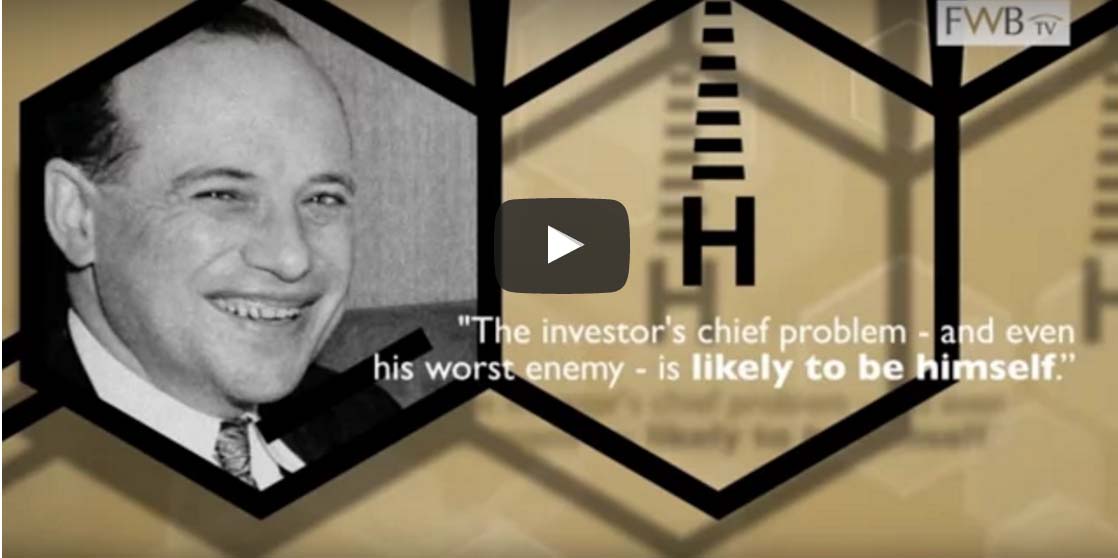

If you’re an investor, there’s a good chance the real enemy is the face you see every morning while shaving (or applying makeup!). The pithy quote in the screen shot is of course from legendary value investor Benjamin Graham.

The main point of this 4-minute video is that successful investing is about controlling what you can. You can’t control what the market does, but you can control what you do in response. In our experience, a person’s returns depend less on whether they pick great investments than on whether they can manage their emotions.

One of the experts in the video describes the physiology of stress that investors suffer during — well, times like the past few weeks! In the heat of volatility, particularly the downward variety, our emotions can get the better of us. There’s a reference to a Cambridge University study of 142 students, all male, who were invited to play a game about trading stocks. They found that the more testosterone they found in the subjects, the greater the risks they took on. Such surges of chemicals and emotion can actually affect your perception of the future, and seldom for the better!

Implications for actively managed funds

Since the Evidence-based Investor Videos largely sing the praises of passive or index investing, you might not be too surprised by a statement that this research may have some implications for investors who use actively managed funds. One source asserts that the investment industry is a stress competitive arena and many fund managers tend to be young males. The decisions they make under pressure and stress may cause them to be overconfident about the stock bets they place on your behalf.

The video concludes that investors may benefit by doing business with a rational, use unemotional advisor.

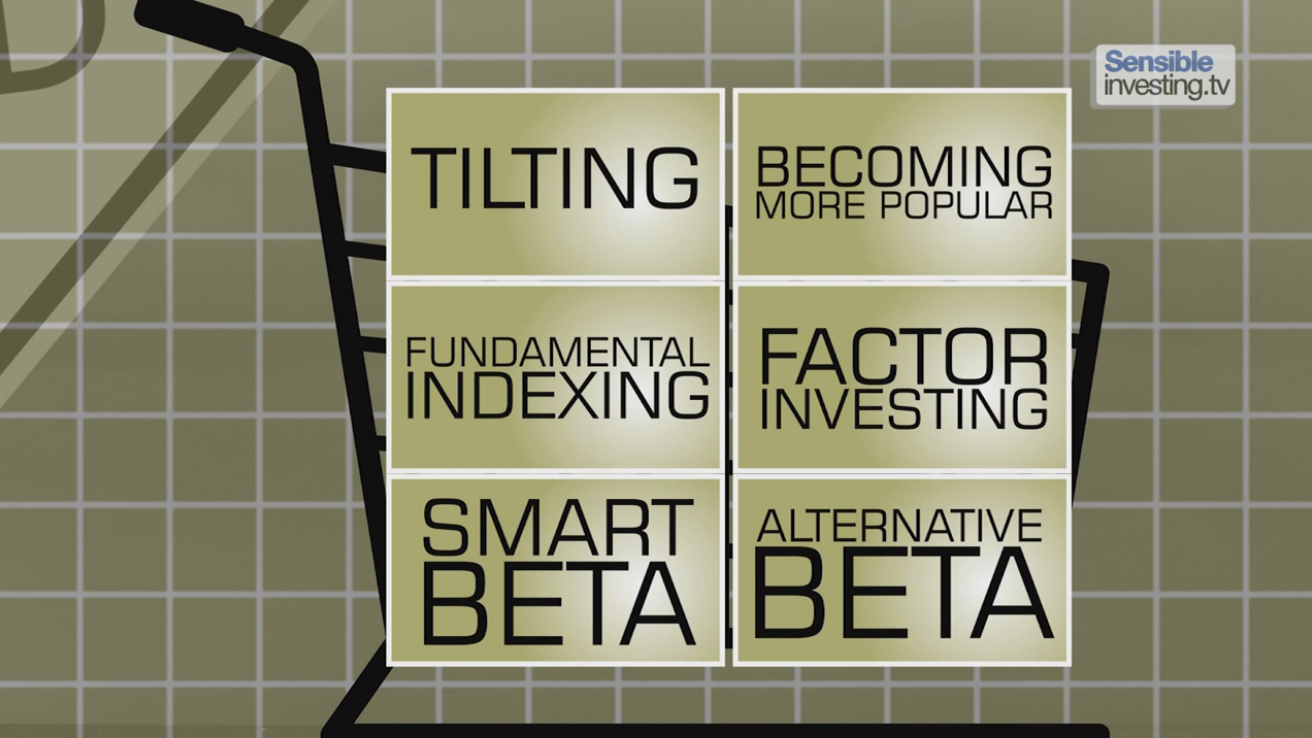

In addition, SensibleInvesting.TV has put up part 7 of the How to Win the Loser’s Game series of videos. While indexing is a relatively simple way to invest, there are still important questions index investor need to ask. Crucially, they need to ensure they are invested in a diverse range of assets that reflects their attitude to risk. They might also want to “tilt” their portfolios to particular risk factors — small-cap or value stocks, for example. While more volatile, these have been shown to deliver higher returns over the long term.

In a previous post on my series on Behaviorial Finance, I reviewed Richard Thaler’s concept of Loss Aversion behaviour. [the Hub version ran here last week.]

The concept states that people will feel more hurt emotionally with a loss than an equivalent gain gives pleasure.

Consequently, we will be more prone to take excessive risks to eliminate that loss.

Thaler also observed this phenomenon in reverse: specifically, in how people behave when they are making successful financial/investment decisions.

Thaler said this behavior gains critical mass in periods that would be described as financial bubbles, in which people are enjoying repetitive excessive gains in their investments. Using the stock market euphoria of the late ’90s as an example, Thaler comments:

“… in the 1990s individual investors were steadily increasing the proportion of their retirement fund contributions towards stocks than bonds, meaning that the portion of their new investments that was allocated to stocks was rising. Part of the reasoning seems to be that they had made so much money in recent years that even if the market fell, they would only lose those newer gains. Of course the fact that some of your money has been made recently should not diminish the sense of loss if that money goes up in smoke. The same thinking that pervaded the views of speculative investors in the boom housing market years later. People who had been flipping properties in Miami, Vegas had a psychological cushion of house money that lured them into thinking that at worst they would be back to where they started. Of course when the market turned down suddenly, those investors who were highly leveraged lost much more than house money. They lost their homes…”

Conventional thinking has been (and I’ve practiced this myself) that when you have gains in a stock you should take some money off the table and sell the equivalent amount you initially invested in and the then hold the profit amount.

Playing with the House’s money

At that point, you are essentially playing with the house’s or in this case the stock market’s money. If we were to lose all that “profit” or house money, we wouldn’t feel we really haven’t lost any money.

However according to Thaler’s observations about Loss Aversion, we will likely take more aggressive, and riskier decisions when the House Money is reduced, which perpetuates the bubble factor. We will either double down on the investment, continue to hold because we feel it is still a high quality investment compared to other investments (Endowment Effect) or engage in other high risk investment opportunities to regain that House Money. During bubble or bull markets periods, it will work for awhile, however at some point that excessive risk will bite back and ultimately that House Money will likely be gone along with part or all of the initial investment they originally put down.

I had a faced a situation that demonstrates this house money behaviour. I had owned a position in NeuLion. It was a very good investment decision, as it was up nearly 90 per cent so I had made a lot of money on paper. Unfortunately, the stock crashed but I was still up 25%. I decided to sell enough stock to cover my initial investment. The remaing stock I had was therefore House Money. At the time I decided to do this because in my mind I could rationalize and live with the fact that I didn’t really lose money even though the stock tanked royally.

The question that I faced was should I buy more stock at the lower price if the fundamentals of company were still strong or sell the remainder of my position if it fell below my loss threshold, which is 20 per cent. Under the Loss Aversion behaviour that Thaler described, I would buy more stock even if the company has experienced a negative game changer moment and is a riskier prospect.

With awareness of these types of behaviours, I decided to not buy additional stock and instead decided to ride the position out to see if the company could turn it around. If it couldn’t and the position fell another 20 per cent, I would sell the remainder of the position.

It’s interesting as normally one of my disciplines I have built up is to sell positions when they cross a minimum return threshold that I am seeking. Normally for me that is in the 20 per cent range but this time, I decided to hold onto the stock for longer, more so for practice as in the past I have realized that I tend to sell shares earlier and in many cases left money on the table. In this example I strayed away from my discipline and while I didn’t lose money, it could have easily gone the other way.

Managing your Greed

Greed ultimately drives this level of behaviour. The theme from this observation is that as much as it’s important to manage your losses, it is equally important to manage your gains, or more plainly, manage your greed. When you make investment decisions, you need to establish a minimum return you are seeking and when you reach that threshold you should re-evaluate the investment to determine if there is still upside or if it makes sense to bank the profit and move on to better opportunities.

Greed gets the better of us in most cases, but again developing a discipline and avoiding the false sense of security that the House Money Effect offers can allow you a greater chance to maximize the profits and benefits of your successful investment decisions.

Aman Raina, MBA is an Investment Coach and founder of Sage Investors, an independent practice specializing in investment coaching and portfolio analysis services. This blog was originally published on his web site and is reproduced here with permission.

Understanding the RRSP regime makes it easier to stickhandle your retirement marathon. This workhorse has been delivering on retirements since its introduction in 1957.

It really fits two groups of investors like a glove.

Those without employer pension plans and the self-employed.

Some investors still shun RRSP deposits but three solid reasons to pursue RRSP accumulations stand out for me:

• Long-term, tax deferred investment growth.

• Future withdrawals, ideally at lower tax rates.

• Contributions provide immediate tax savings.

Stay focused on how the RRSP dovetails into your total game plan.

The power of compounding really delivers.

Your RRSP mission is three-fold:

• Keep it simple.

• Treat it as a building block.

• The journey lasts a lifetime.

I summarize six vital “back to basics” RRSP areas for your review:

Despite all of the evidence that low-cost passive investing outperforms actively managed portfolios, many investors still cling to the belief that an active approach can help steer them through turbulent times in the market.

Even investors who have taken the plunge into index funds and ETFs can’t help themselves when faced with uncertainty. Emotions take over, as do our instincts to tinker with our investments to try and optimize performance.

Despite Dan’s best efforts to explain that these new and simplified portfolios should be used as part of a long-term investment strategy, the overwhelming number of comments from readers suggests that it’s nearly impossible for indexers to simply set-it and forget it.

Every year our team devotes a couple of our regular Wednesday morning meetings for reflection on the year that has passed. This is a chance for our team to review the insights, errors and observations that were made in the preceding twelve months and learn from each other.

We thought we’d share three of these lessons with our readers:

1.) Beware the assumption of mean reversion

One of the greatest surprises to investors this year was the continued slide in the price of oil. Like other structural/thematic trends, the decline in the price of oil due to international oversupply and weakening global demand has gone on far longer than some initially anticipated. Many assumed that prices would dip and then return to a more normalized range between $60 and $80. This is a good example of assuming mean reversion, i.e., that prices will naturally revert back to their mean. Continue Reading…

In addition, SensibleInvesting.TV has put up part 7 of the How to Win the Loser’s Game series of videos. While indexing is a relatively simple way to invest, there are still important questions index investor need to ask. Crucially, they need to ensure they are invested in a diverse range of assets that reflects their attitude to risk. They might also want to “tilt” their portfolios to particular risk factors — small-cap or value stocks, for example. While more volatile, these have been shown to deliver higher returns over the long term.

In addition, SensibleInvesting.TV has put up part 7 of the How to Win the Loser’s Game series of videos. While indexing is a relatively simple way to invest, there are still important questions index investor need to ask. Crucially, they need to ensure they are invested in a diverse range of assets that reflects their attitude to risk. They might also want to “tilt” their portfolios to particular risk factors — small-cap or value stocks, for example. While more volatile, these have been shown to deliver higher returns over the long term.