including very approximate data about its death rate and the ways it spreads. Currently there is no vaccine. The current estimations put COVID-19’s death rate at approximately 3% as per GlobalNews. Comparatively, the death rate of SARS (outbreak in 2003) was placed at 9.6% and the death rate of Ebola (also known as EVD – Ebola Virus Disease) varied from 25% to 90% with the average values at 50% as per the World Health Organization.

All this leaves life insurance companies with a lot of uncertainty on how to deal with current and past Coronavirus patients. We reached out to a number of Canadian insurers to understand how they would treat such cases.

Insurance companies are all about managing risk

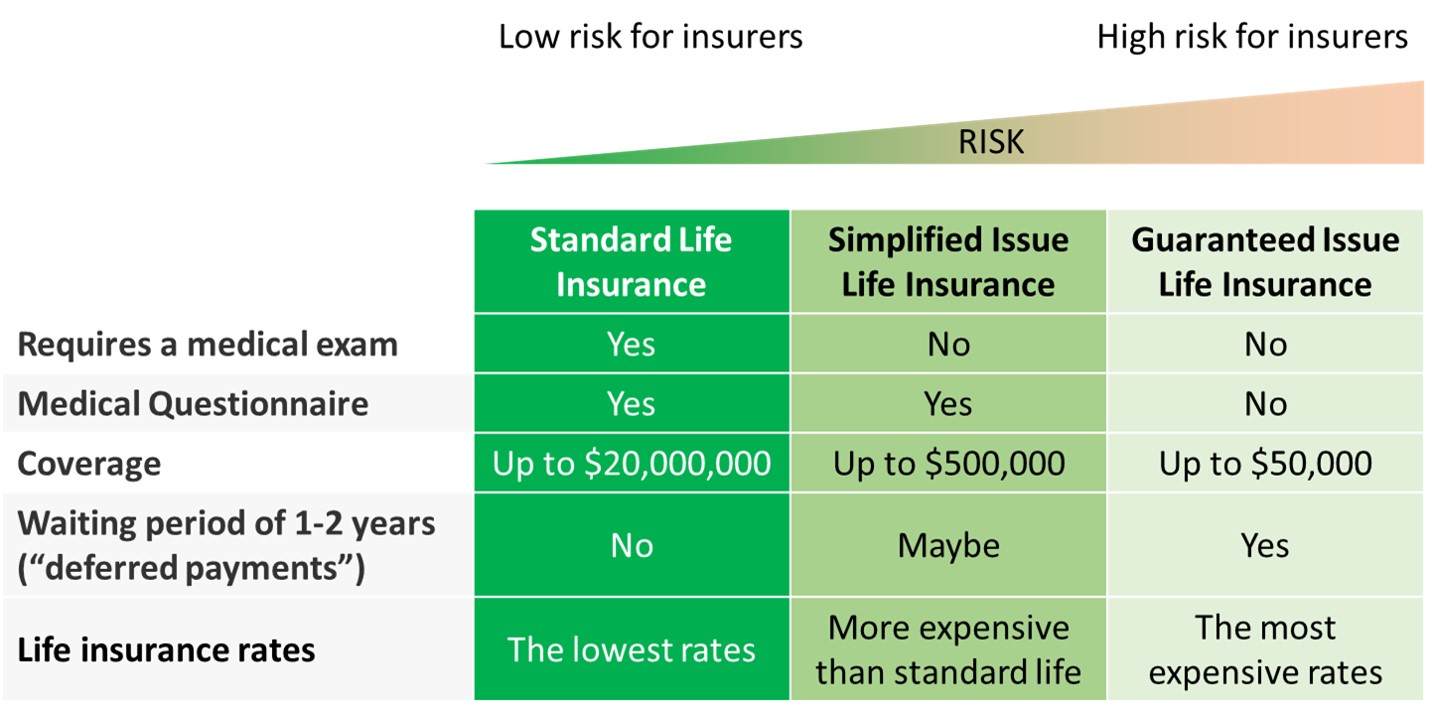

Insurance companies are all about managing risks and ensuring that they collect revenue in order to run their business and pay for claims. Insurers do this through defining various levels of life insurance products associated with different levels of risk. An overview below shows key products with their key characteristics.

In a nutshell, standard life insurance is associated with low risks, comes with the highest coverage limits, but REQUIRES both a detailed medical exam and completion of a medical questionnaire.

Simplified life insurance comes WITHOUT medical exams (which makes it very attractive for some people) but WITH a short, medical questionnaire. It comes at a cost and coverage limits are lower than standard life insurance.

Guaranteed life insurance DOES NOT require medical exams NOR a medical questionnaire. It is a life insurance product that you can always buy, but it comes at much higher costs, with limited coverage, and extra clauses not providing any coverage if an applicant passes away in the first two years after purchasing the policy.

Two last life insurance types are also called no medical life insurance since they do not require a medical exam. They are increasingly popular among seniors and people with health conditions.

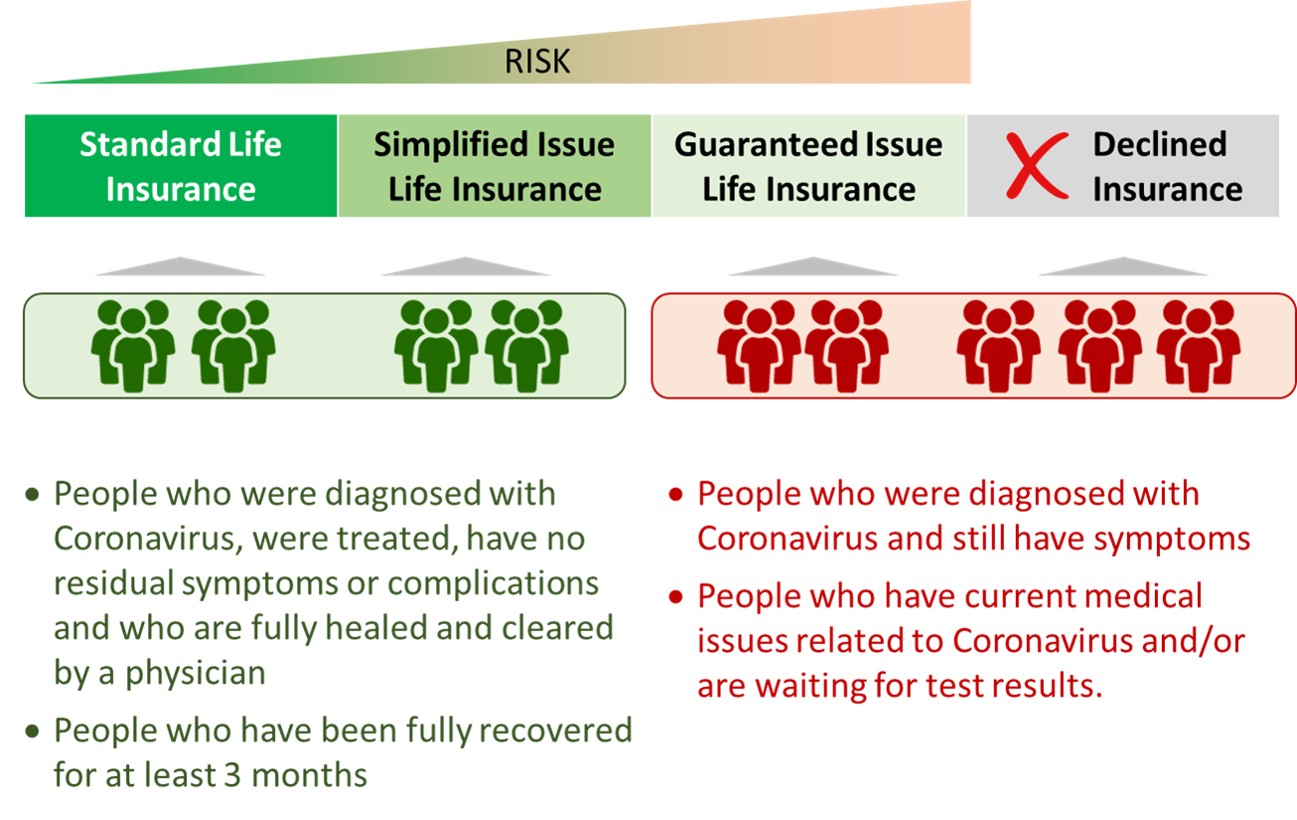

How do insurance companies treat people with Coronavirus?

Our inquiries to various insurance specialists showed that there are two groups of insurers:

Those who do not have a defined approach of dealing with Coronavirus and

Those who are able to share the exact conditions under which people with Coronavirus will be able to get life insurance.

The first group of insurers would either decline your application or delay it until a clear course of action is defined or offer you only guaranteed issue life insurance.

The second group of insurers will be able to offer you a standard life insurance policy, but only once you are within defined parameters which are:

• 3 months have passed since full recovery OR

• Fully healed and cleared by a physician after being diagnosed with Coronavirus

An overview below illustrates this concept:

What exactly do the insurers say if they are not ready to provide insurance?

The first group of insurers who are not open to providing life insurance for Coronavirus patients say: