For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

My latest MoneySense Retired Money column looks at one unexpected upside of inflation; the government’s indexing to inflation of tax brackets, retirement savings limits and OAS thresholds. You can find the full column by clicking on the link here: Inflation a scourge for retirees? Ottawa’s silver lining(s)

TFSA room rises to $7,000

Fans of the popular Tax-free Savings Account (TFSA) will experience this as early as Jan. 1, 2024, when the annual maximum contribution room rises to $7,000, up from $6,500 in 2023. As of January 2024, someone who has never before contributed to a TFSA now has cumulative contribution room of $95,000.

In November Kyle Prevost’s weekly Making Sense of the Markets column included an item titled Make inflation work for you. “We shouldn’t ignore or discount the more advantageous aspects of inflation, such as increased government benefits and more contribution room in our RRSPs and TFSAs.”

Prevost linked to a spreadsheet posted on X (formerly Twitter) by financial advisor Aaron Hector, posted late in October, after the CPI announcement that Ottawa’s official inflation indexing rate for 2024 would be a sizeable 4.7%. While below 2023’s 6.3% indexation rate, it’s well above 2022’s 2.4% and 2021’s 1%.

Also quoted in the MoneySense column is Matthew Ardrey, wealth advisor with Toronto-based TriDelta Financial. “One of the main benefits is paying less taxes.” Income tax brackets increase with inflation each year. For example, in 2021 the lowest tax bracket in Ontario ended at $45,142 of income. “Starting in 2024, this lowest tax bracket now ends at $51,446. This is a 14% increase over just a few years.” Continue Reading…

Image Creator: Fortune Live Media Credit: Fortune The Most Powerful Women

By Noah Solomon

Special to Financial Independence Hub

Warren Buffett is widely regarded as one of the best stock-pickers in history. Among the Oracle of Omaha’s most famous pieces of investment advice is “Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1.”

It goes without saying that when it comes to investing, it is impossible never to lose money. Even the longtime Berkshire CEO has occasionally taken his lumps. This begs the question of what Buffett meant by his statement. To best interpret the Oracle’s words, I took an actions speak louder than words approach and analyzed his historical returns over the past 30 years ending December 2022.

Unsurprisingly, Buffett & Co. trounced the S&P 500 Index, delivering a 13.1% compound annual rate of return vs. 9.6% for the benchmark. Had you invested $1 million with the Oracle rather than in the Index, your investment would have grown to $39,883,361, exceeding the benchmark investment’s value of $15,843,412 by a whopping $24,039,949 (it’s with good reason that people call him the Oracle!).

Moving beyond the headline numbers, the specific pattern of Berkshire’s returns is highly anomalous. In years when the S&P 500 Index had a positive return, Buffett’s performance tended to be undifferentiated. On average, for every 1% the index rose, Buffett’s holdings gained almost exactly the same amount. Clearly, the Oracle’s massive outperformance doesn’t come from knocking the lights out in good times.

In stark contrast, in years when the S&P 500 Index fell, Buffett gained 4.2% on average (no, that’s not a mistake!). This does not mean that the Oracle never loses money. In 2008, Berkshire declined 31.78% vs. 36.0% for the S&P 500. However, in down markets he has either tended to lose far less than the Index or not suffer any losses. The latter occurred during 2000-2002, when the Oracle gained 29.7% vs. a decline of 37.6% for the Index.

John Kelly & Fortune’s Formula: An Unsung Hero of Investing

Very few business school graduates or investment professionals have heard of the Kelly Criterion, which was developed in 1956 by American scientist John Kelly. Despite its relative obscurity and lack of mainstream academic support, the Kelly Criterion has attracted some of the best-known investors on the planet, including “Bond King” Bill Gross, Renaissance Technologies’ James Simons, Warren Buffett, and Charlie Munger (may the great man rest in peace).

The first well-known user of the Kelly Criterion is legendary investor and grandfather of quantitative finance Edward O. Thorp, who referred to it as “fortune’s formula.” He used Kelly’s theory to develop a system for calculating the odds and altering one’s bets accordingly in blackjack, which forever changed the game. Thorp then launched investment firm Princeton Newport Partners (PNP), which produced an annualized return of 15.8%, as compared to 10.1% for the S&P 500 Index. PNP achieved this return with 75% less volatility than the market and lost money in only three of its 230 months in operation.

The Kelly Criterion seeks to maximize long-term wealth by optimally adjusting the amounts of capital to commit to investments as their expected returns and risks fluctuate. Importantly, the formula dictates that you should increase your allocation when the odds are more favorable and curtail your commitment as the odds deteriorate. The imperative of adjusting one’s stance in response to changing circumstances was also espoused by the father of modern macroeconomic theory John Maynard Keynes. When criticized for being inconsistent during a high-profile government hearing, Keynes responded “When the facts change, I change my mind. What do you do, sir?”

Interestingly, this premise stands in stark contrast to the traditional approach to money management, whereby client portfolios maintain a fixed allocation to stocks, bonds, etc., regardless of changes in the market environment or economic backdrop.

What Does John Kelly Have in Common with Warren Buffett?

Having stated that “Our favorite holding period is forever,” Buffett is well known for buying quality companies and holding them for the long term. However, there is another, lesser-known side to the Oracle’s approach which harbors a more than subtle resemblance to Kelly’s.

In her book, “The Snowball: Warren Buffett and the Business of Life,” author Alice Schroeder explains that Buffett’s best opportunities have always arisen during periods of crisis and uncertainty. In Buffett’s view, the opportunity cost of holding cash is low when compelling investment opportunities are few and upside is limited. Conversely, when downside is limited and compelling prospects are abundant (typically during the uncertainty that reigns during or after a market crash), the opportunity cost of holding cash becomes unjustifiably high. At such times, investors should aggressively deploy their cash holdings into assets that offer higher returns. This sentiment is well-summarized by Buffett’s assertion that “Cash and courage in a time of crisis is priceless.” Continue Reading…

As Canadians shop for last-minute gifts and search for deals, our Interac transaction data predicts that the busiest shopping day of the year will fall this year on December 22nd.

According to the transaction data, nearly 27.8 million purchase transactions are expected to take place next Friday (Dec. 22), representing roughly 2.7 million more transactions than the same date last year.

While Canadians are still planning to partake in gift giving, hosting, and more this holiday season, they’re feeling the constraints of today’s economic climate. Recent Interac survey* findings reveal that nearly four in ten Canadian shoppers (38 per cent) say they are feeling the pressure to spend during the holiday season even though their finances are tight.

Our survey revealed this phenomenon is felt as well among newcomers to Canada. Nearly seven in ten newcomers (69 per cent) say they feel more pressure to spend money around the holidays now that they live in Canada. What’s more, 71 per cent say their financial stress during the holidays has grown since moving to this country.

Amid rising prices, the holidays can be a stressful time of year. More than two thirds of Canadians (68 per cent) say they’re stressed about at least one aspect of spending during the holiday season and some sources of stress beat out others. Among those who are stressed, our survey shows us that buying gifts (77 per cent), spending money hosting and entertaining family and friends (41 per cent) and giving money to family members (34 per cent) are the top sources of stress.

For newcomers who are experiencing at least some holiday spending stress (82 per cent), spending money travelling to visit family and friends (48 per cent) is a prominent stressor.

As stressful as holiday spending can be, there are ways to make things a little easier:

Plan ahead

Try creating a gifting budget well in advance of any spending plans to help stay on track. Where possible, you can also look for a sale, consider a refurbished item or tap into purchases that make you and those around you feel good. You can also lean on Interac Debit to track your payments easily and take charge of your own money

Share the love, split the cost

When purchasing gifts for loved ones, organizing festive outings or hosting your family and friends, split the cost using Interac e-Transfer. Sharing the cost is one of the best ways to make sure you’re maximizing fun while staying in control of spending.

Embrace experiences

The holidays are a time to get together with friends and family and enjoy one another’s company. Consider sharing in an experience, rather than giving a physical gift. Interac research shows us that feel-good experiences are more likely to deliver happiness than material goods.

There seems to be some confusion around what to expect for monetary policy in 2024. There’s a strong consensus that cuts are coming, but what is far less certain is how many – and why they are implemented.

Let’s assume that all cuts are of the traditional 25 basis point variety. Since the bank rate is adjusted every six weeks, there will be eight or nine opportunities to adjust it in 2024 in both Canada and the United States.

There are as many as three narratives making the rounds about what might be in store. Each narrative has a combination of rate cuts for monetary policy and corresponding outcomes for the broader economy. I attended a luncheon last week hosted by Franklin Templeton, where senior representatives outlined three possible scenarios with three different narratives accompanying them. A similar perspective was offered earlier this week by the Vanguard Group.

The three narratives are as follows:

#1 We have a soft landing.

The soft landing involves the economy remaining relatively robust, employment remaining strong, delinquency is modest, and rates are normalizing at a level close to but somewhat lower than where they are right now. Most people would suggest that scenario involves no more than two cuts in 2024.

#2 We have a routine recession.

To be more precise, the second narrative involves a garden-variety recession that lasts perhaps a couple of quarters that involves only modest reductions in economic activity over that time frame. Nonetheless, this scenario includes five or six rate cuts to stimulate the economy to the point where things can become stable going forward.

#3 We have a severe recession.

The final narrative involves massive cuts that are made out of desperation to keep the economy from plunging into an abyss. This scenario is not only the most drastic, but also seems to be the least likely. Nonetheless, if things get really ugly, seven, eight or nine rate cuts might be needed to stanch the bleeding. One or more of those cuts might even be for 50 basis points or more.

While I accept the logic associated with all three scenarios, I cannot help but notice that much of the financial services industry is conflating those scenarios in a way that strikes me as being intellectually inconsistent. The financial services industry has long been overly optimistic in the way it portrays outlooks and forecasts. It routinely engages in something I call bullshift, which is the tendency to shift your attention to make you feel bullish about the future.

There can be little doubt that stimulative cuts are positive developments for capital markets. What the industry seems disinclined to acknowledge is that cuts are often made out of desperation. People need to look no further then what happened throughout the entire industrialized world in the first quarter of 2020. Central banks in all major economies cut rates to essentially zero by the end of March of 2020 in the aftermath of the COVID pandemic. At the time it was seen as being both necessary and reasonable, given the severity and breadth of the challenge.

Reining in Inflation

As we all know, inflation became the primary public policy challenge by the beginning of 2022. Central banks needed to take what looked like draconian measures to rein in inflation, which had risen to generational highs and needed to be brought under control lest a sustained period of inflation like what was experienced in the 1970s were to recur. By the end of 2023, inflation is still higher than the high end of the range that is deemed to be acceptable for most central banks.

There is still work to be done, yet many pundits seem eager to take a victory lap, as if a reduction in inflation is somehow akin to bringing inflation under control. Much has been done over the past 20 months, but more work is needed. The admonition that rates will have to stay higher for longer is a very real constraint on economic activity and long-term growth prospects. We head into the new year on the horns of a dilemma. Bond market watchers are now suggesting that rate cuts will come no later than Q2 2024, whereas central bankers are insisting that those cuts will be modest and will only begin in Q3 of 2024 at any rate. They cannot both be right.

It gets worse. Most commentators have taken to suggesting that we will have both a soft landing and five or six rate cuts in the New Year. That strikes me as being fantastic – not to mention intellectually inconsistent. If we have a soft landing, it will likely entail the economy being remarkably resilient as it has been throughout 2023. There is absolutely no reason to have a parade of rate cuts in such an environment.

Stated differently, the financial services industry needs to pick a lane. If it believes we will have a soft landing in 2024, it should also be anticipating a very small number of very modest cuts in the second half of the year. Conversely, if it believes a recession is on the horizon, it should be forecasting multiple cuts only after it is clear a recession is underway. These would likely be needed to stimulate the economy in an environment where inflation will likely be modest as a direct result of economic weakness.

To hear the industry tell it, the economy will remain strong, but we’ll get multiple rate cuts anyway. You can’t have it both ways. I call Bullshift.

John De Goey is a Portfolio Manager with Designed Securities Ltd. (DSL). DSL does not guarantee the accuracy or completeness of the information contained herein, nor does DSL assume any liability for any loss that may result from the reliance by any person upon any such information or opinions.

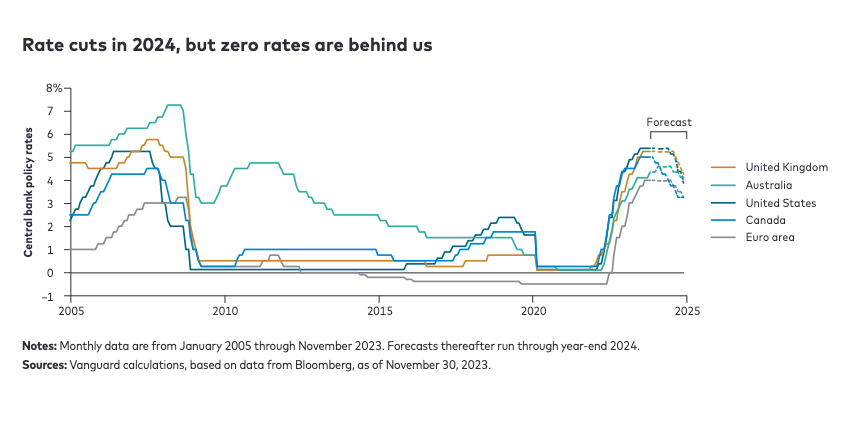

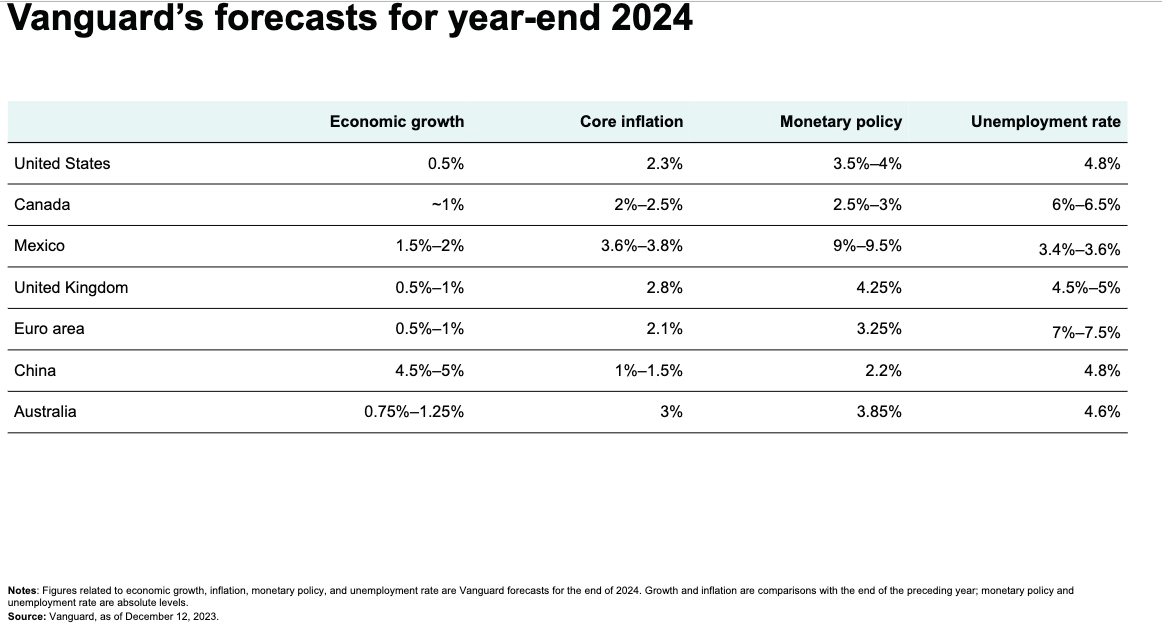

Higher interest rates are here to stay, according to the Vanguard Economic and Market Outlook for 2024, delivered online on Tuesday, Dec. 12. The following is an advance document viewed under embargo and it has been edited down from a Global Summary prepared by Vanguard Global Chief Economist Joseph Davis and the Vanguard global economics team. Anything below in quotes is directly lifted from that document. Otherwise, I have used ellipses and/or paraphrased to make this fit the Hub’s normal blog format. Subheadings are also by Vanguard. At the end of this blog, we have also added a chart about Canada in particular, and projected investment returns in Canada and the rest of the world, supplied by Vanguard Canada.

The main paper begins:

Joseph Davis, Ph.D., Global Chief Economist for Vanguard Group Inc.

“Higher interest rates are here to stay. Even after policy rates recede from their cyclical peaks, in the decade ahead rates will settle at a higher level than we’ve grown accustomed to since the 2008 global financial crisis (GFC). This development ushers in a return to sound money, and the implications for the global economy and financial markets will be profound. Borrowing and savings behavior will reset, capital will be allocated more judiciously, and asset class return expectations will be recalibrated. Vanguard believes that a higher interest rate environment will serve investors well in achieving their long-term financial goals, but the transition may be bumpy.”

Monetary policy will bare its teeth in 2024

“The global economy has proven more resilient than we expected in 2023. This is partly because monetary policy has not been as restrictive as initially thought. Fundamental changes to the global economy have pushed up the neutral rate of interest — the rate at which policy is neither expansionary nor contractionary. Various other factors have blunted the normal channels of monetary policy transmission, including the U.S. fiscal impulse from debt-financed pandemic support and industrial policies, improved household and corporate balance sheets, and tight labor markets that have resulted in real wage growth.

In the U.S., our analysis suggests that these offsets almost entirely counteracted the impact of higher policy interest rates. Outside the U.S., this dynamic is less pronounced. Europe’s predominantly bank-based economy is already flirting with recession, and China’s rebound from the end of COVID-19-related shutdowns has been weaker than expected.

The U.S. exceptionalism is set to fade in 2024. We expect monetary policy to become increasingly restrictive as inflation falls and offsetting forces wane. The economy will experience a mild downturn as a result. This is necessary to finish the job of returning inflation to target. However, there are risks to this view. A “soft landing,” in which inflation returns to target without recession, remains possible, as does a recession that is further delayed.

In Europe, we expect anemic growth as restrictive monetary and fiscal policy lingers, while in China, we expect additional policy stimulus to sustain economic recovery amid increasing external and structural headwinds.”

Zero rates are yesterday’s news

“Barring an immediate 1990s-style productivity boom, a recession is likely a necessary condition to bring down the rate of inflation, through weakening demand for labor and slower wage growth. As central banks feel more confident in inflation’s path toward targets, we expect they will start to cut policy rates in the second half of 2024.

That said, we expect policy rates to settle at a higher level compared with after the GFC and during the COVID-19 pandemic. Vanguard research has found that the equilibrium level of the real interest rate, also known as r-star or r*, has increased, driven primarily by demographics, long-term productivity growth, and higher structural fiscal deficits. This higher interest rate environment will last not months, but years. It is a structural shift that will endure beyond the next business cycle and, in our view, is the single most important financial development since the GFC.”

A return to sound money

“For households and businesses, higher interest rates will limit borrowing, increase the cost of

capital, and encourage saving. For governments, higher rates will force a reassessment of fiscal

outlooks sooner rather than later. The vicious circle of rising deficits and higher interest rates

will accelerate concerns about fiscal sustainability.

Vanguard’s research suggests the window for governments to act on this is closing fast — it is

an issue that must be tackled by this generation, not the next.

For well-diversified investors, the permanence of higher real interest rates is a welcome

development. It provides a solid foundation for long-term risk-adjusted returns. However, as the

transition to higher rates is not yet complete, near-term financial market volatility is likely to

remain elevated.

Bonds are back!

Global bond markets have repriced significantly over the last two years because of the transition

to the new era of higher rates. In our view, bond valuations are now close to fair, with higher

long-term rates more aligned with secularly higher neutral rates. Meanwhile, term premia

have increased as well, driven by elevated inflation and fiscal and monetary outlook

uncertainty.

Despite the potential for near-term volatility, we believe this rise in interest rates is the single

best economic and financial development in 20 years for long-term investors. Our bond

return expectations have increased substantially. Continue Reading…