By Penelope Graham, Zoocasa

Special to the Financial Independence Hub

For those trying to scrape together a down payment in Canada’s hottest housing markets, the Home Buyer’s Plan is known as an effective tool. Offered by the federal government, it allows first-time buyers to pull funds from the RRSPs completely tax-free to put toward their home down payment. If you’re lucky enough to have RRSP matching via your employer, or have been saving for retirement for some time, it can seem an especially attractive method to amass down payment funds.

However, there are a few restrictions buyers should be aware of:

- Buyers must have a signed Agreement of Purchase and Sale to buy or build a property before applying to access the funds.

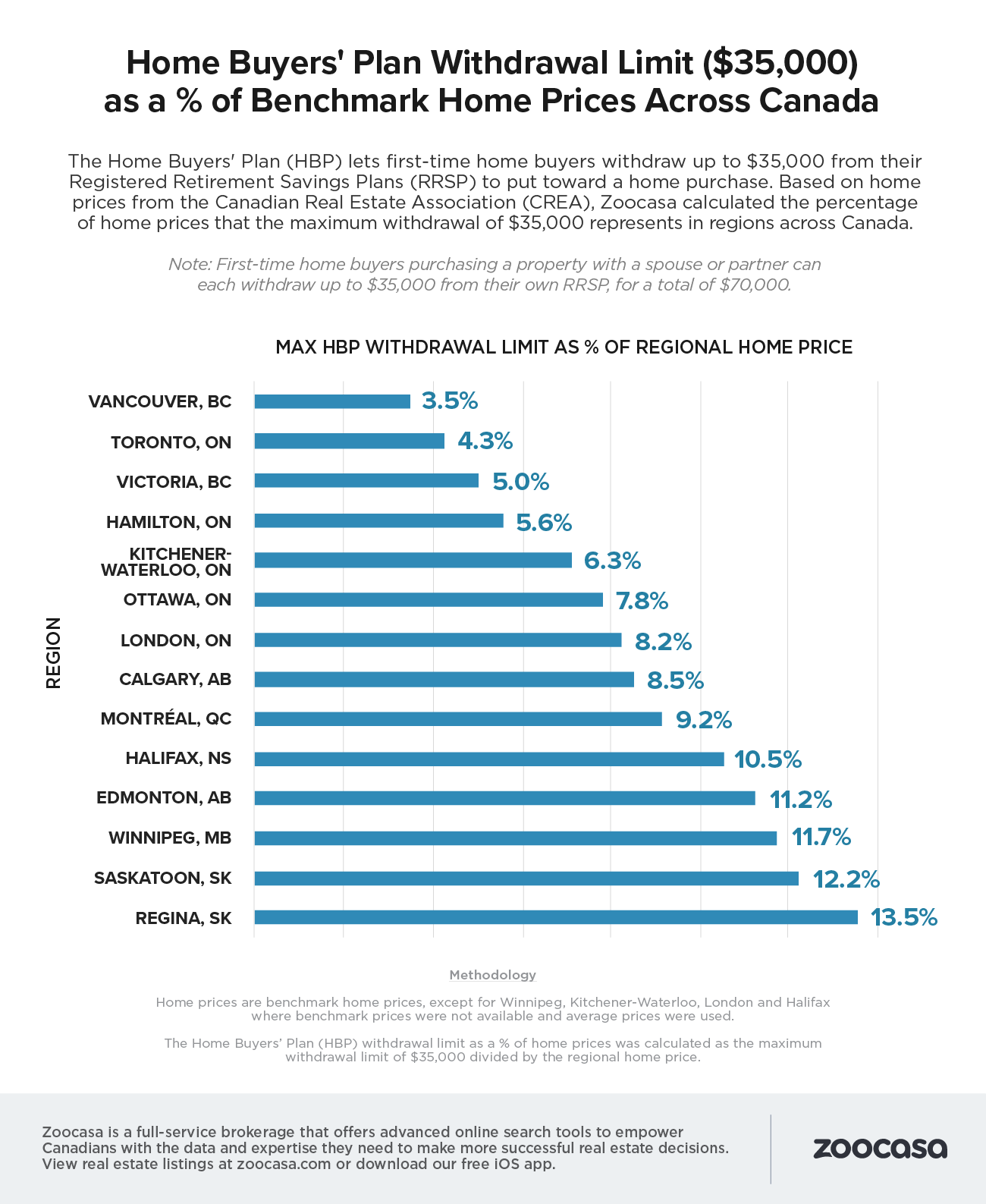

- They can pull up to a limit of $35,000 from an individual’s RRSP, and up to a combined $70,000 from RRSPs held by two individuals buying together (assuming the funds are saved in the first place).

- The funds must have been sheltered within the RRSP for a minimum of 90 days before they can be accessed.

- Buyers are required to “pay themselves back”, contributing one fifteenth of the withdrawn amount on an annual basis over a 15-year timeline, or be taxed on that portion at their full rate.

- Buyers must qualify as “first timers,” which the Government of Canada defines as not having owned a home, or occupied one that your spouse has owned, in the four consecutive years before this home purchase is made. (However, there are exceptions in the case of a marriage or common-law relationship breakdown where former partners can restore their first-time buyer status.)

- Buyers must intend to dwell in the home as their permanent residence within one year of its purchase or completion.

How long would it take to actually save for the HBP?

Assuming a buyer satisfies all the criteria above, they also need to actually save the funds in the RRSP in order to use them for their home purchase: and that’s easier said than done in some urban centres than others.

To see how long it would take to actually set aside the maximum $35,000 in an RRSP, Zoocasa sourced individual income thresholds in 14 cities across the nation. The data was based on 2017 tax filings as reported by Statistics Canada, and assumed the income was earned income, eligible to create RRSP contribution room, and that individuals contributed the maximum to their RRSP annually (18% of earned income, to a maximum of $26,500). The study also compared how long it would take for those in the top 50%, 25%, and 10% income groups to save $35,000.

According to the findings, for a median-income household contributing the max amount to an RRSP, it would take between 4.3 – six years to pull together $35,000.

(See Infographic at the top of this blog).

How far would $35,000 go in your Housing market?

As well, the extent that the maximum HBP funds would actually aid in a home purchase varies across Canada; it’s no surprise that in the priciest markets, such as homes for sale in Toronto or Vancouver, that it’s hardly a drop in the bucket – just 4.3% and 3.5% of a benchmark home price, respectively.

Its effectiveness remains limited in Ontario’s secondary real estate destinations such as the Hamilton, London, and Kitchener real estate markets, accounting for 5.6%, 8.2%, and 6.3%, respectively.

In fact, those really looking to get the most bang for their buck using the HBP are best to look to the Prairie markets, as $35,000 would go towards a whopping 13.5% of a home in Regina, 12.2% in Saskatoon, and 11.7% in Winnipeg.

Penelope Graham is the Managing Editor at Zoocasa, a full-service brokerage that offers advanced online search tools to empower Canadians with the data and expertise they need to make more successful real estate decisions. View real estate listings on zoocasa.com or download our free iOS app.