By Stephen Dover, CFA, Franklin Templeton Institute

(Sponsor Blog)

Any consideration of emerging markets must begin with the case for global investment strategy. The decision to allocate capital internationally is not just about geographic diversification. Rather, it is increasingly driven by fundamental shifts in absolute and relative returns that drive global capital flows, by the discovery of new investment opportunities, and by the need to identify and manage concentration risk.

This section establishes the reasons why active international allocation strengthens institutional portfolios that also reinforces the rationale for emerging market allocations.

In an extended period of “US exceptionalism”—roughly spanning the 15 years from the global financial crisis to the middle of the current decade — investors increasingly gravitated to US equity and credit markets. That was understandable, given the superior returns — in absolute and risk-adjusted terms — delivered by US financial assets.

Importantly, superior returns on US assets were driven by superior fundamentals, including growth, institutional solidity, vast market liquidity, innovation and historic levels of profitability.

At the same time, however, US-based equity returns became more concentrated, as mega-

capitalization stocks accounted for a growing share of widely followed market-capitalization indexes.

Partly driven by concerns about concentration risk and partly because of improving returns in other

markets, investors have more recently begun to look for opportunities in other markets.

Over the past year, European, Japanese and emerging equities, and particularly emerging debt, have episodically produced superior returns to those found in US equity and fixed income markets. Those outcomes have begun to raise awareness of global opportunities, among them in emerging markets.

Renewed interest in global investing stems from other factors as well. Economic and monetary policy

divergence is becoming more significant. Prior to the US-Iran War, the Federal Reserve (Fed) was

biased to cut rates, the European Central Bank (ECB) had paused its easing cycle, the Bank of Japan

(BoJ) had already cautiously begun to hike rates, and various emerging central banks were prepared

to cut rates amid falling inflation. Those divergences in policies had contributed to a weakening of

the US dollar since early 2025, which in turn boosted investor interest in non-US markets, including

in emerging markets.

With the outbreak of the war and the impairment of shipping via the Strait of Hormuz, policy

perceptions have again shifted. The Fed and emerging central banks are now (mostly) on hold, the

ECB and the BoJ are inclined to tighten their monetary policies. Unsurprisingly, volatility, correlation

and returns have shifted markedly.

But the underlying point remains: Divergence in the conduct of monetary policy creates opportunity for tactical re-allocation. And it isn’t just about monetary policy. In many respects, fiscal policy divergence is even more notable.

In the United States, large structural budget deficits are forecasted over the next decade.

Meanwhile, Japan’s new government is promising more fiscal stimulus as well. So, too, are Germany and the European Union.

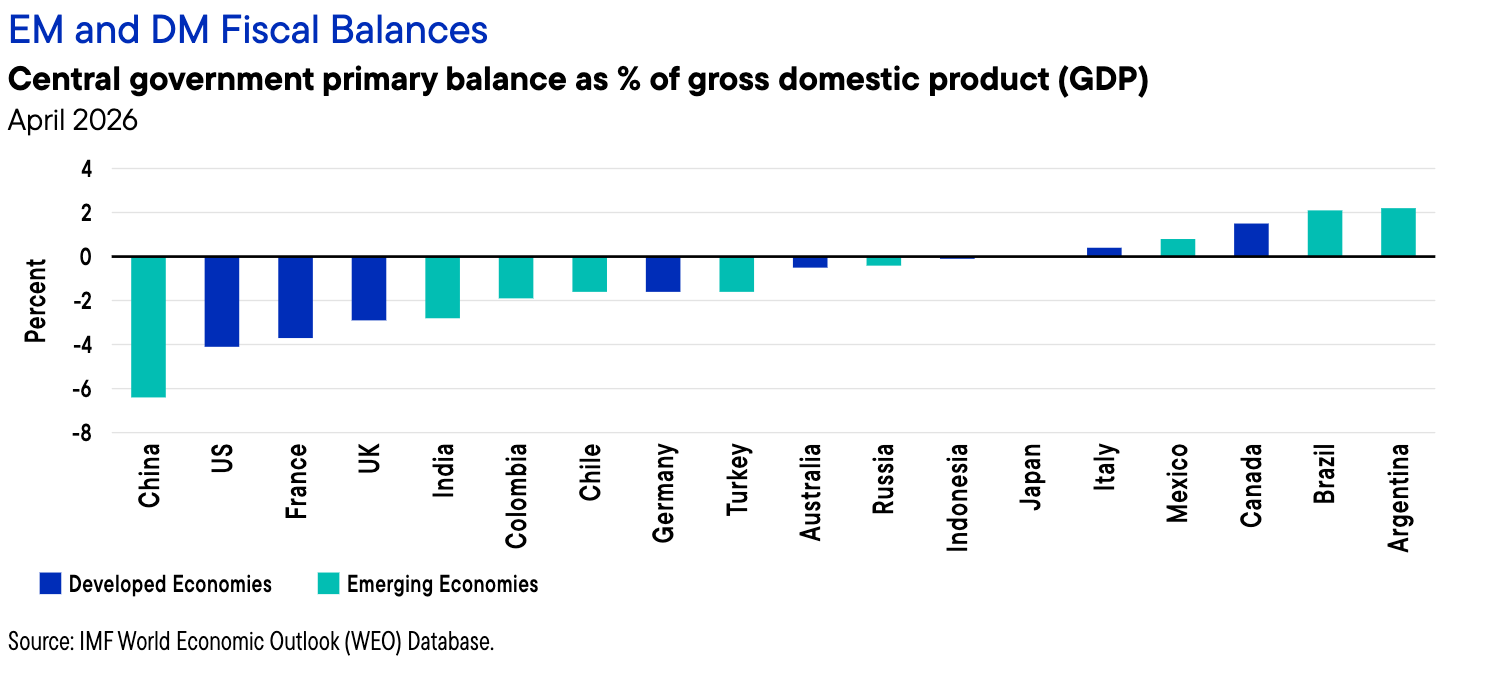

In contrast, over the past decade many emerging countries have been pursuing more disciplined,

orthodox fiscal policies, with the upshot that their sovereign credit fundamentals are improving in

absolute and relative terms. That trend lends support to secular declines in risk premia and should

manifest in even lower nominal and real interest rates, as well as stronger emerging currencies.

Directly, that boosts emerging debt returns, but it also lends greater resilience to many parts of the

emerging complex.

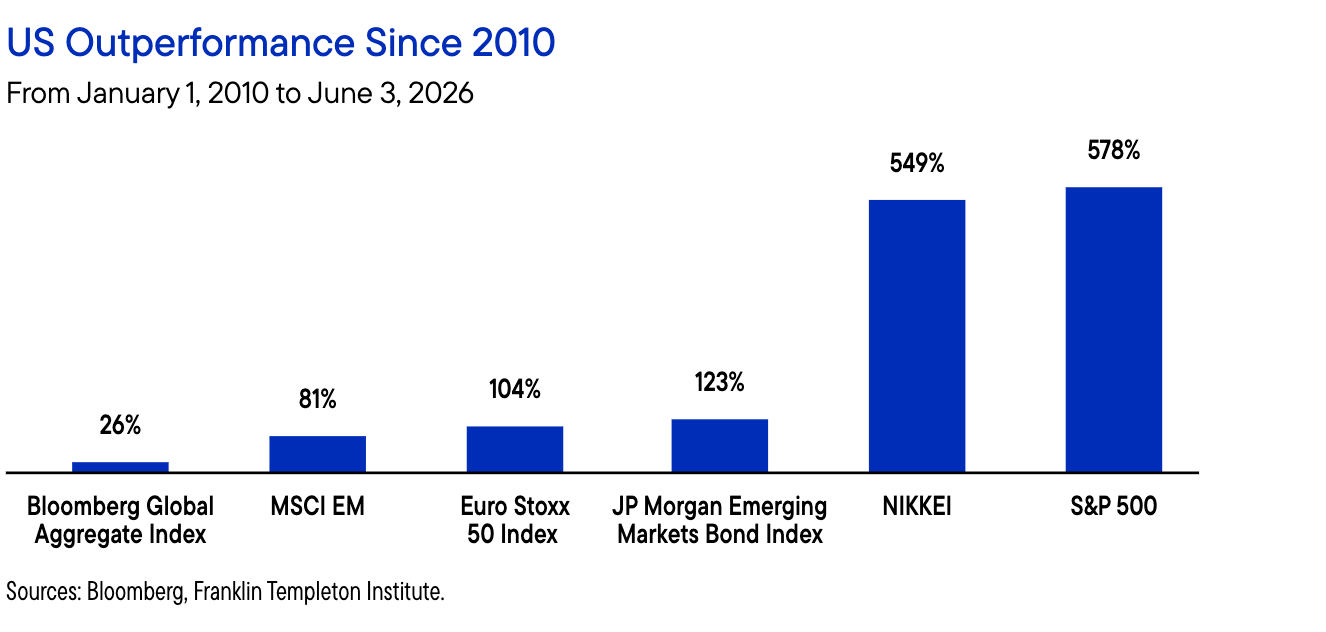

As noted, global markets — including emerging markets — have recently exhibited episodes of

outperformance relative to US equity and fixed income returns. That is important, because for most of

the past 15 years US exceptionalism has been dominant. So much so, indeed, that if one compares the

efficient frontiers of investing with and without emerging markets since 2010, it is clear emerging

market allocations had almost no positive impact on portfolio returns, adjusted for risk, over the past 15

years.

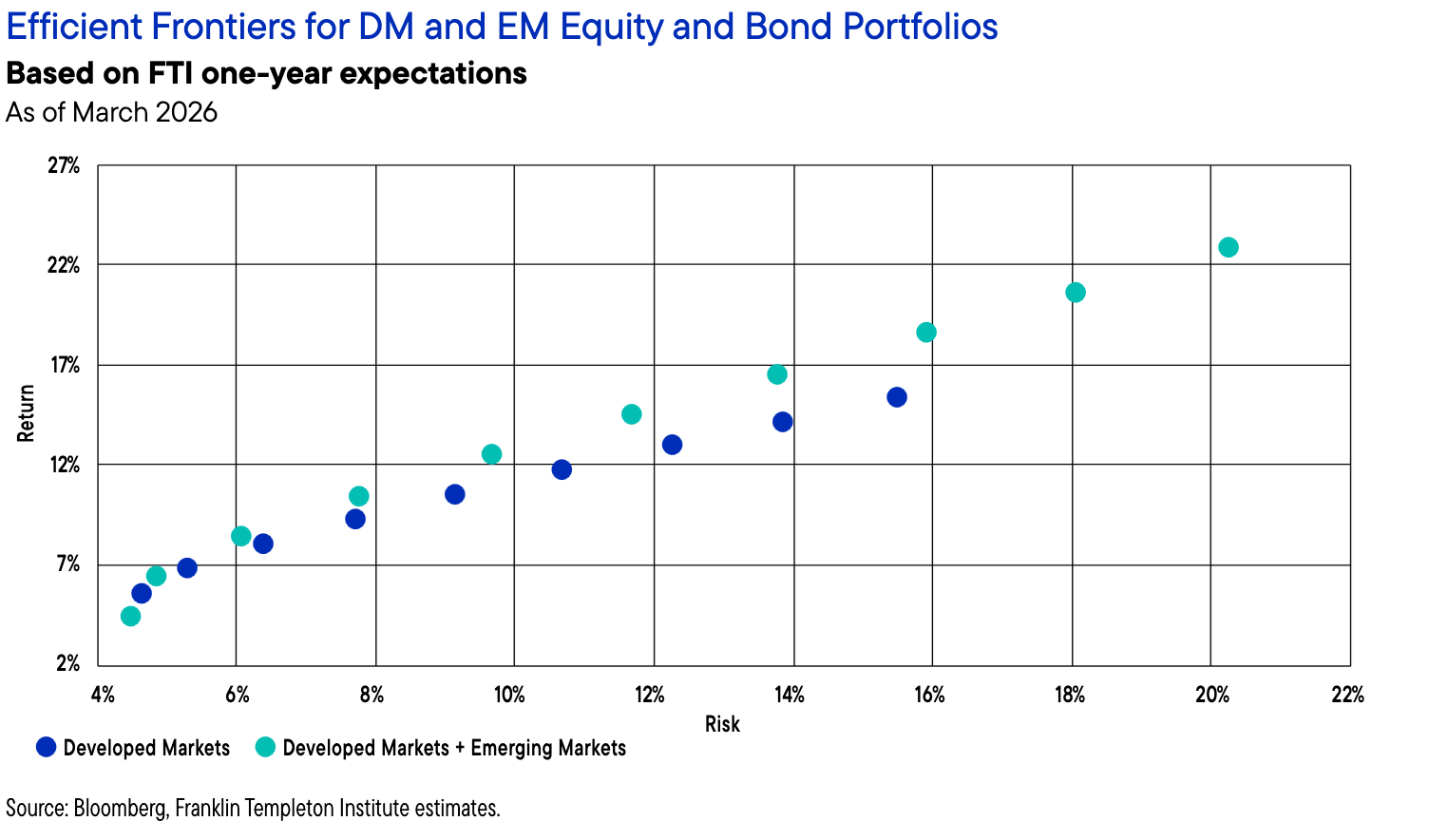

But we believe those historic results are not likely to persist. Owing to improving emerging market

fundamentals, which we describe in detail in the next section of this paper, absolute and relative

expected returns are shifting in their favor. Using our estimated year-ahead returns across all

markets — developed and emerging, public equity and debt — a clear upward and leftward shift in the

efficient frontier is apparent when comparing a developed market only to a blended emerging and

developed portfolio. We believe emerging markets (alongside other non-US developed markets) are

therefore poised to contribute to improved portfolio performance in the year ahead: and most

probably for longer.

EMs are undergoing a profound transformation, one that is not cyclical in nature but structural, durable and increasingly self-reinforcing. The traditional narrative of emerging markets as externally dependent, volatility-prone economies is being reshaped by a new set of underlying forces that are redefining their role in the global economy.

EMs have generally shown significant resilience this decade, facing down a series of shocks arising from the COVID-19 pandemic, the inflationary outcome of the Russia-Ukraine war and the US Fed’s sharp interest-rate hikes during 2022-2023, and last year’s substantial tariff volatility. Not only did EMs survive this period, but many have thrived.

As world trade reconfigures and global actors realign geopolitically, EMs have found themselves generally well-placed to benefit from these global shifts: including some that are likely to benefit under the new tariff regime. This compares to earlier years when EMs would often face crises (whether debt, balance of payments and/or in banking systems) from global shocks.

The fact that EMs are in a favorable position now is largely a result of policy choices that have situated them handsomely to face a rapidly changing world economy. In this regard, we note three significant global regime changes that we believe EMs are now well-placed to benefit from: structural improvements in EMs, global trade econfiguration, and a shift in the US dollar’s ability to attract global capital inflows.

Regime change: EMs are structurally sounder

Policy responses with respect to both monetary and fiscal policy have improved significantly across EMs over the past couple of decades. Adoption of sound, credible policies and nurturing of institutions (such as inflation targets, fiscal rules and independent central banks) have helped policy formulation and improved the market’s perception of the credibility of EM policymakers. Continue Reading…