By Nick Barisheff

By Nick Barisheff

Special to the Findependence Hub

Over time, most investment dealers have implemented misguided policies that will negatively affect their clients’ investment portfolios and their ability to achieve a secure retirement.

There are two main policies that have negative impacts on investors’ portfolios. One is restricting investments to a client’s original Risk Tolerance in the Know Your Client application form (KYC). When opening an account, the client will advise the dealer of their Risk Tolerance. Most clients will indicate that they are medium risk. On March 8, 2017, the Ontario Securities Commission (OSC) implemented risk rating rules that require all mutual funds to rate their fund according to 10-year standard deviation. In 2018, I published an article entitled New Mandatory Risk Rating is Misleading Canadian investors.

Prior to the OSC’s implementation of the risk rating rules, on December 13, 2013, the OSC issued CSA Notice 81-324 and Request to Comment – Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts. My comments on this policy were submitted to the OSC on March 12, 2014, along with comments from 50 other industry experts.

I presented a paper to the OSC that argued that Standard Deviation is not an appropriate measure of risk, since the best-performing mutual fund and the worst-performing mutual fund in Canada had the same Standard Deviation. The measure of Standard Deviation of an investment does not reduce the risk of incurring losses.

A better, more accurate methodology would have used downside standard deviation or the Sharpe or Sortino ratios which measure risk adjusted returns. Nevertheless, the OSC implemented risk rating rules requiring all mutual funds to rate the risk of their funds according to 10 year standard deviation.

As a result, if investments in a client’s portfolio exceeded the risk tolerance as indicated in the original KYC, the client was forced to redeem those investments, by the advisor’s compliance department. A number of BMG’s clients were forced to redeem their positions since our funds had a medium-high risk rating according to the OSC formula, and the clients’ KYC indicated medium-risk tolerance. A number of clients wanted to change the KYC in order to allow them to maintain ownership of our funds but were advised that, unless there was a significant change in their financial circumstances, they could not change their KYC.

The second policy that dealers have implemented is Concentration Risk. Clients are not allowed to hold more than 25% in any one investment. If the investment rises and exceeds 25% units are redeemed to reduce their holdings back to 25%. If clients want to add more than 25% the client would need to provide a written trade authorization that would have to be approved by the compliance department. Many investors have investments outside of their brokerage accounts such as real estate and GICs. In that case concentration limits are set to 10% of Investable assets.

As a result, a significant number of clients have terminated their advisors and opened discount brokerage accounts. We refer to these clients as the Do It Yourself (DIY) investors. Not only do DIY investors save money due to lower management fees, they are able to make their own investment decisions without interference, foregoing financial advice. We have a dedicated web page – BMG DIY Investor – designed specifically for these independent investors.

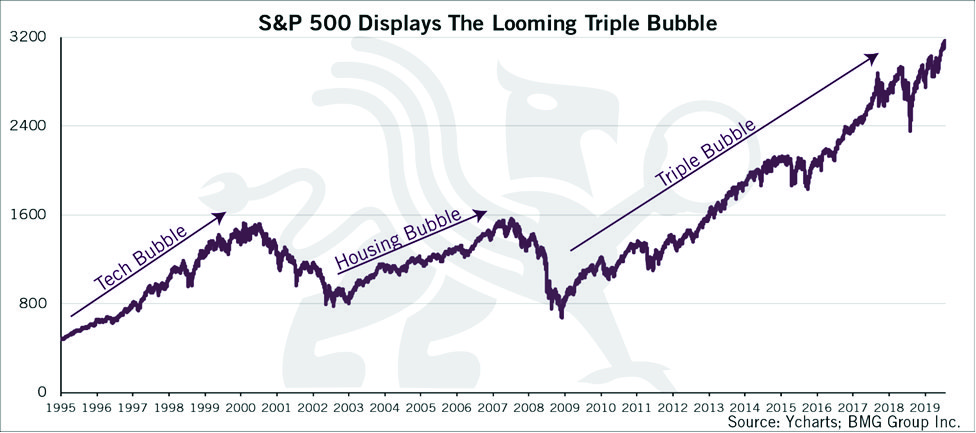

Today, many investors are concerned about the economic challenges facing them. They realize that the equity markets are the most overvalued and longest-running in history and are vulnerable to a major correction.

As a result they are exposed to losses of 50% to 70% in their equity investments according to a number of analysts. Apart from equities, the fixed income part of their portfolios will also experience significant losses if central banks raise interest rates to fight inflation.

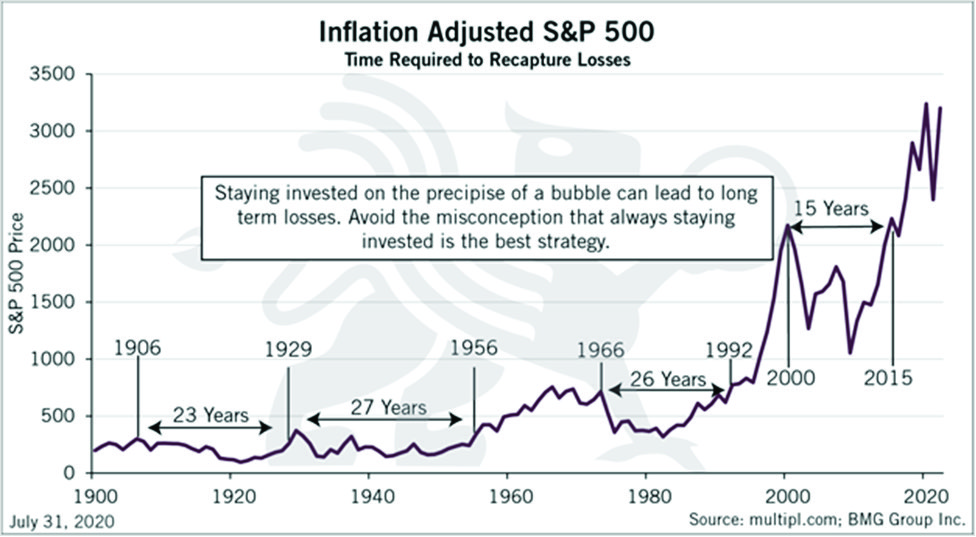

While holding a mix of 60/40 of stocks and bonds may have generated good results during the past 10 years, it is unlikely to be repeated during the next 10 years. Moreover, if markets experience a major correction it will take a long time just to break even.  The 1929 Crash took 27 years to break even and the Dot Com Crash took 15 years to break even. Retired baby boomers may not live long enough to break even after this crash.

The 1929 Crash took 27 years to break even and the Dot Com Crash took 15 years to break even. Retired baby boomers may not live long enough to break even after this crash.

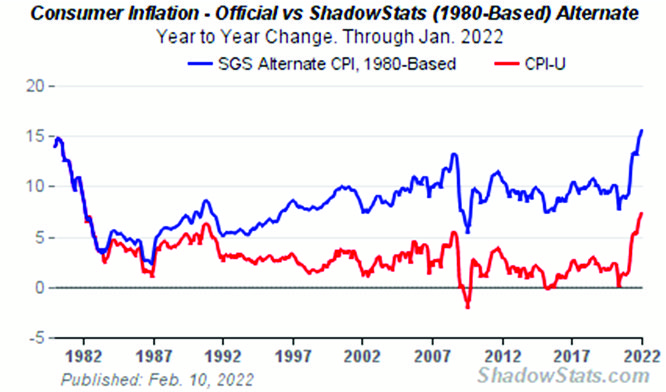

Investors are also concerned about the loss of purchasing power of their investments. Official inflation is now 7.9%; that translates to 15% using Shadowstats methodology.

The reality is that, unless the portfolio is generating returns in excess of the inflation rate, the investor is losing purchasing power.

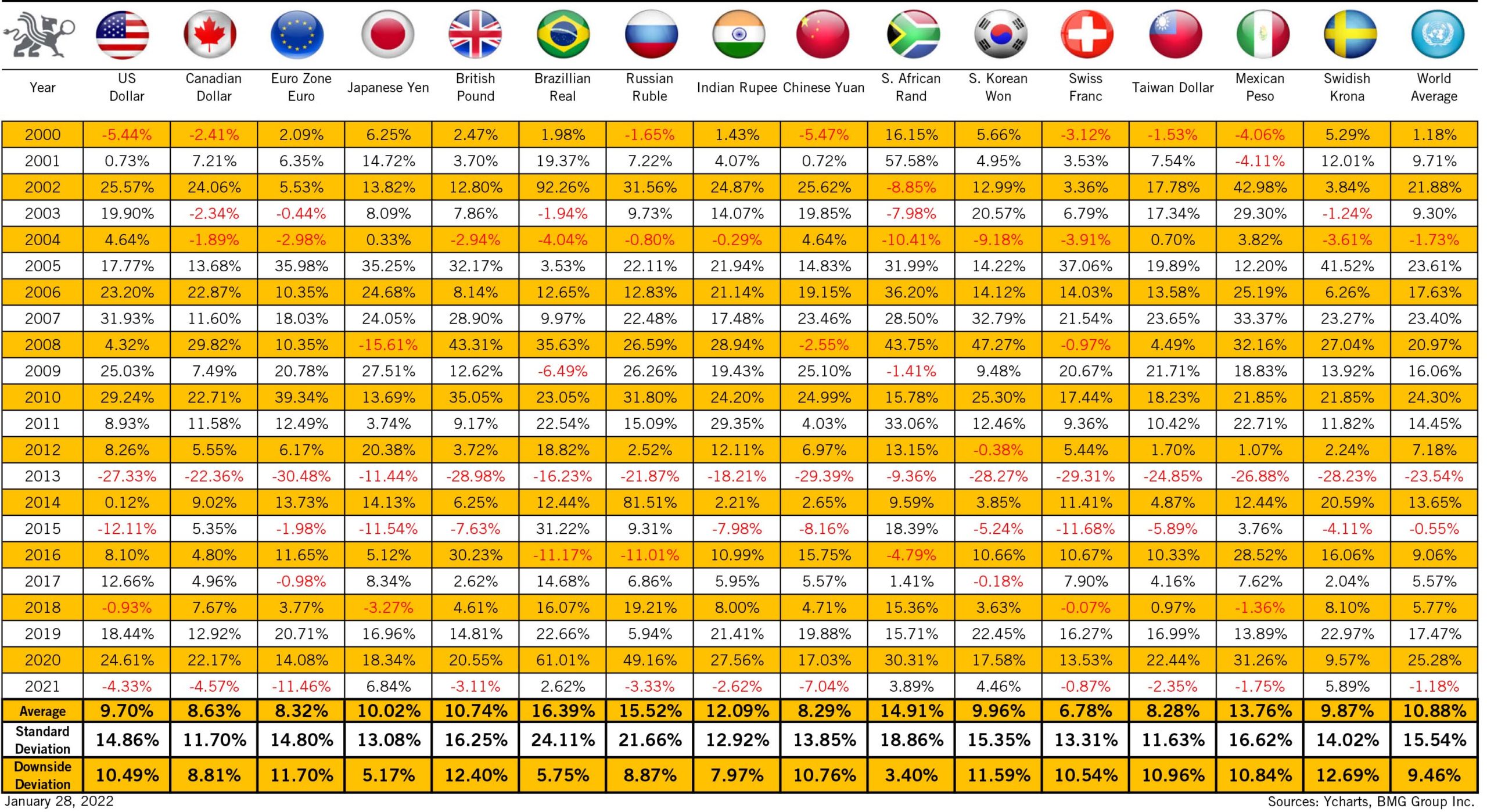

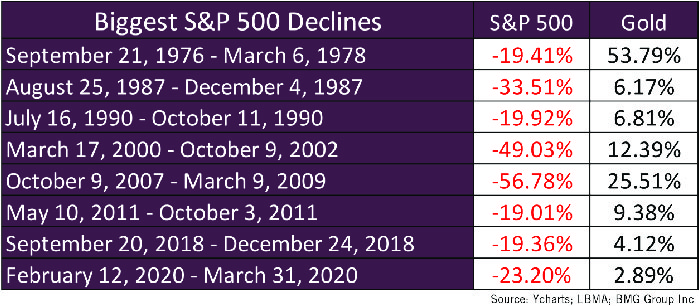

Precious metals have performed well, rising 6.7% this year to the 1st of March. Over the past twenty years gold has averaged over 11% per year in all currencies, as can be seen in this chart:

In addition, gold has performed exceptionally well during market declines.

Compliance departments hold the mistaken notion that precious metals funds are a risky asset, and therefore limit client holdings to 25%. They do not differentiate between mining stock funds and bullion funds. These two categories of precious metals mutual funds have completely different risk profiles. Their view on the risks of gold bullion contradicts the major regulatory authorities such as the Bank of International Settlements (BIS), which regulates global central banks. The BIS considers gold a zero risk monetary asset.

In addition, compliance departments base their risk decision based on standard deviation rather than considering the current economic and geopolitical risks. This is a mistaken notion, as gold has a lower standard deviation and a higher return than most of the DOW components.

In summary, investors are faced with rising inflation, overvalued equity and bond markets, and risk significant losses to their portfolio that may take years just to break even. Under normal financial conditions it is difficult to build an adequate retirement nest egg. Today however, portfolios need to be adjusted to compensate for current conditions. Many advisors who are trying to protect their clients by increasing their gold allocations in their portfolios are frustrated by these compliance policies as they also believe that, in this environment, portfolios should hold in excess of 25% in bullion.

The Permanent Portfolio which was developed in the 1970 calls for 25% allocations to Equities, Bonds, Real Estate and Gold. The Permanent Portfolio has outperformed the 60/40 portfolio during the past 20 years.

While I wrote my book $10,000 Gold – Why Gold’s Inevitable Rise is the Investors Safe Haven in 2013, today I firmly believe that gold will achieve this level and that investors will not only face devastating losses in their investment portfolio, but also miss out on a once-in-a-lifetime investing opportunity.

Nick Barisheff is the founder, president and CEO of BMG Group Inc., a company dedicated to providing investors with a secure, cost-effective, transparent way to purchase and hold physical bullion. BMG is an Associate Member of the London Bullion Market Association (LBMA) as well signatory to the Six Principles of Responsible Investments (United Nations endorsed Principles for Responsible Investment – PRI).

Nick Barisheff is the founder, president and CEO of BMG Group Inc., a company dedicated to providing investors with a secure, cost-effective, transparent way to purchase and hold physical bullion. BMG is an Associate Member of the London Bullion Market Association (LBMA) as well signatory to the Six Principles of Responsible Investments (United Nations endorsed Principles for Responsible Investment – PRI).

Widely recognized as international bullion expert, Nick has written numerous articles on bullion and current market trends that have been published on various news and business websites. Nick has appeared on BNN, CBC, CNBC and Sun Media, and has been interviewed for countless articles by leading business publications across North America, Europe and Asia. His first book, $10,000 Gold: Why Gold’s Inevitable Rise Is the Investor’s Safe Haven, was published in the spring of 2013. Every investor who seeks the safety of sound money will benefit from Nick’s insights into the portfolio-preserving power of gold. www.bmg-group.com This article was originally published published in March 2022. It is republished on the Hub with permission.

The information contained in this article provides a general overview of subjects covered, and the expressed personal views and opinions are not intended to be taken as advice regarding any product, organization or individual, and should not be relied upon as such. Consult your investment and legal advisors regarding specific coverage issues. Information and opinions expressed in this article are provided without warranty of any kind, either express or implied, including, without limitation, warranties of merchantability, fitness for a particular purpose, and non-infringement. BMG uses reasonable efforts to include accurate and up-to-date information from public domains and sources but does not make any warranties or representations as to its accuracy or completeness. BMG assumes no liability or responsibility for any errors or omissions in the content of this article.