For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

Here’s a Look at the Best Investments to Hold in a TFSA – and Why

Image via Deposit Photos

We recently had a question from a member of Pat McKeough’s Inner Circle that asked:

“Pat, I hold Intel in a non-registered account with a capital loss showing and am thinking of transferring it to my TFSA “in kind” with no tax penalty. Is Intel a suitable stock to hold in a TFSA?”

We’re not tax experts, so you might want to consider talking to an expert, especially if there are large funds involved.

However, transferring shares in kind into a TFSA does trigger a capital gain or loss for income tax purposes.

If the investment is in a capital gains position, you will have to declare it as a capital gain on your income tax return. But if there is a capital loss, you will not be able to declare the loss for tax purposes. This is because the government still sees you as the beneficial owner of the security.

Note that if you sell the shares in a non-registered account, you can deduct your loss against capital gains. For example, if he were to sell his Intel shares in 2023, he’d get to deduct the loss against his 2023 capital gains.

If you still have capital losses left over, you can carry them back up to three years (2022, 2021 and 2020), or forward indefinitely to offset future capital gains.

Hold Lower-Risk Investments in a TFSA

We think it is best to hold lower-risk investments (such as blue-chip stocks we see as buys like Intel) in your TFSA. That’s because you don’t want to suffer big losses in these accounts. If you do, you can’t use those losses to offset capital gains, as is the case with taxable (non-registered) accounts. You’ll also lose the main advantage of a TFSA: sheltering gains from tax. You won’t have gains to shelter if the value of your investments falls. Continue Reading…

Around the middle of December, advisory firms and the people who work for them start putting out their retrospectives regarding the year that is just about to end and / or offer their forecast for the new year. I have long argued that forecasting is a mugs game. To the extent that I have grudgingly participated in the exercise previously, I have found it to be humbling. As such, I want to stress that what follows is not so much a forecast as it is a concern for what may – and I stress MAY – come to pass in light of what we already know about the incoming administration south of the border.

To begin, the President-elect is a criminal. He has literally been convicted of 34 felonies. This is in addition to two impeachments, various infidelities, an attempted insurrection, and the stealing of highly classified state secrets. We now have a good sense of what his cabinet will look like: assuming most of his forthcoming nominees are ultimately appointed. This is a man who is quite willing to appoint incompetent sycophants who will help him expand his ongoing criminal activity at the expense of more traditional character traits like relevant education, experience, and character. The notion of traditional public service seems to be foreign to many would-be cabinet appointees.

Will Trump manufacture a Recession?

Early in December, I was in Southern California and spoke with the founder of an AI company in Silicon Valley. He told me there is a theory making the rounds that Donald Trump intends to do something highly unconventional in his longstanding pursuit personal self-interest. The executive told me that a number of thought leaders are of the opinion that Trump intends to deliberately manufacture a recession immediately upon taking office.

Their view is that, given the experiences of both the global financial crisis and the COVID crisis, it has become apparent that when the economy is severely threatened and bailouts are required, billionaires and plutocrats end up doing very well. Meanwhile, ordinary middle-class people and those even lower on the social spectrum fall further behind.

In the aftermath of the election on November 5th, American capital markets responded favorably based on the presumption that lower taxes and less regulation would be highly stimulative and favourable for the economy. This view held sway even though the President-elect campaigned on a platform of indiscriminately-high tariffs, mass deportations, and a draconian cutting of government services via the department of government efficiency (DOGE).

There are some who fear that the promise to rein in the debt will be used as an excuse to cut back on government programs that ordinary Americans rely on. As it stands, approximately three quarters of all U.S. annual expenditures are fixed in law and allocated toward entitlements such as Medicare, Medicaid, and Social Security, as well as interest on the national debt.

Cutting US$2 trillion from the budget is simply impossible without encroaching on at least some of these programs. Stated differently, even if Trump were to cut all other programs (including the CIA in the SEC) to zero, the savings would still be less than the $2 trillion a year he pledged to cut. He will, of course, blame Joe Biden for “the mess he inherited” either way.

No fiscal Conservatives left in America

Meanwhile, the evidence shows that for over half a century, the U.S. accumulated debt has been growing under both major parties. It seems there are no fiscal conservatives left in America. Again, I stress, this is not a forecast, but rather a recounting of a narrative that several thoughtful people who live south of the border believe to be plausible. If you think wealth inequality and income inequality are a problem now, you could be in for a rude awakening if anything close to this narrative comes to pass.

As many people know, I have long been a proponent of efficient capital markets. Any person who espouses this view believes that prices reflect all available information to the point where it is impractical to think that mispricings are sufficiently large and identifiable so as to allow people to engage in trading that would allow that person to make material profit. The American stock market clearly does not subscribe to the narrative I’ve just outlined. Of course, consensus opinions can be wrong. In this instance, perhaps more than any other in my lifetime, I actively want the consensus to be correct. Continue Reading…

I’m just sitting on a fence

You can say I got no sense

Trying to make up my mind

Really is too horrifying

So I’m sitting on a fence

The Rolling Stones

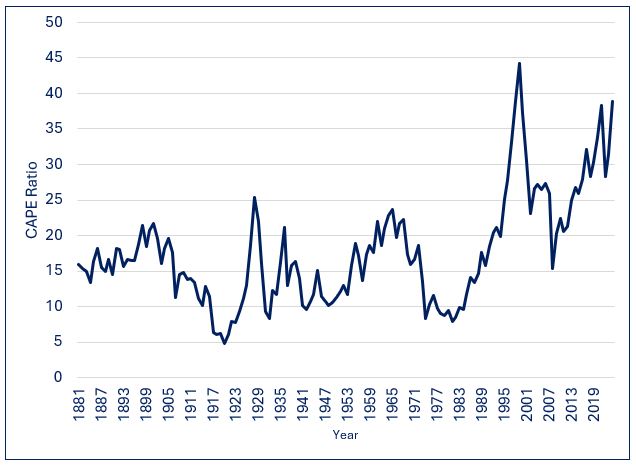

Benjamin Graham and David Dodd are universally regarded as the fathers of value investing. In their 1934 book “Security Analysis” they introduced the concept of comparing stock prices with earnings smoothed across multiple years. This long-term perspective dampens the effects of expansions as well as recessions. Yale Professor and Nobel Prize winner Robert Shiller later popularized Graham and Dodd’s approach with his own version, which is referred to as the cyclically adjusted price-to-earnings (CAPE) ratio.

S&P 500 CAPE Ratio: 1881- Present

Since 1881, the CAPE ratio for U.S. equities has spent about half of the time between 10 and 20, with an average and median value of about 16. Its all-time low of 5 occurred at the end of 1920, and its high point of 45 occurred at the end of 1999 during the height of the internet bubble.

What if I told you …. ?

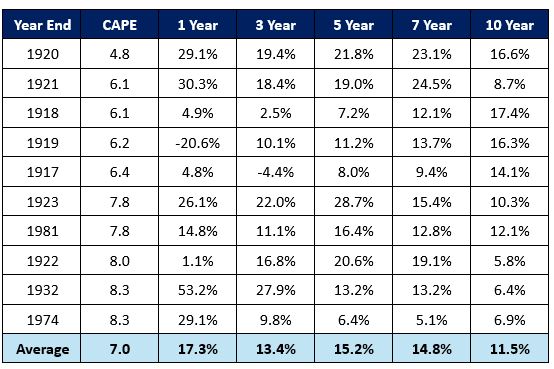

The following table shows average real (after inflation) annualized returns following various CAPE ranges.

S&P 500 Index: CAPE Ratio Ranges vs. Average Annualized Future Returns (1881 Present)

What is abundantly clear is that higher returns have tended to follow lower CAPE ratios, while lower returns (or losses) have tended to follow elevated CAPE levels. An investment strategy that entailed having above average exposure to stocks when CAPE levels were low, below average equity exposure when CAPE levels were high, and average allocations to stocks when CAPE levels were neither elevated not depressed would have resulted in both less severe losses in bear markets and higher returns over the long-term.

By no means does this imply that low CAPE ratios are always followed by periods of strong performance, nor does it imply that poor results are guaranteed following instances of elevated CAPE levels. That would be too easy!

S&P 500 Index: Lowest CAPE Ratios vs. Future Real Returns (1881 – Present)

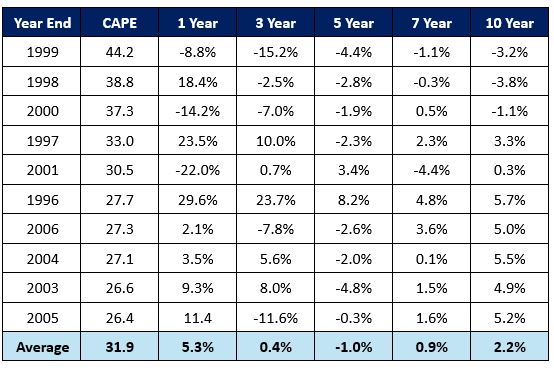

S&P 500 Index: Highest CAPE Ratios vs. Future Real Returns (1881 – Present)

Looking at the performance of stocks following extreme CAPE levels, it is clear that valuation is best used as a strategic guide rather than as a short-term timing tool. It is most useful on a time scale of several years rather than a shorter-term timing tool.

Although there have been instances where low CAPE levels have been followed by weak performance over the next 1-3 years, there have been no instances in which average annualized returns over the next 5-10 years have not been either average or above average. While it sometimes takes time for the proverbial party to get started when CAPE levels hit abnormally depressed levels, markets have without exception performed admirably over the medium to long-term.

Similarly, although there have been instances where high CAPE levels have been followed by strong performance over the next 1-3 years, there have been no instances in which average annualized returns over the next 5-10 years have not been either below average or negative. Whenever CAPE levels have been extremely elevated, it has only been a matter of time before the valuation reaper exacted its toll on markets. This brings to mind the following quote from Buffett:

“After a heady experience of that kind, normally sensible people drift into behavior akin to that of Cinderella at the ball. They know that overstaying the festivities — that is, continuing to speculate in companies that have gigantic valuations relative to the cash they are likely to generate in the future — will eventually bring on pumpkins and mice. But they nevertheless hate to miss a single minute of what is one helluva party. Therefore, the giddy participants all plan to leave just seconds before midnight. There’s a problem, though: They are dancing in a room in which the clocks have no hands.”

Be the House, Not the Chump

There have been (and inevitably will be) times when equities post strong returns for a limited time following elevated CAPE levels and instances where stocks post temporarily weak results following depressed CAPE levels.

However, successful investing is largely about playing the odds. If you were at a casino, wouldn’t you prefer to be the house rather than the chump on the other side of the table? Although chumps occasionally get lucky, this doesn’t change the fact that the odds aren’t in their favour and that they are playing a losing game. Over the long-term, investors who refrain from reducing their equity exposure when CAPE levels are elevated and don’t increase their allocations to stocks when CAPE levels are depressed will achieve satisfactory returns over extended periods. That being said, I sure wouldn’t recommend such a static approach for the simple reason that it involves suffering severe setbacks in bear markets and leaving a lot of money on the table over the long-term.

Given the historically powerful relationship between starting CAPE levels and subsequent returns, what if I told you that the CAPE ratio currently stands at 38, putting it at the top 98th percentile of all year-end observations going back over 150 years, and the top 96th percentile over the past 50 years? Presumably you would at the very least consider taking a more cautious stance on U.S. stocks.

Let’s Pretend ….

Let’s pretend that you knew nothing about the historical relationship between CAPE levels and subsequent returns. A combination of behavioural biases, speculative fervour, and FOMO (fear of missing out) might lead you to adopt an “if it isn’t broken, don’t fix it” stance of inertia.

Recency bias can give people a false sense of confidence that what has occurred in the recent past is “normal” and is therefore likely to continue in the future. Moreover, the strong returns which have occurred since the global financial crisis can exacerbate FOMO, thereby prompting investors to stay at the party (and perhaps even to imbibe more intensely by increasing their equity exposure). Lastly, the potential of innovative technologies such as AI to revolutionize businesses can capture investors’ imaginations and incite euphoria to the point where they believe that there is no price that is too high to pay for the unlimited profit potential of the “shiny new toy.”

Standing at the Crossroads

So here we stand at a crossroads, caught between the weight of history and the possibility that this time it may truly be different. What is an investor to do? One can never be 100% sure. The “right” answer will only be known in hindsight once it becomes a matter of record, at which point it will be too late for investors who get caught on the wrong side of the fence. Continue Reading…

A Tax Free Savings Account (TFSA) is far more versatile and powerful than you might think.

Now that we’re into the start of a new year (Happy New Year!) here are some great things you can do with your TFSA.

TFSA Backgrounder

The TFSA was first introduced in the 2008 federal budget.

It became available to Canadians for the 2009 calendar year – as of January 1, 2009. Launched part-way through The Great Recession (where markets collapsed significantly during 2008 triggered by a financial crisis), the account was designed as a savings account (hence the name) to encourage Canadians to save more money.

But the “savings” word in the name is very misleading, no?

Correct.

Since account introduction in 2009, adult Canadians have had a tremendous opportunity to save and grow their wealth tax-free like never before.

As with an RRSP, the TFSA is intended to help Canadians save money and plan for future expenses. The contributions you make to this tax-free account are with after-tax dollars and withdrawals are tax-free. Consider it like an RRSP account in reverse.

For savvy investors who open and use a self-directed TFSA for their investments, these investors can realize significant gains within this account. This means one of the best things about the TFSA is that there is no tax on investment income, including capital gains!

How good is that?!

Let me tell you … here is summary of many great account benefits:

Capital gains and other investment income earned inside the account are not taxed.

Withdrawals from the account are tax-free.

Neither income earned within a TFSA nor withdrawals from it affect eligibility for federal income-tested benefits and credits, like future Old Age Security (OAS) income.

Anything you withdraw can be re-contributed in a following year, in addition to that year’s contribution limit.

While you cannot contribute directly as you could with an RRSP, you can give your spouse or common law partner money to put into their TFSA. Do it without any income attribution!

TFSA assets could be transferable to the TFSA of a spouse or common-law partner upon death. More details below for you.

The annual contribution limit is indexed to inflation in $500 increments, that happened in recent years …. and more!

I’ve got my preference for which account I focus on for wealth-building purposes (related to the RRSP vs. TFSA debate, including what account I would suggest you max out your contributions to first) but let’s compare each first:

RRSP

TFSA

A tax-deferral plan.

A tax-free plan.

Contributions can be made with “before-tax” dollars as part of an employer-sponsored plan or “after-tax” dollars when a contribution is made with a financial institution.

Contributions are made with “after-tax” dollars.

Contributions are tax deductible; you will get a refund roughly equal to the amount of multiplying your contribution by your tax rate.

Contributions are not tax deductible; there is no refund to be had.

If you don’t contribute your maximum allowable amount in any given year you can carry forward contribution room, up to your limit.

If you make a withdrawal, contribution room is lost.

If you make a withdrawal, amounts withdrawn create an equal amount of contribution room you can re-contribute the following year.

Because contributions weren’t taxed when they were made (you got a refund), contributions and investment earnings inside the plan are taxable upon withdrawal. They are treated as income and taxed at your current tax rate.

Because contributions were taxed (there was no refund), contributions and investing earnings inside the account are tax exempt upon withdrawal.

Since withdrawals are treated as income, withdrawals could reduce retirement government benefits.

Withdrawals are not considered taxable income. So, government income-tested benefits and tax credits such as the GST Credit, Old Age Security (OAS) and the Guaranteed Income Supplement (GIS) aren’t affected by withdrawals.

You can’t contribute to an RRSP after age of 71. Accounts must be collapsed in the 71st year.

You can contribute to a TFSA after age of 71.

The Summary: part of your RRSP is borrowed money (i.e., you owe the government taxation.)

The Summary: all of your TFSA is your money.

Based on my personal investment plan, I feel the TFSA ultimately trumps the RRSP as a retirement vehicle to focus on first at any income level even though I contribute to both every year. All the money in the TFSA is mine to keep, grow and manage with no taxation withdrawal consequences.

Since inception, here are the annual and cumulative limits assuming no withdrawals over that period were made:

TFSA contribution limit 2009 to 2025:

Year

TFSA Annual Limit

TFSA Cumulative Limit

2009

$5,000

$5,000

2010

$5,000

$10,000

2011

$5,000

$15,000

2012

$5,000

$20,000

2013

$5,500

$25,500

2014

$5,500

$31,000

2015

$10,000

$41,000

2016

$5,500

$46,500

2017

$5,500

$52,000

2018

$5,500

$57,500

2019

$6,000

$63,500

2020

$6,000

$69,500

2021

$6,000

$75,500

2022

$6,000

$81,500

2023

$6,500

$88,000

2024

$7,000

$95,000

2025

$7,000

$102,000

Based on the recent bull run in recent years, I know some individuals that have over $200,000in their TFSAs.

I also know some couples who have their combined TFSA assets worth more than $400,000 in value.

Pretty impressive tax-free money!!

Q&A with Mark – What has worked for me/us over the years?

Well, we’ve bought various assets, namely Canadian stocks and ETFs over the years.

To date, we have avoided any TFSA withdrawals. Instead, like I referenced above, we use our TFSAs for owning equities and wealth-building purposes.

Q&A with Mark – What types of investments can you own inside the TFSA?

Thankfully lots!

Similar to the assets you can hold within a Registered Retirement Savings Plan (RRSP), the TFSA can also be used to help Canadians build significant wealth beyond just holding cash savings. You can own a number of different types of investments inside the TFSA: Continue Reading…

No matter what goes on in the news, Washington or the world, to build a stable tomorrow, we must take control of our own lives. Even with all the current upheaval, here are five things you can do today to empower yourself.

Track spending

This is the number one most useful financial technique to implement today. Imagine if businesses did not track their expenses. How would they know the financial health of their enterprise? It is no different for you and me. It is paramount to know where your money is going and what percentage of your net worth you are spending.

Know your net worth

Assets minus Liabilities equals Net Worth. Place a value on everything you own and subtract what you owe. This figure is your net worth. Now divide how much you spent last year by your net worth number and you will have your percentage of spending to net worth. Continue Reading…