For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

Navigating the financial landscape of the medical industry is essential for healthcare professionals and medical students aiming to build successful careers. Understanding the economic aspects enhances the ability to make informed decisions and contributes to better resource management, ultimately improving patient care.

Here’s what to know about the financial side of the medical industry.

By Dan Coconate

Special to Financial Independence Hub

Image by Adobe Stock/Photographer Nuttapong Punna|.

When it comes to fast-growing industries, few stand out like healthcare.

While the top priority in healthcare is always quality patient care, you can only provide that care if you can afford to keep the lights on.

In other words, strong financial management is the foundation that allows any healthcare organization to fulfill its primary purpose.

Let’s take a quick look and discover the financial dynamics of the medical industry, covering budgeting, revenue cycles, and economic challenges healthcare providers face.

Cost Management and Budgeting

Cost management aids in sustaining healthcare facilities. Hospitals and clinics must carefully budget for various expenses:

Staffing

Medical supplies

Equipment

Technology upgrades

By implementing strategic budgeting practices, healthcare providers can optimize their operations, reduce waste, and allocate resources more efficiently. This is particularly vital in rural areas, where financial constraints can impact the quality of healthcare services.

Funding and Revenue Streams

Understanding the various funding and revenue streams is fundamental in the medical industry. In Canada, healthcare is primarily funded through public sources, including federal and provincial government allocations. However, private contributions, grants, and partnerships also supplement these funds.

Healthcare professionals and administrators should be well-versed in navigating these financial avenues to ensure their institutions remain well-funded and capable of delivering high-quality care.

Financial Compliance and Regulations

All healthcare providers must adhere to financial compliance and regulatory standards. This includes maintaining accurate financial records, adhering to billing practices, and ensuring transparency in financial transactions.

Compliance safeguards entire institutions against legal repercussions and builds trust with patients and stakeholders. Staying updated with the latest regulations and implementing financial management systems can prevent discrepancies and enhance operational efficiency.

Investment in Technology and Innovation

Investment in technology and innovation is a significant financial consideration for professionals in the healthcare industry. Advanced medical technologies, electronic health records (EHRs), and telemedicine platforms require substantial financial outlays but offer long-term benefits. Continue Reading…

Aerial drone view of a wind farm on the Atlantic coast. Image courtesy BMO ETFs/Getty Images

By Andrew Vachon, BMO Global Asset Management

The Bank of Canada (BoC) cut rates on June 5th for the first time after one of the most aggressive hiking cycles in Canadian history.

Market expectations from the BoC indicate that we may see 2 to 3 more cuts before the end of the year with the second cut potentially as early as July and the remaining later in the year.

South of the border, inflation has remained “stickier” however; the market expects the U.S. Federal Reserve (the Fed) to cut rates twice before the end of the year with the first beginning in September. Moreover, forecasters are predicting the BoC could potentially cut the overnight rate from the current rate of 4.75% all the way down to 3.5% by this time next year, presenting more opportunity for the Utilities sector. 1

With the anticipation of further rate cuts from the BoC and the Fed we may see the Utilities sector shine. Government bond yields tend to have an inverse relationship with utilities (when interest rates drop, utility stock prices typically increase, and vice versa). This is mainly due to the costs involved with these companies. The cost of construction for power plants, and the maintenance of infrastructure required to deliver gas, water, or electricity can make utilities expensive when the cost of borrowing is high.

From a technical perspective, the BMO Equal Weight Utilities Index ETF (Ticker: ZUT) just broke out of a massive “double bottom” reversal pattern this week. A double bottom pattern is a classic technical analysis charting formation showing a major change in trend from a prior down move. The recent close above resistance at $20.60 completed the pattern, shifted the long-term trend to bullish, and opened an initial upside target that measures to $23.40.

One of the key drivers for the turnaround in utility stocks as of late is a sharp decline in long-term interest rates. There is now a possibility of yields testing the lows of 2023, which could be a persistent tailwind for interest rate sensitive sectors of all stripes and perhaps push this Utility ETF above the initial upside target of $23.40 at some point in the next 6-12 months. 2

Yielding the Benefits

For the long-term investor, Utilities offer investors stable and consistent dividends over time along with lower volatility. The long-term growth potential to deliver safe and reliable returns, make the sector an attractive investment to consider adding to your portfolio. Utilities overall have remained fundamentally strong as they provide basic services such as gas, water, electricity and telecommunications that will always be in demand regardless of where we are in the economic cycle.

There are long-term benefits for Canadian investors, especially those who might consider the current environment as an opportunity to capture growth. Continue Reading…

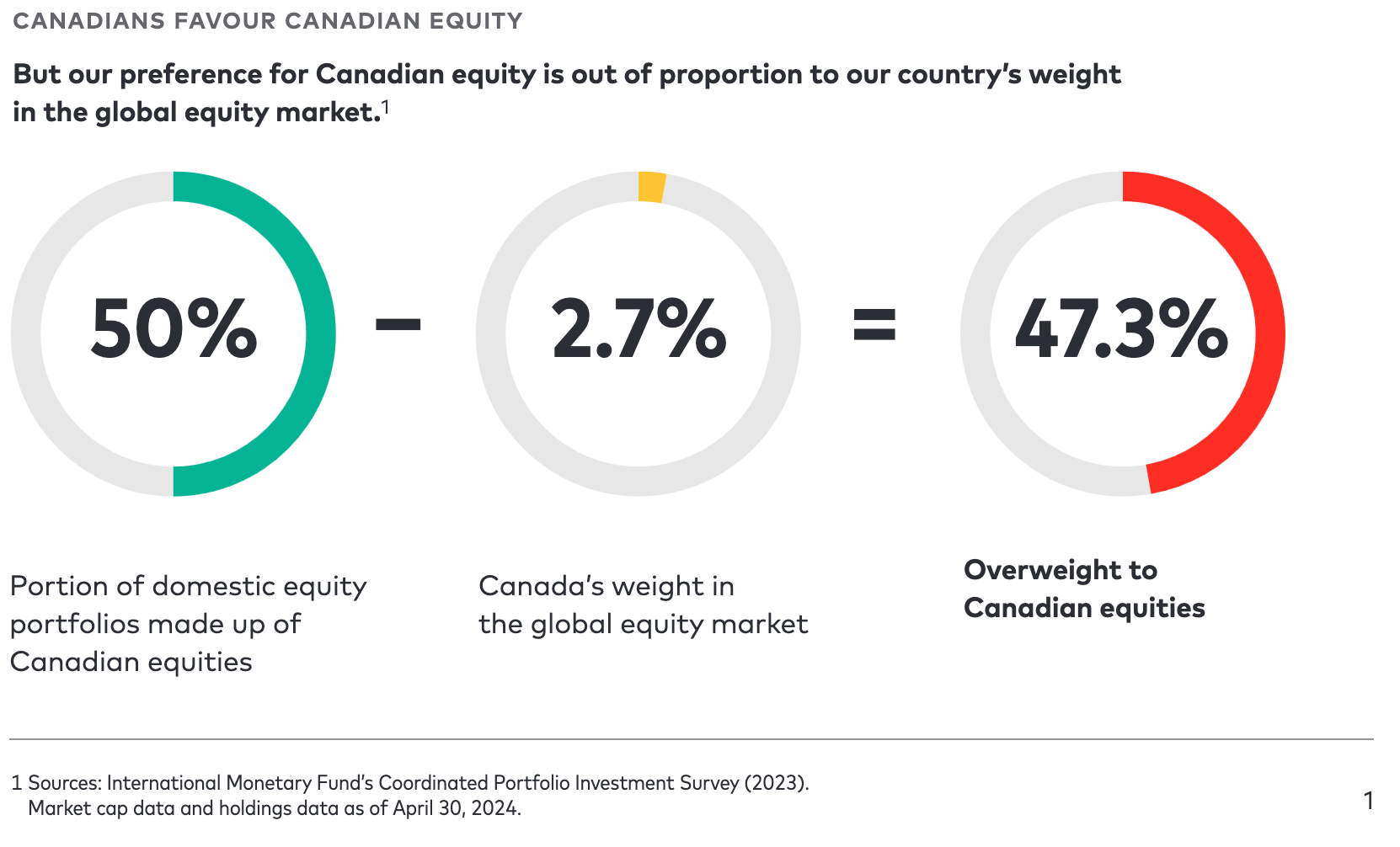

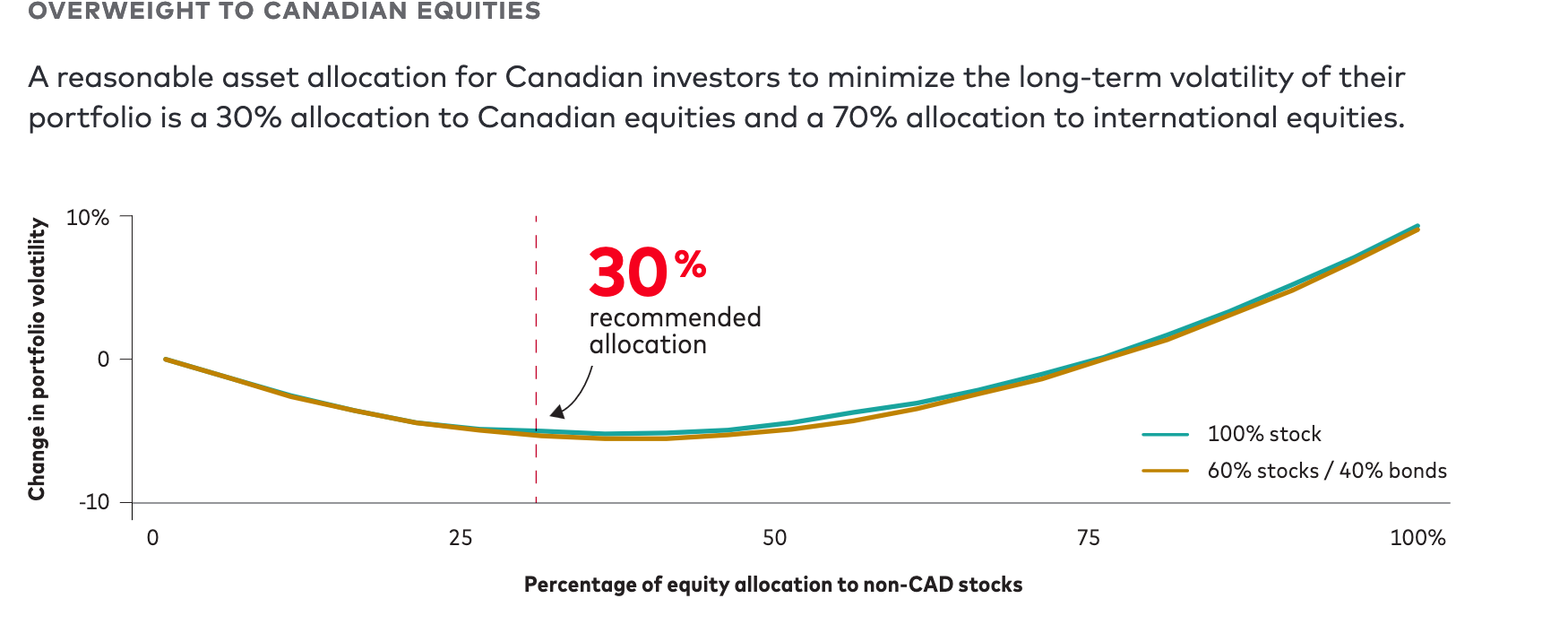

A just-released study from Vanguard Canada on Home Country Bias shows that Canadians have about 50% of their portfolios allocated to Canadian equities: well beyond what is recommended for a country that makes up less than 3% of the global stock market.

As the chart below shows, Vanguard recommends just 30% in Canadian stocks but notes that the domestic overweight is slowly decreasing as investors move to global and U.S. equities.

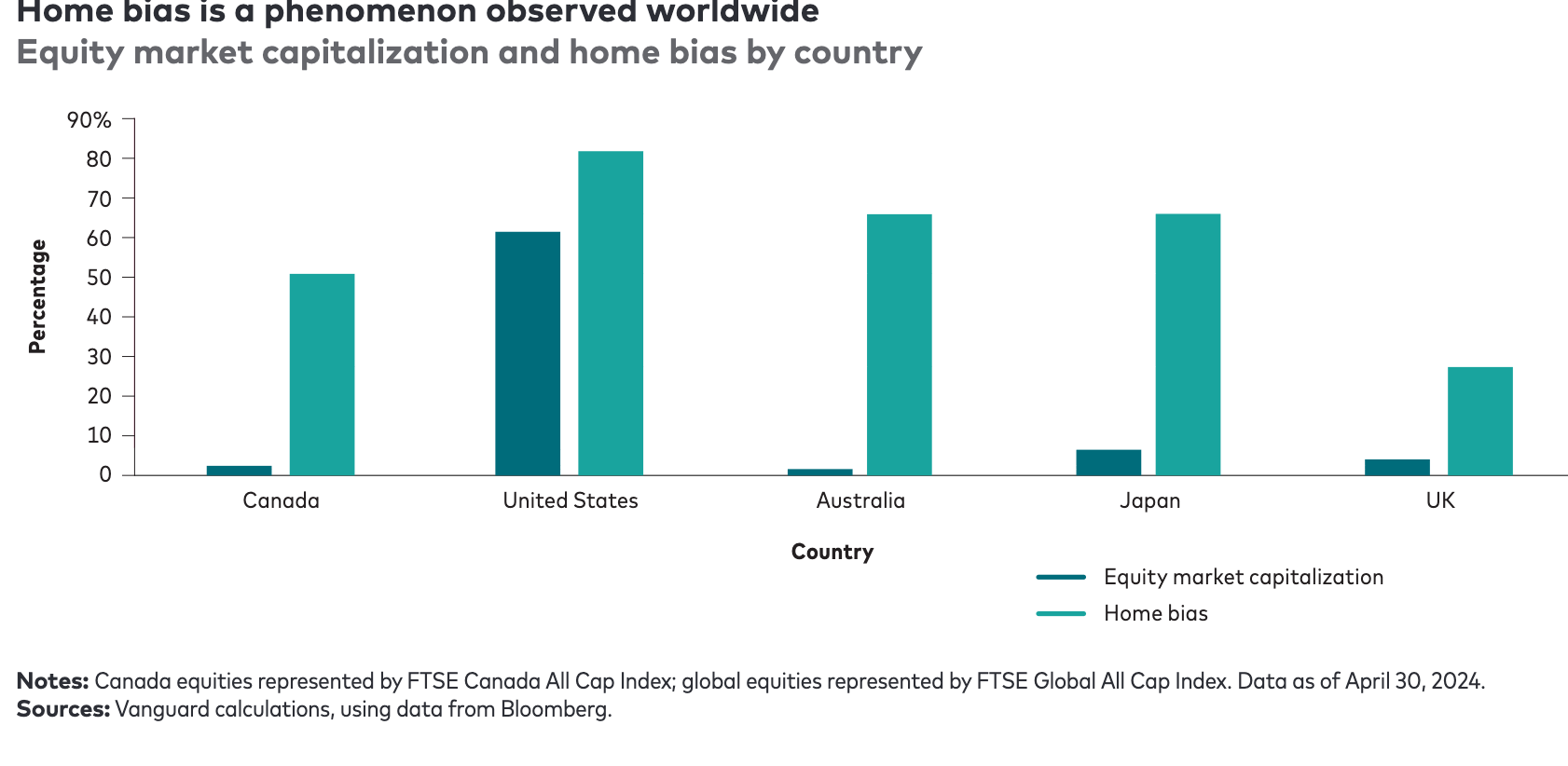

Vanguard says home country bias is not unique to Canada: Americans behave similarly with respect to the U.S. stock market. But as you can see from the chart below, because the U.S. makes up more than half of the global stock market by market capitalization, the gap between its relative overweighting is far less dramatic than in Canada. Canada’s home country bias is almost as pronounced as in Australia (a similar market to Canada in terms of resources and financial stocks), and Japan is not far behind.

However,Vanguard adds, “overall, Canadians and investors in other developed countries are trending towards a greater appetite for diversification through global equities.”

Too much Canada can be volatile

So what’s wrong with having too much Canadian content (both stocks and bonds)? Vanguard says portfolios overweight Canadian equity can be volatile because the domestic market is too concentrated in just a few economic sectors. “Relative to the global market, Canada’s market is concentrated within a few large names. It is also significantly overweight in the energy, financials and materials sectors, and significantly underweight in others.” Continue Reading…

The United States stock markets have delivered positive returns through much of 2024, continuing the positive momentum that was established in the previous year.

However, that performance has increasingly been powered by a smaller segment of large-cap companies. Indeed, readers have undoubtedly heard about the outsized performance of the “Magnificent 7” in the tech space over the past year. If we strip out the “big six” of Amazon, Meta, Nvidia, Microsoft, Apple, and Alphabet from the S&P 500, we have experienced three calendar quarters of negative earnings growth across the rest of the market.

Investors took profits in the month of April. Demand resumed in the month of May, but with a broader range of equities. Nvidia continued to show its dominance, but there were other sectors and stocks that were able to catch up with the leaders to close out the first half of 2024.

The summer season is historically slow in the markets. Harvest’s portfolio management team expects volatility to persist for both bonds and equities. Moreover, the team emphasizes that this summer is a key moment to stay active, attentive, and invested. A prudent strategy in this environment involves looking under the surface for opportunities while generating cash flow from call options to support total returns.

June Healthcare check up

The healthcare sector pulled back slightly in the month of May 2024. Negative moves in the healthcare sector over the course of May 2024 were driven by stock specific events. Macroeconomic data sets impacted the healthcare sector in line with others. Within healthcare, the managed care subsectors experienced volatility earlier in 2024 and changes to reimbursement structures impacted valuations in the near term. The Tools & Diagnostics sub-sector has also proven volatile due largely to a slower-than-expected recovery in China.

Regardless, there are still very promising opportunities in the GLP-1 drug category space for diabetes and obesity. The uptake of these drugs in the U.S. has been significant at a still-early stage in their lifespan. A recent study from Manulife Canada found that drug claims for anti-obesity medications in Canada rose more than 42% from 2022 to 2023.

Harvest Healthcare Leaders Income ETF (HHL:TSX) offers exposure to the innovative leaders in this vital sector. This equally weighted portfolio of 20 large-cap global Healthcare companies aims to select stocks for their potential to provide attractive monthly income as well as long-term growth. HHL is the largest active healthcare ETF in Canada and boasts a high monthly cash distribution of $0.0583.

Harvest Healthcare Leaders Enhanced Income ETF (HHLE:TSX) is built to provide higher income every month by applying modest leverage to HHL. It last paid out a monthly cash distribution of $0.0913 per unit. That represents a current yield of 10.44% as at June 14, 2024.

Where does the technology sector stand right now?

Investors poured back into technology stocks in May 2024 after taking profits in the month of April. However, they were more discriminating than in previous months and showed a preference for hardware stocks, specifically semiconductors.

Nvidia maintained its leadership position. It has soared past a $3 trillion market capitalization in the first half of June 2024. However, other AI-related tech stocks encountered turbulence which may give some investors pause around the broader bullish case for AI. Continue Reading…

Come gather ’round people Wherever you roam And admit that the waters Around you have grown And accept it that soon You’ll be drenched to the bone If your time to you is worth savin’ And you better start swimmin’ Or you’ll sink like a stone For the times they are a-changin’

In this month’s commentary, I will discuss both how and why the environment going forward will differ markedly from the one to which investors have grown accustomed. Importantly, I will explain the repercussions of this shift and the related implications for investment portfolios.

The Rear View Mirror: Where we’ve been

After being appointed Fed Chairman in 1979, Paul Volcker embarked on a vicious campaign to break the back of inflation, raising rates as high as 20%. His steely resolve ushered in a prolonged era of low inflation, declining rates, and the favourable investment environment that prevailed over the next four decades.

Importantly, there have been other forces at work that abetted this disinflationary, ultra-low-rate backdrop. In particular, the influence of China’s rapid industrialization and growth cannot be underestimated. Specifically, the integration of hundreds of millions of participants into the global pool of labour represents a colossally positive supply side shock that served to keep inflation at previously unthinkably well-tamed levels in the face of record low rates.

It’s all about Rates

The long-term effects of low inflation and declining rates on asset prices cannot be understated. According to Buffett:

“Interest rates power everything in the economic universe. They are like gravity in valuations. If interest rates are nothing, values can be almost infinite. If interest rates are extremely high, that’s a huge gravitational pull on values.”

On the earnings front, low rates make it easier for consumers to borrow money for purchases, thereby increasing companies’ sales volumes and revenues. They also enhance companies’ profitability by lowering their cost of capital and making it easier for them to invest in facilities, equipment, and inventory. Lastly, higher asset prices create a virtuous cycle: they cause a wealth effect where people feel richer and more willing to spend, thereby further spurring company profits and even higher asset prices.

Declining rates also exert a huge influence on valuations. The fair value of a company can be determined by calculating the present value of its future cash flows. As such, lower rates result in higher multiples, from elevated P/E ratios on stocks to higher multiples on operating income from real estate assets, etc.

The effects of the one-two punch of higher earnings and higher valuations unleashed by decades of falling rates cannot be overestimated. Stocks had an incredible four decade run, with the S&P 500 Index rising from a low of 102 in August 1982 to 4,796 by the beginning of 2022, producing a compound annual return of 10.3%. For private equity and other levered strategies, the macroeconomic backdrop has been particularly hospitable, resulting in windfall profits.

From Good to Great: The Special Case of Long-Duration Growth Assets

While low inflation and rates have been favourable for asset prices generally, they have provided rocket fuel for long-duration growth assets.

The anticipated future profits of growth stocks dwarf their current earnings. As such, investors in these companies must wait longer to receive future cash flows than those who purchase value stocks, whose profits are not nearly as back-end loaded.

All else being equal, growth companies become more attractive relative to value stocks when rates are low because the opportunity cost of not having capital parked in safe assets such as cash or high-quality bonds is low. Conversely, growth companies become less enticing vs. value stocks in higher rate regimes.

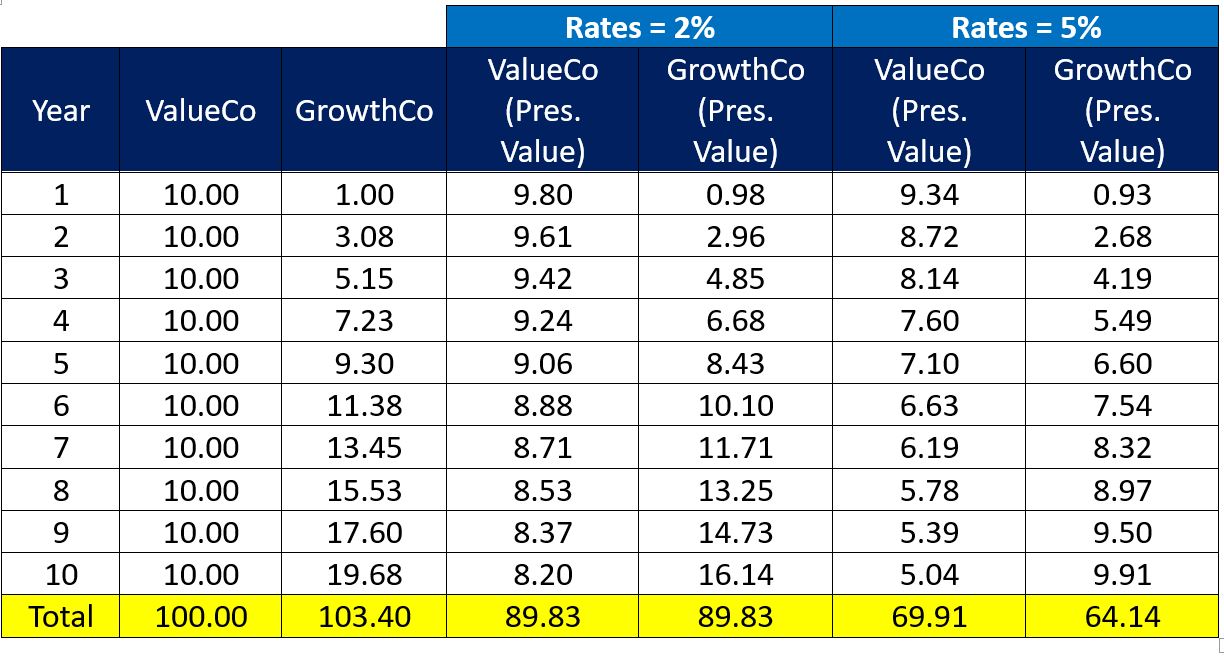

Example: The Effect of Higher Interest Rates on Value vs. Growth Companies

The earnings of the value company are the same every year. In contrast, those of the growth company are smaller at first and then increase over time.

With rates at 2%, the present value of both companies’ earnings over the next 10 years is identical at $89.83.

With rates at 5%, the present value of the value company’s earnings decreases to $69.91 while those of the growth company declines to $64.14.

With no change in the earnings of either company, an increase in rates from 2% to 5% causes the present value of the value company’s earnings to exceed that of its growth counterpart by 9%.

Losing an Illusion makes you Wiser than Finding a Truth

There are several features of the global landscape that will make it challenging for inflation to be as well-behaved as it has been in decades past. Rather, there are several reasons to suspect that inflation may normalize in the 3%-4% range and remain there for several years.

In response to rising geopolitical tensions and protectionism, many companies are investing in reshoring and nearshoring. This will exert upward pressure on costs, or at least stymie the forces that were central to the disinflationary trend of the past several decades.

The unfolding transition to more sustainable sources of energy has and will continue to stoke increased demand for green metals such as copper and other commodities.

ESG investing and the dearth of commodities-related capital expenditures over the past several years will constrain supply growth for the foreseeable future. The resulting supply crunch meets demand boom is likely to cause an acute shortage of natural resources, thereby exerting upward pressure on prices and inflation.

The world’s population has increased by approximately one billion since the global financial crisis. In India, there are roughly one billion people who do not have air conditioning. Roughly the same number of people in China do not have a car. As these countries continue to develop, their changing consumption patterns will stoke demand for natural resources, thereby exerting upward pressure on prices.

Labour unrest and strikes are on the rise. This trend will further contribute to upward pressure on wages and prices.

A Word about Debt

The U.S. government is amassing debt at an unsustainable rate, with spending up 10% on a year-over-year basis and a deficit running near $2 trillion. Following years of unsustainable debt growth (with no clear end in sight), the U.S. is either near or at the point where there are only four ways out of its debt trap: