McLister says new limits on government-backed mortgage funding will make it costlier for lenders to fund mortgages, or new underwriting rules will make it harder to qualify for mortgages.

2.) Record discounts for variable mortgage rates:

By the end of 2015, some lenders or brokers will be advertising discounts better than prime minus 1%.

3.) Brokers will break into there camps:

These will be full-service, online mortgage brokers and everyday brokers. The latter will be uncompetitive versus other brokers, banks and credit unions, McLister says.

4.) A glut of private money:

Alternative lenders like Mortgage Investment Corporations (MICs) will thrive as investors chase higher yields and the abundance of capital will tempt sub-prime lenders to take more risk. McLister expects that as a result some will offer mortgages with only 10% or 15% down instead of the traditional 20% or 25%. As a result, consumers will have more lending options at lower interest rates.

5.) Brokers will pitch you other stuff:

Expect cross selling of everything from GIS to insurance, credit cards and RRSPs.

I haven’t noticed many changes since Scotiabank bought out ING Direct in 2012, except for two:

They changed the name to Tangerine

Why did they do this? Is it a fruit? Is it a colour? WHY? People like my parents already think ING is a fake bank that will steal all my money: calling it something as light and fluffy as Tangerine does not help my case that it is a real bank with real interest rates, and that banks with tellers and real estate are as 20th century as AOL.

I will forgive them, however, because CEO Peter Aceto told Canadian Business that they weren’t allowed to use the name ING anymore. Here’s the rationale behind that decision:

“Simplicity”and “innovation”were two things the bank wanted to come across in its new name—the idea was to hearken back to its earlier days (being an alternative, simplified place to do your banking), but push the brand forward at the same time. The name Orange was considered on the shortlist, but was considered to be “too safe or obvious of a choice.”Tangerine makes reference to ING Direct’s orange history, (Ed Note [DK]:by orange history, do they mean just using the colour orange? How does a bank have colour history?) while also being significantly different.

Aceto says part of the branding discussion also took into account the more “fun”aspects of the name.

“We understood the risk that a name like that could be interpreted as being silly, or not serious,”he says. “Banking is important, it’s serious. We’re asking you to give us your life savings, or to help you buy a home or invest.”

That’s why there won’t be any references to fruit in any of Tangerine’s advertising materials or promotional campaigns. The fun name “does a lot of work for us”in sparking interest in Tangerine, Aceto says, but service at the customer level needs to be thoughtful and earnest in order to build a client base.

“I want people to think, oh, they’re different. They’re not like everyone else.”

They changed the debit card by making it flimsier and WRONG

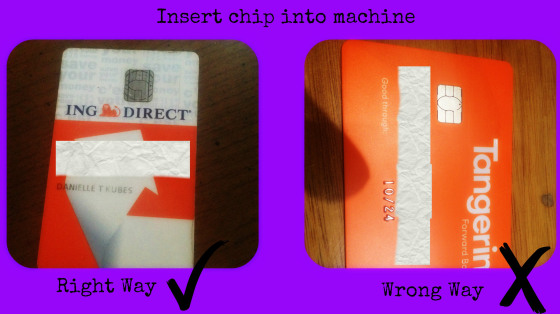

Writing the bank name horizontally across a debit card made sense when we signed for things.

Now we use a chip and PIN# method of payment. The chip is always entered vertically.

So why, on all debit cards, is the bank name still horizontal?

ING was the only card to write its name vertically, which was logical and made them seem the most current.

With the buyout, it has gone backwards and written its company name horizontally.

Also, while you can’t see this in a picture, the new card is very flimsy and bendy. It’s not really a problem but coupled with Tangerine it just kind of makes the bank seem flimsy.

Now, these are all personal pet peeves that have no affect on how they do business; banking with them hasn’t changed. They don’t have the best interest rates anymore; that award would go to credit unions in Western Canada, but they are still way better than the Big Five banks and they also have lower fees (no fees!) than the credit unions.

All in all, it’s still my favourite Canadian bank with which to do my daily banking, but it’s no longer my favourite choice with which to invest in GICs, which will be the subject of another post.

Here’s how this article originally appeared at Danielle’s Pretty Little Poor Girl blog. And you should click on the link because apart from Danielle’s awesome slogan, she includes an extra paragraph at the bottom of her original post that further teases the good folks at Tangerine: JC.

Interesting piece in the Wall Street Journal entitled Bond Funds Load Up on Cash. Of course, investors have been preparing — usually prematurely — for the “inevitable” risk in interest rates since soon after the financial crisis in 2008 and so far it’s yet to happen.

As the Journal reports, though, large bond funds in the United States are holding the most cash since that same financial crisis: 6.6% on average among the top ten American bond funds as of their last reporting date, according to Morningstar Inc. That cash position is more than double what it was last year (on average). The last time cash levels in bond funds were this high was 2007.

The expectation is that the Federal Reserve will finally start to act and raise rates sometime in 2015. And of course, now we’re in December of 2014, 2015 isn’t quite so far in the future as it may once have appeared. The Fed’s Quantitative Easing program ended in October (at least the latest incarnation of it).

The yield on the 10-year U.S. Treasury note was 2.169% as of Friday, the Journal reports, down from 3% when 2013 ended.

Savers almost everywhere have nearly been beaten into submission by seemingly perpetual Zero Interest Rate Policies (ZIRP) imposed by central banks around the world.

The simple connection is that when interest rates are low, there is no incentive to save money. The flip side is that low interest rates make borrowing cheap, so people raise their debt load. So, is it still worthwhile to save when interest rates are low?

There are many fundamental reasons for believing that stock markets may have embarked on a long-term bull market comparable to those in the 1950s and 1960s, or the 1980s and 1990s, and that this process is nearer its beginning that its end.

He presents four arguments for a “structural bull market.”

1.) The worst financial and economic crisis in recent memory has ended and most of the world economy is enjoying “decent, if unspectacular, growth.”

2.) While not perfect, economic and financial policies around the world are predictable and so “unlikely to cause further market disruptions.”

3.) Technology continues to advance and innovation should stimulate investment and consumer demand.

4.) Inflation is “almost nonexistent” in the advanced economies, so “interest rates are guaranteed to stay low for a very long time.”

From the Globe & Mail’s mortgage columnist Robert McLister comes this list of five predictions for mortgage shoppers in 2015:

From the Globe & Mail’s mortgage columnist Robert McLister comes this list of five predictions for mortgage shoppers in 2015: