![]()

By Kyle Prevost, MillionDollarJourney

Special to the Financial Independence Hub

So you have been reading Million Dollar Journey (MDJ) for years, have used your Canadian online broker account to DIY-invest your way to a solid nest egg.

You’ve got a TFSA, and RRSP, and maybe even a non-registered account – full of good revenue-generating assets.

Kudos!

Now comes the tough part: How do you turn that nest egg into a usable stream of money that you can spend as you enter retirement?

Surprisingly, when it comes to discussing Canadian safe retirement withdrawal rates, and talking to folks who have retired at all ages, spending their retirement savings represented a massive mental strain for them. I guess (as someone who has never retired or sold investments to pay for retirement) that I always thought that saving for retirement would be the hard part.

Isn’t spending supposed to be more fun than squirreling away?

It turns out that once you get into that savings mindset, it can be hard to flip the switch back to enjoying spending the fruits of your labour. This is especially true for folks who are looking at strategies for an early retirement because they are much more likely to have been super-aggressive savers during their time in the workforce.

I didn’t go into the topic of safe withdrawal rates for retirement expecting the topic to be so deep and full of variables! Afterall, the concept seems simple enough right?

How much can I take out of my investment portfolio each year, if I need that nest egg to last for 30, 35, 40, or even 50 years?

Ok, so let’s maybe start with the rule of thumb that advisors have used when looking at retirement drawdown plans for a while now.

Back in 1994 a financial advisor named William Bengen looked at the last 80 or so years of markets and retirement, did a bunch of math, and arrived at a concept we now call “The 4% rule.”

The basic idea of the 4% retirement withdrawal plan is that someone could safely withdraw 4% of their investment/savings portfolio each year and – assuming a 60/40 or 50/50 split of bonds/stocks in their portfolio – they would never run out of money. This idea of withdrawing a certain percentage of your portfolio to fund your retirement is called the Safe Withdrawal Rate (SWR). The math behind this magic 4% figure means that if you have the nice round $1 Million investment portfolio that we all dream of, you could safely pull out $40,000 the first year, and then adjust for inflation and withdraw 4% plus inflation after that. (So if there was 2% inflation between year one and year two, you could now withdraw $40,800.)

Bengen, and another highly influential study took their rule and retroactively applied it to retirees from every single year from 1926 to 1994. They found that nearly 100% of the time (depending on what was in the investment portfolio) people could retire, and withdraw 4% of their portfolio for 30 years of retirement – and not run out of money. In fact, a large percentage of the time, if retirees followed the 4% rule, they not only didn’t run out of money, they finished life with more money than when they started retirement!

Keep in mind, these authors didn’t worry about OAS or CPP, or a workplace pension, or even the tax implications of different types of withdrawals. They were simply trying to come up with a useful rule of thumb for how much a person could safely withdraw from their retirement portfolio.

What the 4% Rule means for your Magic Retirement Portfolio Number

If you can safely withdraw 4% of your portfolio to fund your retirement, then the simple math tells us that if you can accumulate 25x your annual retirement budget, you no longer have to work.

Here’s the breakdown:

- Jane looks at her budget and realizes that once she retires she will have a lot less spending demands. She carefully weighs the numbers and believes she’ll need $40,000 per year to quit her 9-to-5.

- Consequently, Jane needs the magical “4% of her portfolio” to equal $40,000 per year.

- For a 4% withdrawal to equal $40,000, Jane will need a $1,000,000 portfolio.

- If Jane reassess and realizes she needs $60,000 per year in retirement, Jane would need 25 times $60,000 (because 4% goes into 100% twenty-five times) which is $1.5 Million.

- Jane might not need anywhere close to $1.5M if she intends to do a little part-time work in retirement, and is willing to use some math + research strategies to help herself out a bit when it comes to managing her nest egg! But more on that later…

4% Safe Withdrawal Rate: Potential Problems

Up until the 4% rule became a thing, when financial advisors were asked about safe withdrawal rates, the only thing they could really say is, “it depends.”

This was followed by a whole lot of graphs, math, and other boring stuff that no one really understood, but didn’t want to admit to not understanding.

The 4% rule of thumb was a BIG deal when it came to financial planning. It provided the best answer yet to the millions of retirees who desperately wanted an answer to the question:

“How much money can I take out of this portfolio each year without going broke and eating cat food as an 80-year-old?!!!

Before we get into discussing the nitty gritty of safe withdrawal rates today, we must understand the limitations of the 4% rule. Here are the major rules that I came across after reading for roughly a hundred hours. The research I read was mostly done by people who have dedicated a major part of their life’s work to studying retirement and spending patterns across the globe. As far as I can tell, they are our best hope for trying to define just what the range of outcomes will be for various types of retirement spending + investing plans. The two major experts that I relied on most were Wade D. Pfau and Michael Kitces, with major assists to the writers behind Early Retirement Now, The Mad Fientist, and Millennial Revolution.

1) There is no way to know the future returns for any asset class. We’ll get into this more later on in the show, but basically, the vast majority of the math that these folks are basing their withdrawal rates on is underpinned by a US stock market that has done incredibly well over the last 100+ years. A few other stock markets of developed countries have done as well (Yay Canada!), but the majority of stock markets DO NOT return 10%+ over the long haul.

It turns out that when you don’t know how much money your nest egg will be generating, solving for how much money to take out becomes kind of hard to answer!

2) These withdrawal plans were mostly created with a 30-year retirement time horizon in mind. When most people were retiring at 60 or 65, and living to 75-80, a 30-year window looked like a pretty safe horizon for most people. If this still describes your plan, a 30-year horizon is probably still a pretty safe rule of thumb. If you’re looking at leaving your job at 40-50 years of age (or even earlier) and living well into your 90s, you could easily be looking at a retirement that lasts 50+ years! (Which is pretty cool to think about, really!)

3) The 4% rule doesn’t reflect how many Canadians actually invest and pay for investment advice. In a perfect world, we would all handle our own withdrawal plan and DIY our portfolio allocations and withdrawals. But many of us aren’t interested in diving into the deep end of handling our own assets. Consequently, we have to take those pesky investment-related fees into account when looking at our safe withdrawal plans. If you’re paying 2% of your returns to a mutual fund salesperson each year, you will need a lot more than $1 Million to safely withdraw 4% each year.

4) The 4% rule doesn’t take into account adjustment in behaviour. For example, Jane might take on a little part-time work to make $10,000 per year if she sees her account balance going down too fast. Or she may decide to move somewhere that has much lower living costs. A blanket rule that tries to predict 30 years into the future can’t possibly allow for all of these variables.

5) There is no OAS and/or CPP taken into consideration when looking at the 4% rule. It’s also likely that Jane might not have considered how taxes might affect how much she needs to withdraw each year.

6) The 4% rule tries to address what us finance geeks call Sequence of Return Risk – but it gets really hard to do so after you go beyond the 30-year mark of retirement. More on this below.

So, now that we know what the rules of thumb are for safe withdrawal rates that the professors of all things money have come up with, as well as some of the limitations of those rules of thumb, let’s take a look at what this might mean when applied to your retirement!

How has the 4% Rule Done in the Past

Given all of these variables that the 4% rule doesn’t account for, you might be wondering just why it is so widely used.

The truth is that I put all that naysayer stuff first because folks love to poke holes in financial theories. (For good reason, we’re talking about people’s life plans here.) Let’s look at just why the 4% rule has become the rule of thumb.

As always when discussing financial planning and financial projects, one must understand that while looking at past results in the stock and bond markets is one of the best tools we have, it does not guarantee future results!

Drawing on what I’ve read from Bengen, the Trinity Study, and recent authors such as Pfau and Kitces, here’s some summary notes on just how the 4% rule would have worked in the past in the USA market. (The Canadian market has actually done slightly better most of the time, so the conclusions would be quite similar when looking at past Canadian returns.)

1) When you apply the original 4% withdrawal philosophy, not only does your money never run out over any 30-year period over the last 100 years – But 95% of the time the retiree would have finished with MORE THAN THEY STARTED WITH!

I know this sounds crazy, but companies have made a lot of money the last 100 years. If you owned a piece of them, you’ve done pretty well!

2) More than half of the time, the retiree who stuck to the 4% rule would have DOUBLED THEIR MONEY at the end of the 30-year time frame.

What this means, is that in the past, it is far more likely that retirees could have spent substantially more than that 4% withdrawal safety number, than it was that they would ever run out of money.

3) Rather than use Bengen’s 60/40 portfolio, you can actually increase your chances of favourable outcomes by skewing your portfolio to take on more stocks. Of course, your portfolio will also be likely to cause a bit more heartburn as you watch stocks gyrate up and down over the years.

4) Even folks who retired during the rough decade of the 2000s are doing just fine.

If I Want to Retire Early or do this whole “FIRE” Thing – Does the 4% Work for Me?

The short answer is: Probably Not

When you start to take rules that were created for a 30-year safe withdrawal period, and stretch them out over 50+ years, it makes sense that the rules of thumb don’t really work anymore.

Taking money out of your nest egg for that long means that you’re more likely to encounter a long-term period of rough markets, and have your money run out.

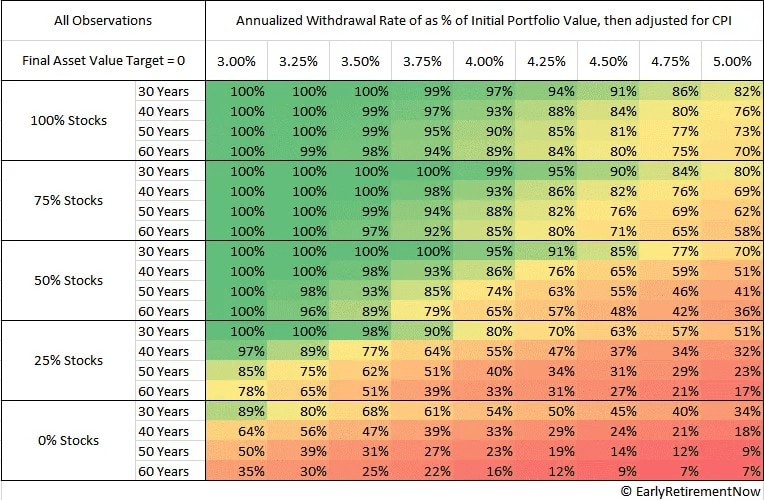

The website Early Retirement Now (created by folks who are fluent in high-level economics math and Monte Carlo simulations) have created the following chart and conclusions when it comes to safe withdrawal rates and long retirement periods.

I’ve checked their assumptions with a ton of really smart people that I trust, as well as doing the math myself, and if you assume the same returns that we’ve had the past 100 years or so in North America, I can’t find anything to argue with!

1) The 30-year 4% rule still works pretty well, and a 5% withdrawal rate is only fit for the very adventurous or flexible-minded out there!

2) Tilting your portfolio towards stocks over bonds increases your chances of the best outcomes – assuming that you don’t panic when markets go down and sell at the worst times.

3) At high stock allocations, the 4% rule still worked pretty darn well for a 50- or 60-year retirement! (With past returns that is.) Continue Reading…