By Winnie Jiang, Vice President, Portfolio Manager, BMO ETFs

(Sponsor Content)

Little about the current economic cycle has conformed to historical norms. With divergence in employment data and leading economic indicators, recent data released sent mixed signals that left investors perplexed about the near-term economic outlook.

On one hand, the job market remains overwhelmingly strong, with ISM (Institute for Supply Management) Services bouncing back from extreme lows in December and retail sales also rebounding. The re-opening of the Chinese economy will likely provide a breather on global supply chain issues while boosting demand. Consumer credit remains well retained as default rates stay low with no warning signs of near-term upticks.

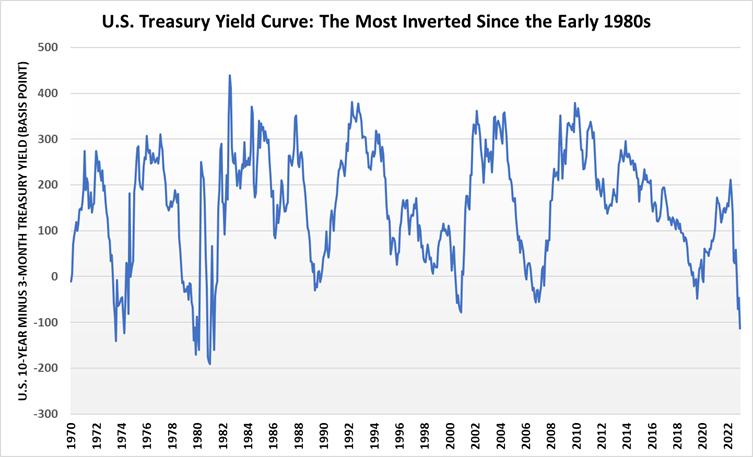

On the other hand, yield curve inversions, a precedent of most recessions, continue to worsen. 3-month U.S. Treasury yields are pushed above 10-year yields by the widest margin since the early 1980s. ISM Manufacturing PMI (purchasing managers’ index) and housing data also point to a gloomy outlook. Corporate sentiment and capital expenditure showed little signs of recovery, and housing permits have rolled back to pre-pandemic levels after surging strongly during Covid.

Source: Bloomberg, January 31st, 2023

The Outlook

While robust job markets and consumer data keep inflation well above the Fed’s long-term target, recent CPI (Consumer Price Index) announcements indicate things are steadily, albeit slowly, moving towards the right direction. The inversion of the yield curve caps the magnitude of further rate increases that could be absorbed by the economy before it slips into a recession.

According to satirist Karl Ludwig Borne, “Losing an illusion makes one wiser than finding a truth.”

I have become completely disavowed of the illusion that:

1.) People are able to predict the future with any degree of accuracy or consistency.

2.) Investors can improve their results by forecasting (or by following the forecasts of others).

Not even the almighty Federal Reserve, with its vast resources, near limitless access to data, and armies of economists and researchers has been particularly successful in its forecasting endeavors. For example:

Near the height of the dotcom bubble in 1999, Fed Chairman Greenspan argued that the internet was bringing a new paradigm of permanently higher productivity, thereby justifying lofty stock price valuations and encouraging investors to push prices up even further to unsustainable levels.

In 2006, Chairman Bernanke brushed off the most pronounced housing bubble in U.S. history, stating that “U.S. house prices merely reflect a strong U.S. economy.”

In late 2021, the Fed determined that the spike in inflation was “transitory.” It neglected to combat it, leaving itself in a position where it had no choice but to subsequently ratchet up rates at the fastest pace in 40 years and risk throwing the U.S. (and perhaps global) economy into recession.

The following commentary describes the underlying challenges relating to economic and market predictions. I will also provide some of the reasons why, despite strong evidence to the contrary, investors continue to incorporate them into their processes.

The Three Enemies of Forecasting: Complexity, Non-Stationarity and People

There is a near infinite number of factors that influence economies and markets. The sheer magnitude of these variables makes it near, if not completely impossible, to convert them into a useful forecast. Further complicating the matter is the fact that economies and markets are non-stationary. Not only do the things that influence markets change over time, but so do their relative importance. To produce accurate forecasts economists and strategists not only need to hit an incredibly small target, but also one that is constantly moving!

For most of the postwar era, economists and central banks relied heavily on the Phillips curve to inform their forecasts and policies. An unemployment rate of approximately 5.5% indicated that the U.S. economy was at “full employment.” Until the global financial crisis, any declines below this level had spurred inflation. Confoundingly, when unemployment fell below 5.5% in early 2015 and hit a low of 3.5% in late 2019, an increase in inflation failed to materialize.

This problem is well summarized by former GE executive Ian H. Wilson, who stated “No amount of sophistication is going to change the fact that all your knowledge is about the past and all your decisions are about the future.”

Saved by 50/50

When it comes to economies and markets, it’s hard enough to be right on any single prediction. A forecaster who gets it right 70% of the time would be a rare (and perhaps even a freakish) specimen.

However, investment theses are rarely predicated on a single prediction. When a forecaster predicts that inflation will (a) remain stubbornly high, (b) rates will rise further, and (c) that these two developments will cause stocks to fall, they are technically making three separate predictions. Even with a 70% chance of being right on each of these forecasts, their overall prediction about the market has only a 70% chance of a 70% chance of a 70% chance of being right, which is only 34.3%! Continue Reading…

Late in January, the Bank of Canada boosted rates by another 0.25% and signalled that they will now pause and evaluate. I’ve been calling that the rate hike hiatus. As I touched on in mid-January, inflation is moving in the right direction and the consumer is holding up quite well. It’s a Goldilocks scenario, for now. That said, the rate hikes have not worked their way through the economy. In fact, many suggest that we’ve felt almost no economic damage from the rate hikes. There is a lag affect; it can take a year or two for hikes to be felt in full. But let’s call the rate hike hiatus good news.

The big news last month was the announced rate hike hiatus in Canada. Of course, markets are forward “thinking” and they are pricing in a soft landing and rate cuts in 2023. That Yahoo!Finance post suggest that cuts are likely not on the table this year. That would only happen if something breaks and we get a serious-enough recession. Also, inflation would have to be completly under control. The Bank of Canada is not likely to cut rates if inflation is not close to that 2% target.

Rate guesses, not so good …

The consensus appears to be the call that there will be no rate cuts in 2023, though there is a sprinkling of calls for cuts in late 2023. And all said, we should remember the rate predictions from March. Not even close.

Inflation is so unpredicatable. And inflation might still be driving the bus in 2023.

Coming in for a landing

Lance Roberts looks at the history of soft landing and hard landings. There were 3 past soft landing scenarios, but none in an inflationary environment. The affect of rate hikes have largely not been felt, and likely have had little push on inflation. But that will come over time of course.

Here’s the chart that shows the positive effect of a weak U.S. Dollar for international equities. With bonds looking better and the potential for international markets, the traditional balanced portfolio might ‘be back’ one day soon.

Rising interest rates are causing a lot of unhappiness among bond investors, heavily-indebted homeowners, real estate agents, and others who make their livings from home sales. The exact nature of what is happening now was unpredictable, but the fact that interest rates would eventually rise was inevitable.

Long-Term Bonds

On the bond investing side, I was disappointed that so few prominent financial advisors saw the danger in long-term bonds back in 2020. If all you do is follow historical bond returns, then the recent crash in long-term bonds looks like a black swan, a nasty surprise. However, when 30-year Canadian government bond yields got down to 1.2%, it was obvious that they were a terrible investment if held to maturity. This made it inevitable that whoever was holding these hot potatoes when interest rates rose would get burned. Owning long-term bonds at that time was crazy.

One might ask whether we could say the same thing about holding stocks in 2020 when interest rates were so low. The answer is no. Bond returns are very different from stock returns in terms of unpredictability. We use bond prices to calculate bond yields; one is completely determined by the other. The situation is very different with stocks. Even when conditions don’t look good for stocks, they may still give better returns than the interest you’d get if you sold them to hold cash. All the evidence says that most investors are better off not trying to time the stock market.

Most of the time, investors are better off not trying to time the bond market either. However, the conditions in 2020 were extraordinary. Long-term bonds were guaranteed to give unacceptably low returns if held to maturity. This was a perfectly sensible time to shift long-term bonds to short-term bonds or cash savings.

Houses

The only way house prices could rise to the crazy heights they reached was with interest rates so low that mortgage payments remained barely affordable. Fortunately, the government imposed a stress test that forced buyers to qualify for a mortgage based on payments higher than their actual payments. This reduced the damage we’re starting to see now. Unfortunately, there is evidence that some homeowners faked their income (with industry help) so they could qualify for a mortgage. This offset some of the good the stress test did. Continue Reading…

’Tis the Season for economic forecasts. Further to the Vanguard 2023 outlook highlighted on the Hub yesterday comes various forecasts from Franklin Templeton Investments and its sub-advisors.

As with Monday’s blog, we’ve highlighted relevant paragraphs directly from the horse’s mouth, including the subheadings from the various money managers. Unless otherwise indicated, images are from our image banks.

ClearBridge Investments: U.S. economic outlook by Investment Strategist Jeff Schulze

Recession is the path of least resistance

As we look ahead to 2023, recession has gone from a distantly possible scenario to the most probable one, and the potential pivot by the Fed that many equity investors are hoping for is unlikely to occur.

Our views are grounded in the reading of the ClearBridge Recession Risk Dashboard of 12 economic indicators, which has been flashing red for the past four months, indicating a recession. Eight of the 12 underlying indicators are signaling recession, including traditional recession precursors, like the 10- year/3-month Treasury yield curve, which inverted this fall. This portion of the yield curve has correctly anticipated the last eight recessions dating back to 1970, providing an average of 11 months of warning.

Image: Pexels/Mart Production

A recession is not a done deal, however. The most likely positive path involves what we have dubbed the “immaculate slackening” where the labor market tightens but not too many jobs are lost. Job openings are still more than 3 million above their pre-pandemic level (but down 1.5 million from the peak), while the total number of persons employed is only around 1 million greater than before COVID-19. This suggests room exists to loosen labor demand but not destroy as many jobs, which would help restore balance and ease wage gains. Importantly, this could help ease inflation, particularly in service industries where wages are a larger component of prices.

The most important factor to achieve a soft landing is a substantial reduction in inflation, which would allow the Fed to back off its aggressive actions. With inflation unlikely to return to 2% in 2023, and the labor market proving resilient, the Fed is likely to continue to tighten monetary policy to slow the economy and curb price increases, which will ultimately result in a recession. Monitoring the health of the labor market will be important in the coming year, given its role as a key inflation barometer for the Fed. We will also be looking for signs of weakening consumption outside of the most interest rate sensitive areas as evidence that a slowdown is taking deeper root.

ClearBridge Investments: Global infrastructure outlook by Portfolio Managers Charles Hamieh, Shane Hurst and Nick Langley

Infrastructure earnings more secure than global equities; U.S. expected to focus on renewables

From no growth in 2020 to rapid growth in 2021 to slow growth in 2022, we look at 2023 with a base case of recessions in the U.S., Europe and the U.K.

The impact on infrastructure, though, should be muted, particularly for our regulated assets, where the companies generate their cash flows, earnings and dividends from their underlying asset bases, as we expect those asset bases to increase over the next several years. As a result, infrastructure earnings look better protected compared to global equities.

Infrastructure assets more secure than global equities. Image from Franklin ClearBridge

Most infrastructure companies have a link to inflation in their revenue or returns. Regulated assets, such as utilities, have their regulated allowed returns adjusted for changes in bond yields over time. As real yields rise, utilities look poised to perform well, and we have currently tilted our infrastructure portfolios to reflect this.

As a result, the underlying valuations of infrastructure assets are relatively unaffected by changes in inflation and bond yields. However, we have seen equity market volatility associated with higher bond yields impact the prices of listed infrastructure securities, making them more compelling when compared with unlisted infrastructure valuations in the private markets.

On top of its relative appeal versus equities, infrastructure should benefit from several macro drivers in 2023 — and beyond. First, energy security is driving policy right now, and a significant amount of infrastructure will need to be built to attain energy security. High gas prices and supply constraints brought on by the Russia/Ukraine war have highlighted the importance of energy security and energy investment. This is supportive of energy infrastructure, particularly in Europe, where additional capacity is needed to supplant Russian oil and gas supply, and in the U.S., where new basins are starting up, in part to meet fresh demand from Europe. Continue Reading…