“Your future depends on many things, but mostly on you.”

“Your future depends on many things, but mostly on you.”

—Frank Tyger (1929–2011), cartoonist, columnist and humourist

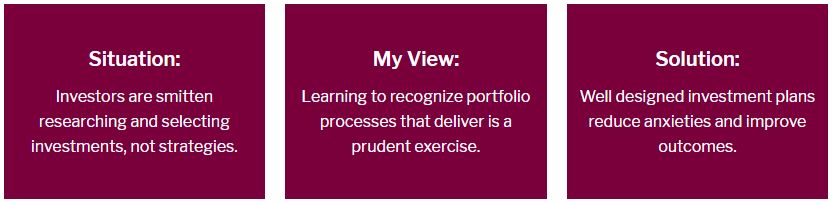

Designing the investment plan for the long haul requires much serious thought. Unfortunately, investors shortchange themselves on two fronts. Firstly, they spend far too much time selecting investments. Secondly, and more important, they spend too little time researching and establishing their investment policies and strategies. The ones that the plans should put into effect to reach personal goals.

In my experience, few investors actually have a sensible game plan that is being followed. Too often, this results in a collection of “flavour of the day” investment selections. Designing the appropriate investment plan is essential, particularly the asset mix targets.

“Understanding the major investment risk factors brings perspective to the plan. The ability, willingness and need to take risks are your top three.”

Happily, this situation is easy to rectify. A new year is about to make its grand entrance. Let us take a breather to contemplate a few improvements.

Stewarding the finances is truly a long journey. If you were my client, I would start with this question, “What is important about investing to your family in 2018 and beyond?”

My observation is that many investors opt for preservation of capital. Others focus on portfolio growth. The rest concentrate on the retirement income stream. Lifestyle needs are also high on the pecking order.

I touch on a handful of key steps in designing your game plan:

1.) Retirement prospects

Determine the family’s desired retirement income goal in today’s dollars. Calculate the size of portfolio to reach and sustain the goal. This provides portfolio direction and purpose. Estimate the personal rate of return required to achieve the retirement nest egg ballpark. Then treat that rate of return as the “investment benchmark” for the game plan.

Once the personal rate of return is identified, there is likely no need to incur higher investment risk than necessary. This is especially important to retired investors. Consider all the investment accounts owned as part of the big picture, not in isolation. Revisiting your “asset location” best practices helps fine tune the game plan.

2.) Investor profile

Analyze which type of investor profile suits and feels best. The most familiar ones are labeled as preservation, income, balanced, growth and aggressive. In my experience, investor profiles change infrequently.

The majority of investors are comfortable within 40% to 60% allocated to stocks and the remainder to cash and bond selections. For example, a balanced profile typically allocates about 50% to stocks, 40% to bonds and 10% to cash instruments.

3.) Asset mix

Asset mix decisions have the greatest impact on portfolio outcomes than any other factor. Studies show that these decisions explain a substantial amount of variations in total portfolio returns. Continue Reading…