Generation X, and to a lesser extent the Millennials, are already starting to feel the retirement squeeze, according to a Franklin Templeton-sponsored survey released Thursday.

Generation X, and to a lesser extent the Millennials, are already starting to feel the retirement squeeze, according to a Franklin Templeton-sponsored survey released Thursday.

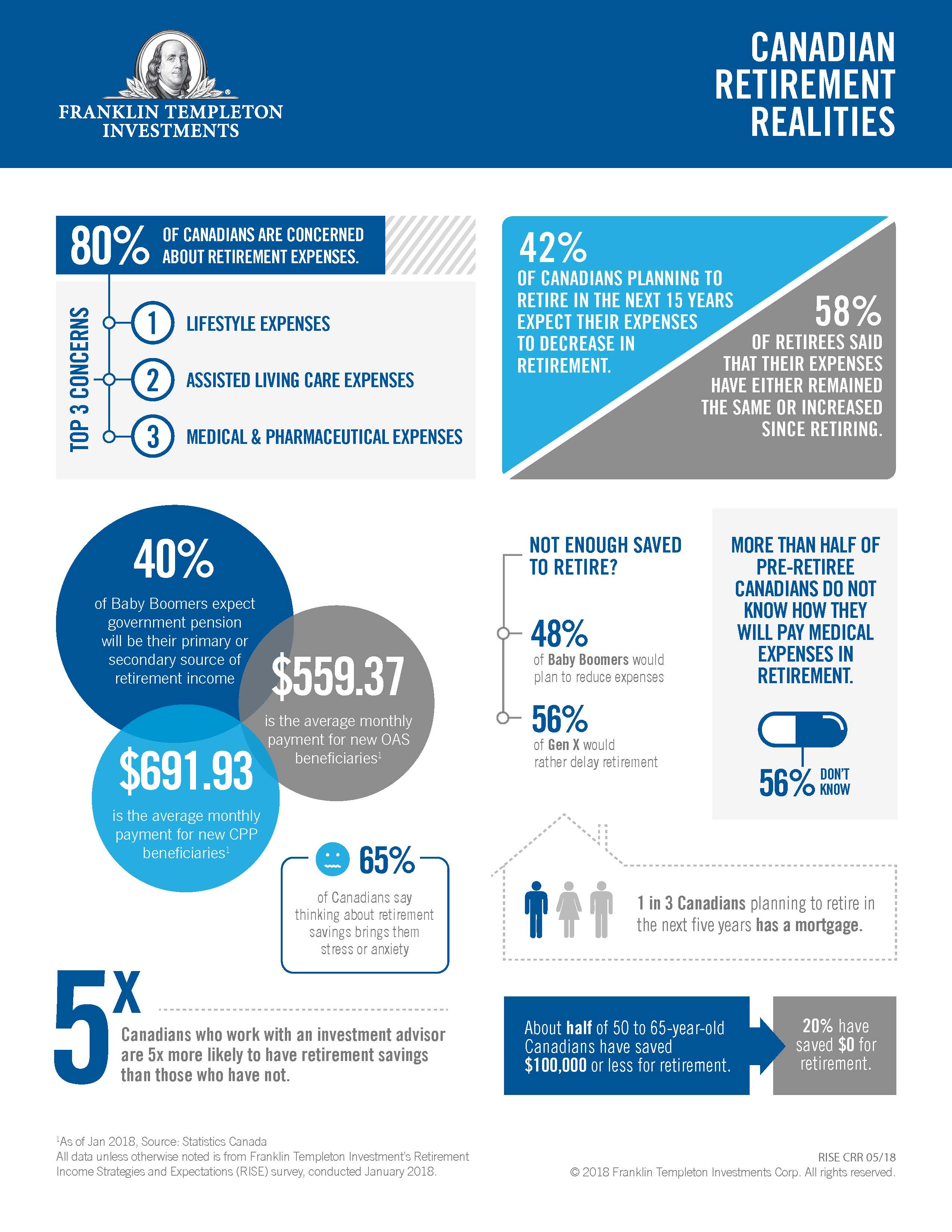

Details are in my column in Friday’s Financial Post, which you can retrieve by clicking on the highlighted headline here: Generation X is ‘stretched beyond their financial limits’ and struggling to save for Retirement.

The challenges should be familiar to members of any generation (four are mentioned in the survey): it’s never easy saving money when you’re starting out in life with low wages and high expenses. But Franklin Templeton cautions against the rationalization embraced by younger investors that they simply can choose to keep on working if they haven’t accumulated enough assets to generate adequate income in retirement.

That may not always be an option, since ill health or corporate downsizing (to mention just two) may prevent this. You can find full details about the fifth annual edition of Franklin Templeton Investments Canada’s 2018 Retirement Income Strategies and Expectations (RISE) survey here.

Stressed GenX resigned to retiring later than hoped

More than half of Gen Xers (aged 37 to 52) are resigned to retiring later than they would want (56% in Canada, 59% in the US). While the online survey included Canadians and Americans across four generations, “this year we felt in particular that Gen X and the stress of preparing for Retirement was the predominant thing coming out of the research,” said Matthew Williams, a Franklin Templeton senior vice president, in an interview.

Millennials (currently aged 18 to 36) also fret about lack of retirement saving but they have a bit more time to get their acts together and start saving. In fact, since 28% of Millennials are still living with their parents or their spouse’s parents, you could argue they’re not even out of the starting gate for financial independence. On the other hand, living at home should give them a leg up in paying down debt (whether student loans or credit cards) since their expenses should be (presumably) minimal. And temporary though the arrangement may be, it’s also an opportunity to sock money saved on rent into a Tax-free Savings Account (TFSA), the better to come up with a down payment for a first home.

And as I say in my financial novel, Findependence Day, a paid-for home is the foundation of Financial Independence. The trick is to get into the automatic saving habit as early as you can. Life is always expensive, which is why young people have to practice what the characters in the book call “guerrilla frugality.”

Yes, the Boomers had some advantages: homes were relatively inexpensive when we were starting out, even though interest rates were sky-high, so we were motivated to pay them down as soon as possible. They can be sold tax-free at today’s much higher prices but even then you have to live somewhere: downsizing to a condo perhaps or to the country.

Some but certainly not all Boomers benefited from Defined Benefit employer pensions; in fact, the survey finds that already-retired boomers are almost twice as likely to rely on employer pensions (39% of them do), than non-retired boomers (21%).

Great Post!

Time for service providers and oversight to treat what retail investors are able to cobble together with slot more respect?! Instead of viewing these nest eggs as folder for their industry profit machines

As for condos being the frugal solution for downsized think again given stiff hikes on fees to offset replacing elevators and other necessary repairs coming due. You can anticipate this will be a huge issue given the times the government encouraged condo development and when it didnt

Further since when was an elevator part of ordinary households upkeep

Unit owners are still responsible for replacing acing kitchens and bathrooms etc

Do the math