By Brooks Ritchey

(Sponsor Content)

Alternative investment funds are an exciting new strategy class that were previously unavailable to retail investors in Canada. Since they are new to the scene, many advisors and investors are interested, but don’t quite know where to begin. Since I have worked in the alternative investment space for years, I thought I could help explain how investors could benefit from these hedging strategies.

Demystifying Liquid Alternatives for investors

Some advisors feel that these strategies are too volatile or complicated to explain to their clients. We spend a lot of our time trying to explain that these are not complicated mysterious investments. The irony is that many alternative investments, liquid alternatives, especially with regulatory oversight, are about the same risk level as fixed-income products.

Others also worry about the fees on hedge funds, but they have come down a lot. Since I’ve been involved in the hedge fund industry, fees have come down from 2% management and 20% performance fees to 75 basis points management fees and no performance fees for some products.

How would you explain Liquid Alternatives to investors?

It’s an investment that has different characteristics than traditional equity and fixed income. Equity markets depend on the trend in economic growth and bonds depend on a different set of macroeconomic factors, but they’re both dependent on a trend. If you’re trying to find a strategy that’s looking for winners in the equity or in the bond market when the trends aren’t positive, you want to consider liquid alternatives. Continue Reading…

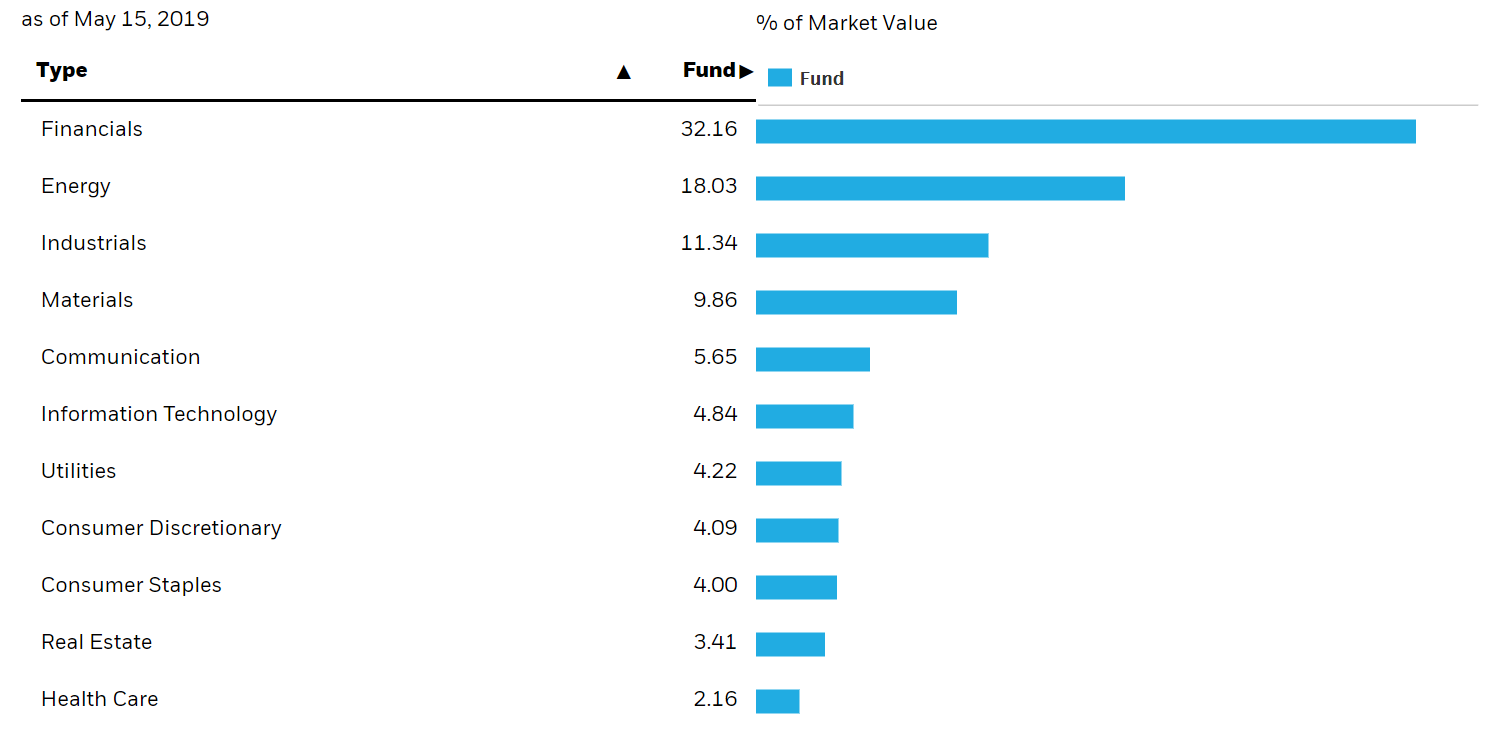

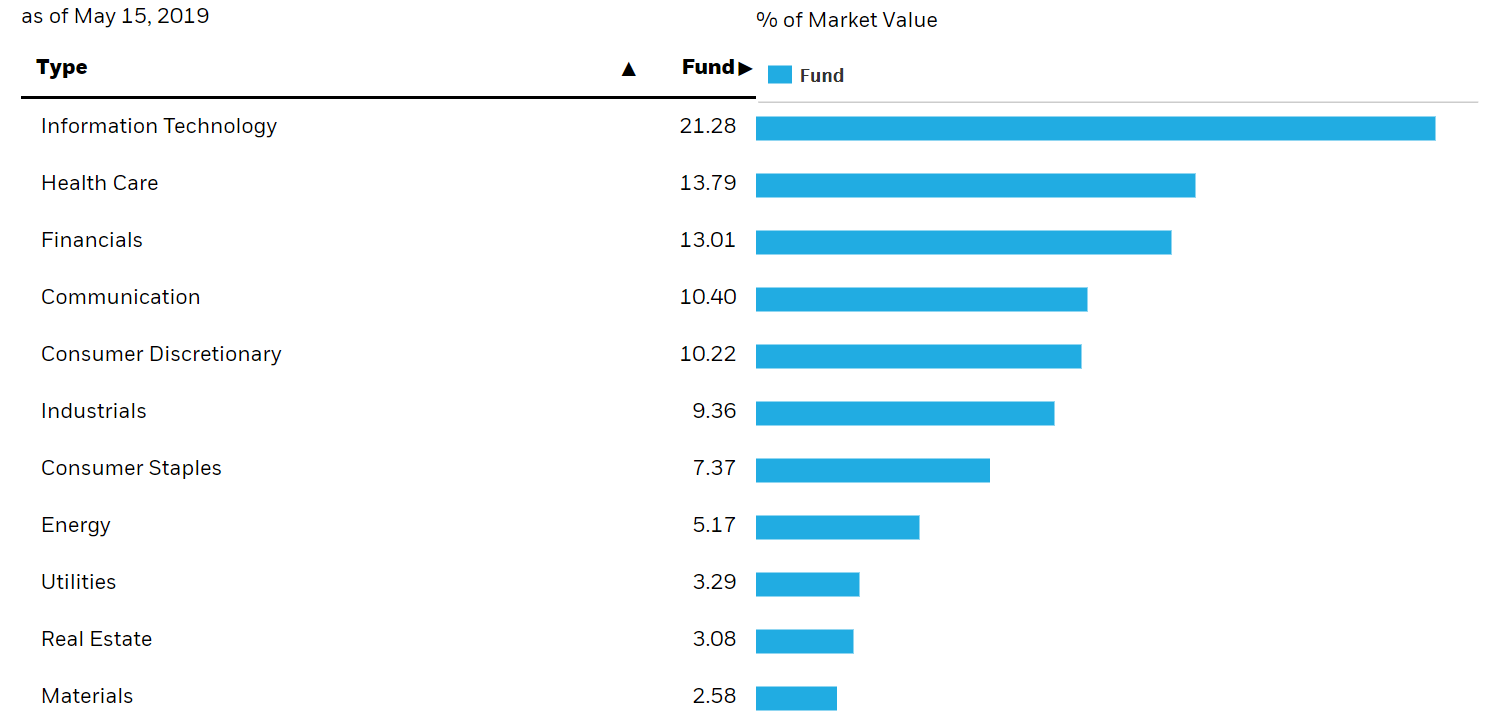

The Canadian investor needs the sector and geographic diversification offered by the US and perhaps International markets. Here’s the sector breakdown of the S&P 500, by way of iShares IVV.

The Canadian investor needs the sector and geographic diversification offered by the US and perhaps International markets. Here’s the sector breakdown of the S&P 500, by way of iShares IVV. The basic principle of the need for added diversification holds true whether a Canadian investor embraces core index funds or dividend focused funds. How much you add by way of International exposure is certainly a personal decision. I am of the opinion that you might go light on that front given that the large and mega cap US companies earn a considerable percentage of their profits overseas. That said, in a recent CTCI investing post I suggested you might also look to developing markets where there is

The basic principle of the need for added diversification holds true whether a Canadian investor embraces core index funds or dividend focused funds. How much you add by way of International exposure is certainly a personal decision. I am of the opinion that you might go light on that front given that the large and mega cap US companies earn a considerable percentage of their profits overseas. That said, in a recent CTCI investing post I suggested you might also look to developing markets where there is