Are you trying to succeed with investments? Our Successful Investor approach teaches these 3 key rules we teach to subscribers.

TSInetwork.ca

Successful investors try to arrange their portfolios so that they more-or-less automatically tap into the profit and long-term growth that inevitably comes with well-established companies.

And now is a particularly good time to follow our Successful Investor investment approach. Our system of the most successful investment strategies has three key rules:

Rule #1: Invest mainly in well-established, profitable, dividend-paying stocks.

Our first rule in the most successful investment strategies will help you stay out of high-risk, low-quality investments. These investments are always available, in good and bad markets. They come with hidden risks due to conflicts of interest and other negatives. Every year, they lead many inexperienced investors to substantial losses.

Recent standout losers include bitcoin and other cryptocurrencies; a disappointing crop of new issues (IPOs), which tend to come to market when it’s a good time for the new-issue company or its insiders to sell, but not a good time for you to buy; and slapped-together promotional stocks that hit the market thanks to the SPAC phenomenon, which offers a short cut to IPO status.

Rule #2: Spread your money out across most if not all of the five main economic sectors.

This is our key to successful diversification. The widely disparaged resource sector turned out to have some major winners last year, in Canadian oil and gas stocks. Nutrien Ltd., our top fertilizer recommendation, shot up in early 2022 as the Russian invaded Ukraine, which put a big dent in world grain supplies.

On the other hand, if you had disregarded resource stocks with the intention of doubling down on tech stocks, you might have wound up with excessive holdings in tech stocks just as they entered a plunge.

Rule # 3: Downplay or avoid stocks in the broker/media limelight.

We’ve recommended a handful of tech stocks and other broker/media favourites in the past few years, but we always advised against concentrating on them.

Rather than zero in on broker/media favourites, we prefer to apply our first and second rules. If you build a balanced, diversified portfolio of high-quality stocks, it’s hard to go too far wrong, even in a challenging year like 2022 that we’ve recently experienced.

Understanding successful investments

A successful investment is one that provides long-term gains for its investors. Profitability will mean different things to many investors. One key to making a successful investment is you need to disregard or at least downplay investment marketing messages. Continue Reading…

For those who depend on investments to provide a portion of their yearly income, 2022 has been a tough slog, to say the least; but take heart: it’s almost over.

Of course, no one can say with certainty that 2023 will be better. Persistently high inflation, ongoing central bank monetary tightening and the increasing likelihood of a recession have made for volatile markets, and this uncertainty could continue well into next year.

Under the circumstances, it’s not surprising that weary investors have poured money into GICs (guaranteed investment certificates) and other cash equivalents. Even with today’s higher interest rates, however, returns remain well below the inflation rate, and unless held in registered accounts, they are fully taxable. Liquidity can also be problematic as most GICs require a locked-in period, with penalties for redeeming before maturity. If you need flexibility, you’ll pay for it with lower returns.

Reliable income requires diversification

Without doubt, GICs have their place: but the proverbial advice about placing all your eggs in one basket still applies. Diversification is as important for income portfolios as it is for equities, and the sources of income should be as uncorrelated to each other as possible. One way to easily bump up the level of income diversification is through a managed program (sometimes referred to as a wrap account) which bundles together different investment vehicles, strategies, styles and portfolio managers in one or more “umbrella” portfolios directed by a governing team of portfolio managers.

20 years of income generation

One of the earliest programs managed in Canada was Franklin Templeton’s Quotential program; in fact, this year marks the program’s 20th anniversary. Of its five globally diversified, actively managed portfolios, the aptly named Quotential Diversified Income Portfolio (QDIP) is designed to generate high, consistent income from multiple uncorrelated sources. Canadian and international fixed income assets form the core of the portfolio, but for added flexibility and performance enhancement, about one-quarter of the portfolio is invested in blue-chip Canadian and international equities selected for their income-generating dividend yields and long-term growth potential.

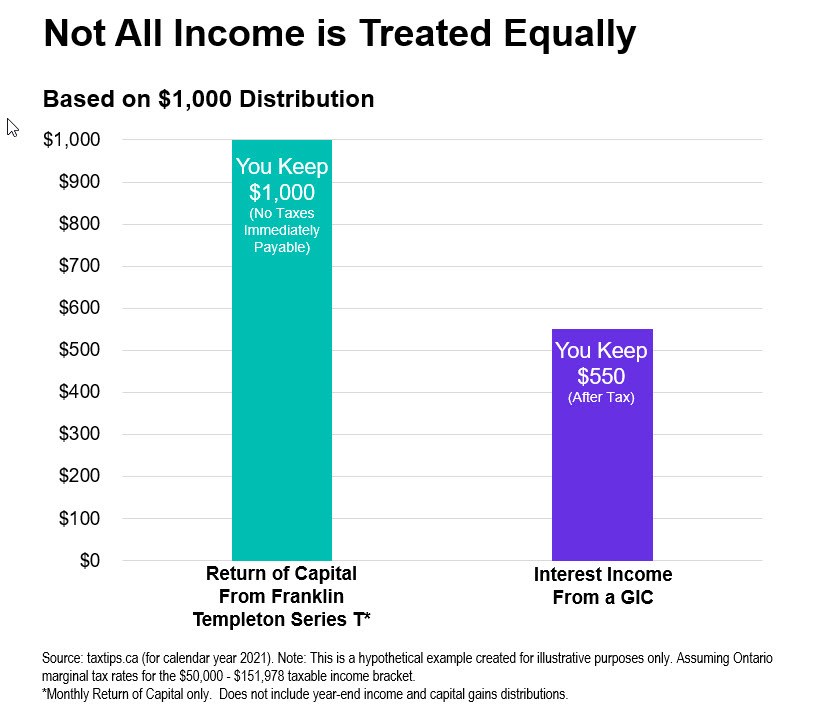

“T” is for Tax Efficient

Reliability solves much of the income puzzle, but an important missing piece is the tax burden. Taxes can eat away at the income generated from investments, especially if you are still earning a salary or receiving significant income from other sources. All Quotential portfolios are available in Series T, which offers a predictable stream of cash flow through monthly return of capital (ROC) distributions. From a tax perspective, ROC is treated more favourably than interest or dividend income. The tax efficiency also extends to the tax deferral of capital gains that can help you better plan for when you pay tax. For snowbirds and others who spend extended periods south of the border, distributions from Series T are available in U.S. dollars for a number of funds, including Quotential Diversified Income.

It’s important to stress that with Series T, capital gains taxes are deferred, not eliminated. Continue Reading…

The IPO or “Initial Public Offerings” market — more commonly known as the new issues market — has gone through an extraordinarily bad time this year. It’s been bad for all three of the groups that take part in this market. They are as follows:

Investors who put their money in new issues have lost substantial sums in the past year. On average, new stock issues tend to do worse than the rest of the market in their first few years of public trading. This past year, they performed much worse than ever.

Financial institutions that bring new issues to market for sale to investors have suffered, too, because demand for new issues has dried up. At this time of year in 2021, the new issues market had raised around $100 billion. So far this year, it has raised just $5 billion. In the past quarter century, the new issues market raised an average of $33 billion at this point in the year.

Companies that raise capital for themselves through the new issues market are suffering as well. When the new issues market began drying up as a source of corporate funding, many would-be issuers of new stocks found it was harder and more expensive than ever to find alternate sources of financing.

This will be worst year for IPOs since 2009

This will be the worst year for raising money in the new issues market since 2009, when the economy was struggling to pull out of the 2008/2009 recession.

As long-time readers know, we generally advise staying out of new stock issues. After all, there’s a random element in the success or failure of every business, especially when it’s just starting out. But new issues expose you to a special risk that you avoid with stocks that have been trading publicly for some time. That is, you can only invest in new issues when they come to market.

This is just one more example of a conflict of interest, which we’ve often referred to as the worst source of risk you face as an investor.

Companies only come to the new issue market to sell their stock when it’s a good time for the company and/or its insiders to sell. The insiders can’t predict the future, of course. However, they do know much more than outsiders do about their company. Continue Reading…

After nearly two years of a global pandemic, capped by surging inflation, the past month has been dominated by Russia’s invasion of Ukraine and a wave of geopolitical uncertainty unleashed by the largest European conflict since 1945.

“What a crazy decade these past two years have been,” is a line making the rounds on social media at the moment.

In the midst of all this volatility, uncertainty, and tension, we believe it’s important to focus on quality investments. We should begin by understanding and defining quality within our unique philosophy at Harvest ETFs. We can then outline some of the strategies at work in our Harvest ETFs that protect against volatile times and how today’s shocks fit in a longer-term macro-outlook.

Be diversified and own quality

To begin, our view remains that you want to be diversified and you want to own quality. How do you measure quality though? At Harvest, we do it through financial metrics like variability of earnings, visibility into earnings, return on invested capital and others. What those metrics tell us is that large-cap companies have the ability to navigate tail risks.

While risks related to geopolitical tension are top of mind now, we should emphasize that supply chain issues, inflation, and interest rate transitions are arguably the biggest volatility risks now. In this uncertain environment, it’s important to prepare for volatility from a wide range of sources. The expectations for how much and how quickly interest rates will rise is also going to be volatile and will likely result in some sectors doing better at different times, more so than what we have seen in recent history. Volatility shouldn’t come as a surprise if we’re adequately prepared for it with an investment approach that focuses on quality & diversity.

Our focus on quality is a core element of the Harvest investment philosophy. That philosophy focuses on leading companies in specific sectors or mega trends as the best place for investors to be if they want long-term capital appreciation prospects and income across market cycles.

Income Generation and Covered Calls

Income generation is another core element of the philosophy at work in Harvest’s equity income ETFs. That is achieved through a covered call strategy, generating a premium by agreeing to sell up to 33% of a holding at a set price. Using an active covered call strategy, Harvest’s team of portfolio managers generate consistent and high yields on their ETFs. As well, the value of call options tends to increase when volatility and uncertainty increase. The premiums generated by the covered call strategy act as some downside protection by the premium received. Continue Reading…

Most investors do not like volatility. They do not like looking at their investment account balance observing that they’ve ‘lost money.’

Of course, you have not lost money until you buy an asset at a certain price and then sell at a lower price. You’ve then just realized your losses. You have not lost money when your portfolio value goes down. And in fact, swings in portfolio values are just par for the course. Stocks and bonds and real estate change in price (with wild swings at times) in regular fashion: it’s normal behaviour. If the stock markets have you spooked, there is a simple and timeless plan of action.

With this strategy, you can ‘win’ if stocks go up. You can win if stocks go down. It’s a strategy that worked during the worst period in stock market history: the Great Depression of the 1930s .

The answer of course is adding money on a regular schedule. In the investment world they call it dollar cost averaging; we can abbreviate that to DCA. There is no need to guess about which way the market is going to go today, next week, next month, next year, or even the next five years. We simply expect or hope that the markets will go up over longer periods, as they have throughout history.

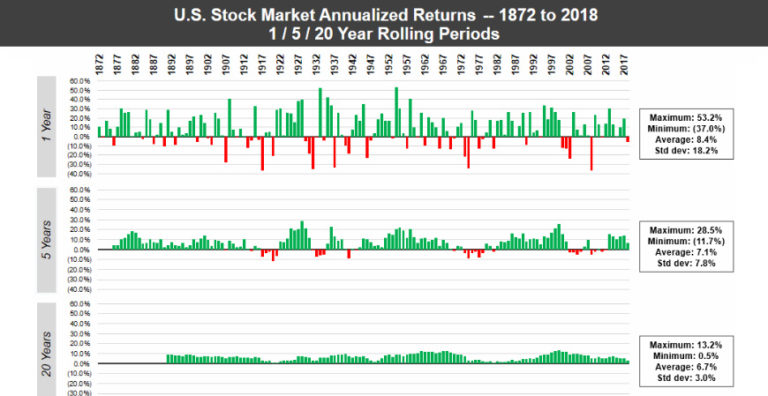

Stock market history

U.S. stocks, S&P 500

You can see that there is lots of green on the board. Stocks mostly go up. It is those pink years (on the table) that usually trip up many investors

The key to long-term wealth building is being able to invest through those down years. And in fact, adding money in those years is quite beneficial as the stocks go on sale.

But keep in mind that stocks can stay under water for extended periods.

Dollar cost averaging

Now this is a consideration for those who have very little exposure to stocks, or who have been out of the markets for quite some time. That event is not as rare as you might think. Many investors have left the markets, though they recognize that they need to be invested to reach their financial goals and enjoy a prosperous retirement. They also want their wealth protected from inflation.

Here’s the demonstration: investing through the initial stages of the Great Depression.

In the above charts we see equal amounts invested, but the dollar cost averaging strategy still delivered positive returns in a vicious bear market. Buying at those lower prices was very beneficial. Now keep in mind for the above to work, the markets have to go up over time. They have to recover. And historically they have.

Time reduces risk

Here is a wonderful graphic that demonstrates the returns over various periods. Our odds increase as we lengthen the time period that we remain invested.

And a table that frames the probabilities of positive returns.

Charlie Bilello

Spread out that lump sum

If you are sitting on a large sum that you want to get invested you will have to have a plan. Over what time period should you get those monies into the market?

If you start investing and the markets keep going up, great. Mission accomplished. The money you’ve invested has increased in value. You are collecting dividends along the way.

But of course when we enter a stock market correction, your total portfolio value will decline. Though you might get enough of a head start so that your money invested remains in positive territory.

At that point when markets are declining, remember that lower prices are good. The stocks are going on sale. And of course, you do not have to invest in an all-equity portfolio. You can dollar cost average into a balanced portfolio.

I’d suggest that you spread the money out over 2 or 3 years. For example, If you are on the 2-year plan and have $100,000 to invest and you’re investing every month, you’d invest $4,167 per month.

You can’t time the markets

For those who already have substantial assets invested, you can’t move in and out of the markets. We don’t know when the corrections will occur. The most reasonable course of actions is still dollar cost averaging. That said, whenever you have money to invest, stock market history says get it invested. The sooner the better.

This is key. If you get scared and sell, you might lose money.

You might have to accept a lower-risk portfolio that is likely to earn less over time compared to a more aggressive stock-heavy portfolio or balanced portfolio. It’s also possible that you do not have the risk tolerance to invest (at all), even in a very conservative ETF portfolio. If that is the case you would have to stick with GICs and high-interest savings accounts. You might add to your real estate exposure for growth. In retirement, you might use annuities to boost your income.

For savings we use EQ Bank. 3-and 6-month GIC’s now 2.05%

To help gauge your risk tolerance level and the appropriate level of portfolio risk, please have a read of the core couch potato portfolios on MoneySense. You’ll find a table within that post that breaks it down.

If you are risk averse, you likely need a managed portfolio and advice. You might consider a Canadian Robo Advisor. These investment companies provide lower-fee portfolios at various risk levels. Advice is also included. A few of these firms also offer financial planning.

At Justwealth, you get access to advice and financial planning. In fact, you’ll have your own dedicated advisor.

They will do a risk evaluation to see if investing is right for you, and then you will be placed in the appropriate portfolio(s). And once again, you’ll be offered the greater financial plan as well.

Start investing

Preet [Banerjee] puts some of the above in video form [YouTube.com]. Preet also goes over how much you might market over various time frames, at different rates of return.

The key is to not be frozen on the sidelines. We might refer to that as ‘paralysis by analysis’.

Build wealth at your own comfort level, at your own pace. You will learn as you go. You can build up your comfort level for risk and volatility. It’s quite possible that you can increase your risk tolerance level over time. We develop risk callouses.

Thanks for reading. We’ll see you in the comment section. If you’re not sure what to do, feel free to flip me a note.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on Feb. 12, 2022 and is republished on the Hub with his permission.