For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

On Wednesday, August 21, 2024, Harvest ETFs introduced another innovative product in its growing lineup: Harvest High Income Shares ETFs.

These single-stock ETFs invest in top, well-favoured U.S. stocks, with a focus to provide high income every month from covered call writing.

The Top U.S. Stocks in Scope

Eli Lilly. A dominant global pharmaceutical manufacturer and distributor.

Amazon. A global e-commerce giant that has established a massive logistics network and an innovator in enterprise cloud computing.

Microsoft. A global leader in software services and solutions, as well as hardware technology.

NVIDIA. Established as a huge force in the semiconductor industry, with its graphics processing units (GPUs) at the forefront of the AI revolution.

These U.S. stocks are well known and sought after. They are four of the largest and most widely held stocks in today’s market. They offer a significant building block for covered call writing strategy, in that the shares of these massive companies have very deep and liquid option markets. Further, the level of volatility that accompanies the share prices is high. That makes these great stocks for Harvest’s active and flexible covered call writing strategy.

The Harvest Process: Strong focus on High and Reliable Income every month

Record matters, and Harvest has it. For 15 years and counting, Harvest has pursued an active covered call writing strategy focused on generating high income, every month for investors in its Income ETFs lineup. Supported by its proven covered call strategy, Harvest has delivered nearly $1 billion in total monthly cash distributions over its 15-year history to investors.

This new, innovative product line, focuses on investing in shares of a single company targeting the largest, most widely held U.S. stocks. Harvest’s investment team — with a combined six decades of investment experience — will use Harvest’s well-established covered call writing strategy to provide high monthly income to investors while delivering on what sets Harvest apart; that is, ensuring that investors enjoy not just high, but consistent, stable, predictable, and reliable income each month.

The premium income from covered call writing can be treated as capital gains. That means the high income that the Harvest High Income Shares ETFs seek to provide can be regarded as being among most tax-efficient income. The Harvest High Income Shares ETFs are organized as Canadian Trust Units and are available in Canadian and U.S.-dollar-denominated Units. As open-end mutual funds listed on an exchange (“ETFs”), on the TSX, they provide trading and reporting flexibility for Canadian investors.

Innovation, High Monthly Income, and Upside

The covered calls strategy used in the Harvest High Income Shares ETFs will operate with up to 50% write level. Harvest’s portfolio management team has stress tested these equities with an average 2-year implied volatility. It found they can produce high levels of income at much lower write levels. Therefore, a 50% write level, in their view, provides a conservative floor to ensure unitholders will be able have reliable high-income generation every month. Continue Reading…

* Republished from the Just Word Blog from Robin Powell, the U.K.-based editor of The Evidence-Based investor and consultant to investors, planners & advisors

There are broadly two types of investing: active and passive investing. Active investors try to beat the market by trading the right securities at the right times. Passive investors simply try to capture the market return, cheaply and efficiently. So which approach is better?

Instinctively, most people who haven’t looked into the issue in any detail tend to assume that active investing is superior. After all, the thinking goes, it’s surely preferable to be doing something to improve your investment performance, instead of just accepting whatever return the market offers. Active investing has certainly been much more popular than passive in the past.

But if you look at the evidence, you’ll see that over the long run, most mutual fund managers have underperformed passively managed funds.

S&P Dow Jones Indices keeps a running scorecard of active fund performance in different countries, including Canada, called SPIVA. It consistently shows that, regardless of whether they invest in equities or bonds, most active managers underperform for most of the time.

The latest SPIVA data for Canada were released a few weeks ago, and they chart the performance of active funds up to the end of December 2023. What the figures show is that the great majority of funds have lagged the relative index once fees and charges are factored in, especially over longer periods of time.

Underperformance over ten years is even more pronounced. For example, 98.04% of Canadian Focused Equity funds, 97.56% of U.S. Equity funds and 97.60% of Global Equity funds underperformed the benchmark. Remarkably, on a properly risk-adjusted basis, not a single U.S. Equity fund domiciled in Canada beat the S&P 500 index over the ten-year period.

In fact, fund managers have found it so hard to outperform that, of the funds that were trading at the start of January 2014, just 61.33% of them were still doing so at the end of December 2023. That’s right, almost four out of ten funds failed to survive the full ten years.

Of course, it might still be worth investing in an active fund if you knew in advance that it’s likely to be one of the very few long-term outperformers. The problem is that predicting a “star” fund ahead of time is very hard to do, and past performance tells us very little, if anything, of value about future performance.

To illustrate this point, the SPIVA team examined the persistence of funds available to Canadian investors. Among Canadian-based equity funds that ranked in the top half of peer rankings over the five-year period to the end of December 2017, only 45% remained in the top half, while 55% fell to the bottom half or ceased to exist, at least in their own right, in the following five-year period.

To be clear, I’m not saying that active managers in Canada are any less competent than their counterparts in other countries. What the SPIVA analysis shows is that managers all over the world struggle to add any value whatsoever after costs. Distinguishing luck from skill in active management is notoriously difficult, but the proportion of funds that beat the markets in the long run is consistent with random chance.

Why do so few active managers outperform?

So why is active fund performance generally so poor? The most important reason is that beating the market is extremely difficult. Why? Because the financial markets are highly competitive and very efficient. Never before have investors had so much information at their disposal. New information is made available to all market participants at the same time, and prices adjust accordingly within minutes, or even seconds.

In the short term, then, prices move up and down in a random fashion. So, identifying a security that is either underpriced at any one time is a huge challenge.

Another reason why active fund performance tends to be so disappointing is that active managers incur significant costs. Salaries, research, marketing, the cost of trading and so on: all of these things need paying for, and it’s the investor who picks up the tab. Once all these costs are added together, they present a very high hurdle for fund managers. Simply put, any outperformance they succeed in delivering is usually wiped out by fees and charges. Continue Reading…

An Interac survey being released today finds that more than two thirds (69%) of Canada’s Gen Z generation [defined as Canadians aged 18 to 27] have embraced the mobile wallet, while almost as many (63%) would rather leave their old-fashioned physical wallets at home for short trips. Gen Z’s Interac contactless mobile purchases also rose 27% in the first half of 2024, compared to the same period a year earlier.

Gen Z appears to be more enthusiastic than their counterparts in older cohorts: 60% of Millennials [aged 28-43] embraced mobile wallets, compared to 44% of Gen Xers [aged 44-59] and just 27% of Baby Boomers [aged 60-78.] Only 10% of the older Silent Generation [age 79 or older] did so.

A whopping 63% of Gen Z mobile wallet users have loaded their Interac debit card on their smartphones, and 31% plan to set debit as their default method of payment. For 63% of them, the reason is perceived faster payment times compared to physical card payments.

“Choosing your default payment method may feel like a small step, but it can play a big role in shaping Canadians’ ongoing spending habits,” said Glenn Wolff, Group Head and Chief Client Officer, Interac in a press release. “When consumers tap to pay with their phones, the decision to select a card from the digital wallet is easy to miss. Canadians could end up unintentionally using a default payment method that prompts them to take on more debt. This differs from traditional physical wallets where the consumer had to select the card they wanted to use each time.”

Majority want to be smarter with money

62% of Gen Z want to be “more mindful when spending” with 57% saying they want the option to use debit when paying in store or online; 79% of them say the cost of living is too expensive and 59% feel the need to be smarter with their money.

Interact says this generation’s desire to control overspending is heightened by back-to-school season: last year, family clothing stores saw almost twice as many Interac Debit mobile purchases in September and October compared to earlier that year in January and February. 54% of Gen Zs see the need to develop new habits to stay in control over their finances, while 56% are setting a timeline for this September to introduce new habits. Continue Reading…

As an engineer by education & training and an analytical person, it shouldn’t come as a surprise to readers that I ponder a lot. I like to think about something carefully before deciding or reaching a conclusion. Although this approach may not work in all situations, I enjoy being analytical on major life decisions.

The other day I woke up with this interesting idea in my head. The idea simply wouldn’t escape from my head and I ended up thinking about it for the entire day.

The interesting idea is simple: Should we go all in on QQQ with our RRSPs?

Since this is an interesting idea, I thought I’d turn it into a blog post, analyze the idea thoroughly, and hopefully come to a conclusion.

Things to consider

A few things before we dive into the analysis.

An RRSP is a tax-deferred account. When you contribute to one, you get a tax deduction for 100% of your contributions. If you contribute $10,000 to your RRSP, it will reduce your net income by $10,000, and potentially bring you down to the lower tax bracket.

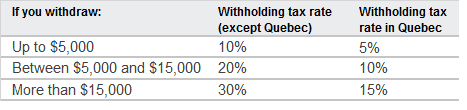

When you withdraw money from your RRSP, you will be subject to withholding tax. The amount of withholding tax is based on how much you take out.

The net amount after the RRSP withholding tax is then taxed at your marginal tax rate.

You also must convert an RRSP to a retirement income option such as a RRIF by the end of the year that you turn 71. Although there are no mandatory withdrawal requirements in the year you set up your RRIF, you must start withdrawing money the year after setting up your RRIF (effectively at age 72). Furthermore, there’s a minimum withdrawal rate for RRIF. The withdrawal rate increases as you age.

Note: You can convert your RRSP before age 71. If you do, there’s a minimum withdrawal rate starting at age 55.

Just like the RRSP, money withdrawn from an RRIF is taxed like working income, or at 100% of your marginal tax rate.

In other words, it doesn’t matter whether the money is from capital gains or dividend income, money withdrawn from an RRSP and an RRIF is taxed at 100% of your marginal tax rate. You don’t get any preferential dividend tax treatment like in non-registered accounts.

When we do start living off our investments (aka live off dividends), our withdrawal strategy is very similar to Mark from My Own Advisor – NRT. This means drawing down some non-registered (N) assets along with registered assets (R), leaving TFSAs (T) for as long as possible.

More details:

N – Non-registered accounts – we most likely will work part-time to keep ourselves engaged and live off dividends to some degree from our non-registered accounts. The preferential dividend tax credits will come in handy.

R – Registered accounts (RRSPs) – we plan to make some early withdrawals from our RRSPs slowly. We may collapse our RRSPs entirely before age 71. We may also convert our RRSPs to RRIFs. This is not entirely decided (if we do convert to RRIFs, we want to make sure the dollar amount is relatively small). Early withdrawals will help us from having a large amount of money in our RRSPs and having a big tax hit when we start withdrawing. In other words, this will help smooth out our taxes.

T – TFSAs – since any withdrawals from TFSAs are tax-free, we intend not to touch our TFSAs for as long as possible so they can compound over time.

Note: if you’re interested in this retirement projections service, mention TAWCAN10 to Mark and Joe to get a 10% discount.

We may also do an RNT (Registered, Non-Registered, then TFSA) withdrawal strategy but will need to crunch some numbers. Whether it’s NRT or RNT, the important part is that we plan to slowly withdraw money from our RRSPs.

Current RRSP Holdings

Although RRSPs are best for holding U.S. dividend stocks to avoid the 15% withholding tax, we hold U.S. and Canadian dividend stocks and ETFs inside our RRSPs.

At the time of writing, we hold the following stocks and ETFs inside our RRSPs:

Our RRSPs consist of 18 U.S. dividend stocks, 10 Canadian dividend stocks, and 2 index ETFs.

In terms of dollar value, my RRSP makes up about 70% while Mrs. T’s RRSP (spousal RRSP) makes up about 30%. Ideally, it would be great if our RRSP breakdown were 50-50 (I’m ignoring my work’s RRSP so in reality the composition is more like a 25-75 split).

Because we started Mrs. T’s RRSP a few years later than mine it hasn’t had as much time to compound. Furthermore, I converted over $120,000 worth of CAD to USD in my RRSP when CAD was above parity. Over time, this gave my self-directed RRSP an automatic 30% performance boost.

In addition, because the exchange rate hasn’t been as attractive, the only U.S. holdings Mrs. T has are Apple and QQQ. The rest of her RRSPs are all in Canadian dividend stocks.

We purchased QQQ earlier this year inside Mrs. T’s RRSP. Dollar-wise, it makes up a very small percentage of our combined RRSPs.

Some info on QQQ

For those readers who aren’t familiar with QQQ, it’s an ETF from Invesco. Since launching in 1999, the ETF has demonstrated a history of outperformance compared to the S&P 500.

QQQ tracks the Nasdaq 100 Index. The fund is rebalanced quarterly and reconstituted annually. At the time of writing, QQQ holds 101 stocks with the top 10 holdings being Microsoft, Apple, Nvidia, Amazon, Meta, Broadcom, Alphabet Class A & C, Tesla, and Costco. The top 10 holdings make up 47.01% of the fund.

The top 11 – 20 holdings for QQQ are AMD, Netflix, PepsiCo, Adobe, Linde, Cisco, Qualcomm, T-Mobile US, Intuit, and Applied Materials. These holdings make up 15.71% of QQQ.

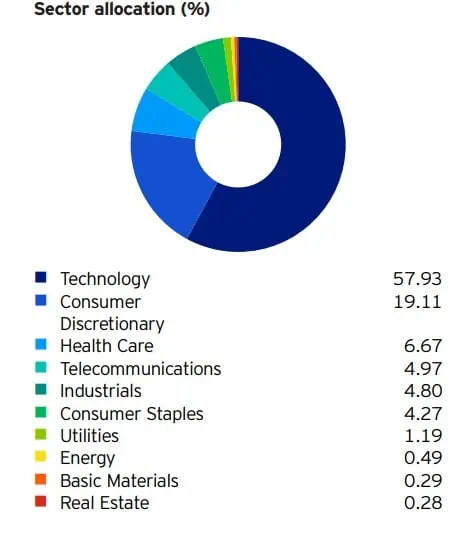

Due to the nature of the Nasdaq 100 Index, QQQ is heavily exposed to technology and consumer discretionary sectors.

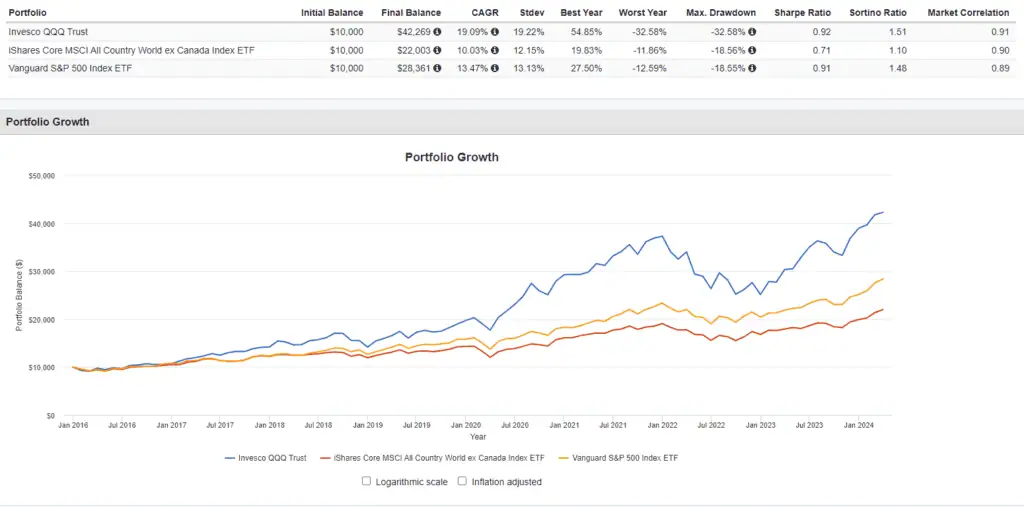

As you can see from below, it also outperformed XAW and VFV significantly. This is the key attraction of QQQ, as the fund has historically outperformed many major indices.

Source: Portfolio Visualizer

As you can see from above, $10,000 invested in QQQ in 2016 would result in over $42,000 in 2024 whereas the same amount invested in XAW and VFV would result in less than $30,000.

Case for going all-in on QQQ

Why would we consider going all in on QQQ?

Because QQQ has done very well historically compared to the major U.S. and Canadian indices.

Per the chart above, QQQ had an annualized return of 19.09% since 2016. In the last 20 years, QQQ has had an annualized return of 14.03% and an annualized return of 18.12% in the last 10 years.

Assuming we invest $150,000 in QQQ and enjoy an annualized return of 15% for the next 10 years, we’d end up with $606,833.66, assuming no additional contributions. On the flip side, if we have the same money and have an annualized return of 10% (long-term stock return), we’d end up with $389,061.37. This means investing in QQQ would result in more than $217.7k of difference in return on capital or 56%. This is a pretty significant difference.

Yes, historical returns don’t guarantee future returns. However, the high exposure to technology stocks should allow QQQ to continue the superior return for years to come.

Due to the fact that RRSP and RRIF withdrawals are taxed 100% at our marginal tax rate, it makes sense to attempt to maximize the total return inside of RRSPs/RRIFs instead of a mix of dividend income and capital return.

Case against going all in on QQQ

The biggest case against going all in on QQQ? Our dividend income would take a big hit.

Our RRSPs contribute about 30% of our annual dividend income. With our 2024 target of $55,000, selling everything in our RRSPs and holding QQQ only would reduce our total dividend income to about $38,500 (ignoring QQQ distributions completely).

But focusing on dividend income alone is a bit silly when we should be considering total return and the total portfolio value.

Out of the 18 U.S. stocks that we hold in our RRPS, QQQ holds 9 of them already. The stocks that QQQ doesn’t hold are:

Abby

Johnson & Johnson

Coca-Cola

McDonald’s

Procter & Gamble

Target

Visa

Waste Management

Walmart

These 9 stocks make up about 25% of our RRSP in terms of dollar value. Since we purchased these stocks many years ago, they have all done very well, with a few of them being multi-baggers. I would hate to sell the likes of Visa and Waste Management.

Investing in QQQ does mean that when we start to live off our investment portfolio, rather than withdrawing mostly from dividends inside our RRSPs in the first few years (to increase our margin of safety), we’d need to sell QQQ shares and touch our principal.

If there are a few years of poor returns at the beginning of our retirement, this could cause a significant reduction in our portfolio value. Essentially, selling shares may not have as much margin of safety compared to relying on withdrawing dividends only.

Another case against going all in on QQQ is that QQQ is currently highly concentrated in technology stocks so it’s not all that diversified compared to other index ETFs like XAW. The latest AI hype has significantly bumped up the share price of many technology stocks. Would we see a Dot Com type of bubble in the future and hamper the return of QQQ? That’s certainly possible.

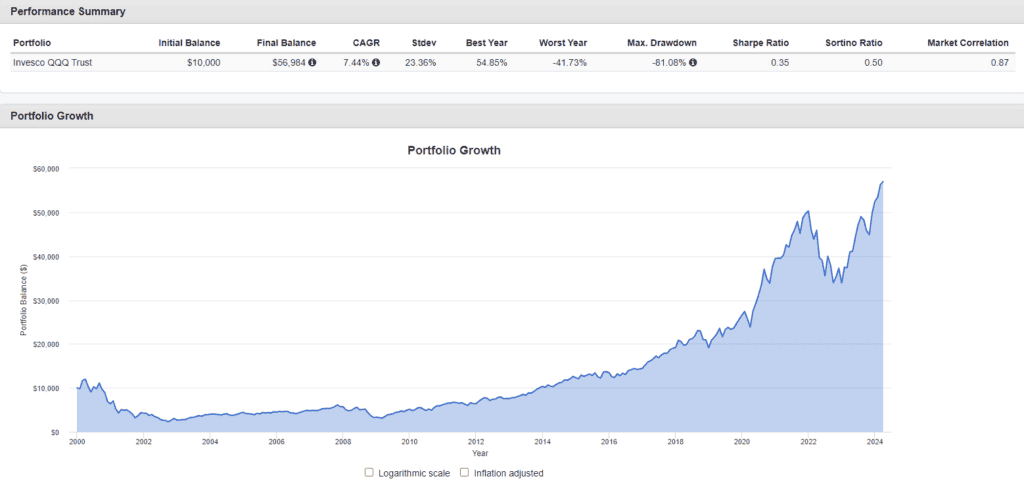

QQQ historical return

As you can see from the chart above, QQQ didn’t recover from the Dot Com bubble for about 14 years. This is a risk we would take on if we were to go all in on QQQ.

Potential Alternatives to going all-in on QQQ

Instead of going all in on QQQ, there are some potential alternatives.

First, we can simply add more QQQ shares in the next few years to have QQQ make up a larger percentage of our dividend portfolio. This is already our plan of record but we stay focused on this goal instead of purchasing more dividend paying stocks in our RRSPs.

Second, since we hold QQQ inside of Mrs. T’s RRSP and she holds mostly Canadian dividend stocks in her RRSP, we can consider closing out these positions and using the money to buy QQQ shares.

If we were to do that, we’d only lose about 12% of our forward annual dividend income, going from $55,000 to $48,400. Assuming QQQ continues the superior performance over other indices, holding only QQQ and Apple in Mrs. T’s RRSP and continuing to contribute to her RRSP only may mean that we have a higher chance of ending up with a 50-50 RRSP split down the road.

Some additional logistics to consider

The second option mentioned above is quite intriguing. But there are some logistics to consider if we were to forward with this option.

The first thing to consider is that we’d need to sell all 9 stock holdings in Mrs. T’s RRSP. At $4.95 per trade at Questrade, this would cost us $44.55. Not a significant amount of money but it would be cheaper if we were to transfer her RRSP to Wealthsimple.

Second, we’d need to convert CAD to USD and take a hit on the exchange rate. Utilizing Norbert’s Gambit would allow us to save on the additional current exchange fees. The alternative solution would be to journal as many of the holdings to the U.S. exchange, close the positions, and end up with USD.

Another option is to consider the Canadian equivalents, like XQQ, ZQQ, HXQ, or ZNQ to avoid currency conversion. As many of you know, I’m all for simplicity and straightforwardness, so it makes sense to hold the original ETF QQQ instead of other alternatives.

Conclusion – Should we go all in on QQQ?

So, have I reached a decision after all the considerations?

I’ll admit, the second option mentioned (holding only QQQ in Mrs. T’s RRSP) is very intriguing to me. But I am going to sleep on it for a bit and discuss the idea with Mrs. T before making any major decisions. In the meantime, we will continue to add more QQQ shares in Mrs. T’s RRSP so QQQ makes up a bigger percentage of our dividend portfolio.

Readers, what would you do? Would you go all in on QQQ?

Hi there, I’m Bob from Vancouver, Canada. My wife & I started dividend investing in 2011 with the dream of living off dividends in our 40’s. Today our portfolio generates over $2,700 in dividends per month. This post originally appeared on Tawcan on July 15, 2024 and is republished on the Hub with the permission of Bob Lai.

Darren Coleman (left) and Kim Moody (right, with glasses).

The following is an edited transcript of an interview conducted by financial advisor Darren Coleman’s of the Two Way Traffic podcast with tax expert Kim Moody, of Moody Private Client. It appeared on August 8th: click here for full link.

Moody recently wrote an article in the Financial Post about the government flirting with the idea of a home equity tax, even on principal residences. Such a tax could result in an annual levy of about $10,000 for a home worth $1 million. He described that, along with the increase in the capital gains inclusion rate that has already passed into law, “really bad tax planning” based on ideology, not economics.

In the podcast Moody and Coleman also discussed …

The disparity between U.S. and Canadian tax rates, beginning with how the state of Florida compares with Ontario, a difference of 17%.

The tax model established in Estonia lets you reinvest in your company without paying corporate tax while personal income is taxed at a flat rate of 20%. They say such a system would work in Canada, and celebrate success and entrepreneurship.

What organizations like the Fraser Institute and mainstream economists think about Canada’s economic performance.

Below we publish an edited transcript of the start of the interview, focusing on the capital gains inclusion rate and trial balloon about taxing home equity.

Darren Coleman, Raymond James

Darren Coleman: I’m Darren Coleman, Senior Portfolio Manager with Raymond James in Toronto. I’m delighted to be joined by Kim Moody of Moody’s tax and Moody’s private client. You’re also a law firm based in Calgary, Alberta, and probably one of Canada’s best known tax and estate planning advisors. You may have heard our last conversation with Trevor Perry about some of the issues we might be seeing in terms of taxation of the principal residence in Canada.

I think because governments have spent so much money that we’re going to see tremendous innovation in taxation. Do you want to set the table for the article you wrote in the Financial Post, where you talked about where this is coming from, and why Canadians might be on alert for what might be coming to tax the equity in their homes.

Kim Moody: The point of the piece was mainly just to put Canadians on notice that you had the Prime Minister and the finance minister sitting down with what I call a pretty radical

think tank. I consider them an ideological bastion of radical thought but that issue aside,

they call them call themselves a think tank, and this particular one, led by Paul Kershaw of

Generation Squeeze, has stuff on their website that pretty much attacks older Canadians:

basically saying they’ve gotten rich by going to sleep and watching TV. Unbelievable. Whoever approved that, it’s just so offensive. But that issue aside, the whole connotation of the messaging is that, hey, these people are rich. We’ve got these poor young Canadians who are not rich and they can’t afford houses because you’re rich and …

Darren Coleman Someone should do something about it, right? That’s the trick.

Kim Moody

Kim Moody: Someone should do something about it. And their solution is to introduce a so-called Home Equity tax on any equity of a million dollars or more. And they call it a modest surtax of 1% per year. So it’s like another, effectively property tax … It’s just so nonsensical and so offensive on a whole bunch of different levels. Like you think about grandma and grandpa, yeah, they’ve got equity in their homes, but they don’t have a lot of cash. They’ve been working hard their entire lives to pay off their houses. And yes, they want to transfer down to their kids at some point, but right now, they’re living again, and they’re making ends meet by living off their pensions that they worked hard, and you’re expecting them to shell out more money for that, and I find that offensive.

…. Back to the original premise of why I wrote the article: to let Canadians know that our leaders are entertaining stuff like this. It doesn’t mean they’re going to implement it, but they’re actually entertaining radical organizations like this and secondly, just to put Canadians on

notice that this is just the beginning. If this regime continues with out-of-control spending and no

adherence to basic economics, then we could expect a whole bevy of new taxes.

Darren Coleman

Indeed, they’ve already done some of this, right? So you know that this idea about we’re going to tax home equity, either through some kind of annual surtax on equity over a certain amount, or we’re going to put a capital gain on principal residences. And I would argue that for years now, Canadians have had to report the sale of the principal residence on their tax returns, which is a non-taxable event, yet you now have to tell them, and if you don’t, there’s a penalty. Continue Reading…