By Noah Solomon

Special to Financial Independence Hub

Crazy People is a 1990 American comedy starring Dudley Moore and Daryl Hannah. Moore plays advertising executive Emory Leeson. Leeson experiences a nervous breakdown, which causes him to design a series of “truthful” advertisements that are blunt and bawdy.

By mistake, his ads get printed and turn out to be a tremendous success. One of Leeson’s more memorable campaigns is for Volvos, which includes the tagline “Volvo — they’re boxy but they’re good.”

Dividend-paying stocks are like the Volvos of the investing world. They are not fancy or exciting, nor do they produce windfall profits over the short term. However, they have a lot going for them when you take a deeper look under the hood.

This month, I explore the historical performance of dividend-paying stocks, including the conditions under which they have tended to outperform their non-dividend-paying counterparts. Relatedly I will also discuss whether the current market environment is supportive of future outperformance.

A Caveat to the Volvo Analogy: Having your Cake and Eating it Too

The “Volvo — they’re boxy but they’re good” tagline implies a clear tradeoff: the suggestion being that one needs to sacrifice performance for reliability. However, the historical data imply that this has not been the case with dividend-paying stocks. Not only have they exhibited greater stability than their non-dividend-paying counterparts, but they have also produced higher returns, thereby providing investors with a “have your cake and eat it too” proposition.

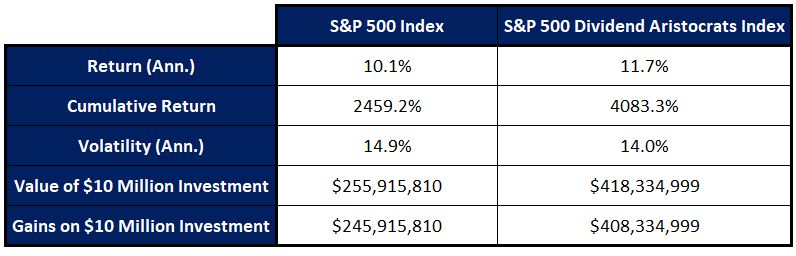

S&P 500 Index vs. S&P 500 Dividend Aristocrats Index (1990 – Present)

Since the beginning of 1990, the S&P 500 Index Dividend Aristocrats Index has produced an annualized total return of 11.7% vs. 10.1% for the S&P 500 Index. This difference in annualized performance has amounted to a tremendous difference in cumulative long-term returns, with the S&P 500 Dividend Aristocrats Index producing a cumulative return of 4,083% vs. a far less impressive 2,459% for the S&P 500 Index. In dollar terms, a $10 million investment in the S&P Dividend Aristocrats Index would have produced $408,334,999 in returns, which is 1.66 times more than the corresponding figure of $245,915,810 for the S&P 500 Index.

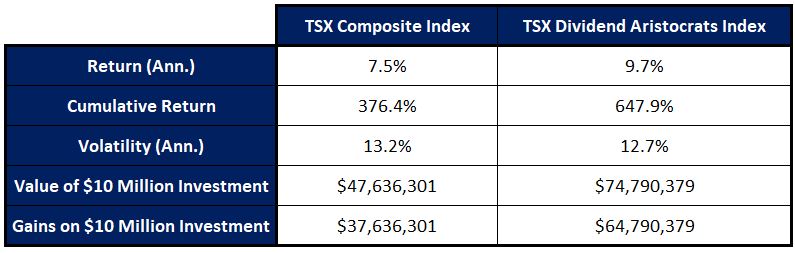

TSX Composite Index vs. TSX Dividend Aristocrats Index (2002 – Present)

The numbers for Canada tell a similar story, albeit over a shorter period due to historical data limitations for the TSX Dividend Aristocrats Index. Since 2002, the TSX Dividend Aristocrats Index has produced an annualized total return of 9.7% vs. 7.5% for the TSX Composite Index. In terms of cumulative performance, the TSX Dividend Aristocrats has produced a total return of 647.9% vs. 376.4% for the TSX Composite Index. In dollar terms, a $10 million investment in the TSX Dividend Aristocrats Index would have produced $64,790,379 in returns, which is 1.72 times more than the corresponding figure of $37,636,301 for the TSX Composite Index.

As an aside, the tremendous difference from 1990 to the present in the 2,459% cumulative return for the S&P 500 Index and that of 1,120% for the TSX Composite Index is largely attributable to the former’s far larger weighting in technology stocks. Between 1990 and 2010, the two markets were neck and neck, with the S&P 500 delivering a total return of 457% vs. 453% for the TSX. Since then, the S&P 500 went on to crush its northern neighbour, with a total return of 359% vs. 120%. During the same period, the mega-cap tech-heavy Nasdaq 100 knocked the lights out, returning 675%.

Tech stocks, and in particular mega-caps, have experienced tremendous earnings growth and trade at premium valuations. Whether their rates of growth continue, or premium multiples will persist, is beyond the scope of this commentary. That being said, there is no guarantee that these trends will persist, and relatedly whether the U.S. stocks will continue to outperform their Canadian counterparts.

Nice to Have in Strong Markets and Essential in Others

Dividends have historically been an integral part of equity market returns. Going back to 1990, a full 52.2% of the total return of the S&P 500 Index since 1990 can be attributed to the power of compounding reinvested dividends. On a relative basis, Canadian dividends have been even more prominent than U.S. ones, with reinvested dividends responsible for an astounding 63.3% of the total returns of the TSX Composite index.

Although dividends’ contributions to total market returns have been substantial over the past several decades, this contribution has tended to vary substantially over shorter sub-periods. As the table below demonstrates, dividends tend to play a smaller role in times of strong price appreciation. By contrast, during periods when capital gains have been muted, dividends play a far more substantial role in overall returns.

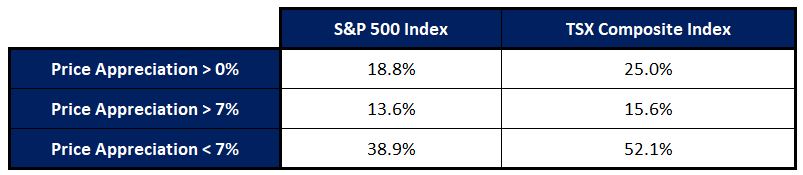

Contribution of Dividends to Total Returns: Rolling 12-Month Periods (1990 – Present)

Taking all 12-month rolling periods since 1990 in which the S&P 500 experienced price appreciation, dividends on average accounted for 18.8% of total returns. However, in periods where prices rose by 7% or more, dividends were responsible for only 13.6% of the total return pie vs. 38.9% when prices rose between 0% and 7%.

In Canada, the relative importance of dividends has also varied with capital gains. In all rolling 12-month periods since 1990 in which the TSX Composite Index experienced price appreciation, dividends were on average responsible for 25% of total returns. In those periods where prices rose by more than 7%, dividends’ share of total returns was only 15.6% as compared to 52.1% when prices rose between 0% and 7%. Continue Reading…