To Hedge FX Risk, or Not to Hedge: Currency markets are notoriously difficult to call but can meaningfully impact portfolio returns. ETF Strategist Bipan Rai provides a detailed framework for investing outside the Canadian market.

By Bipan Rai, BMO Global Asset Management

(Sponsor Blog)

Admittedly, using a spin on a famous Shakespeare quote to start a note on currency hedging1 is verging on trite. Nevertheless, if Hamlet were running a portfolio of overseas assets, his primary concern would have to be the “slings and arrows” of currency markets — which are notoriously difficult to call but can meaningfully impact portfolio returns.

For Canadian investors, looking abroad provides several benefits. The most important is diversification, whether it’s through access to other regions that are less correlated with Canadian markets or to other products that aren’t available domestically.

However, investing abroad also means taking on foreign exchange risk given that international assets are priced in currencies other than the Canadian dollar (CAD).

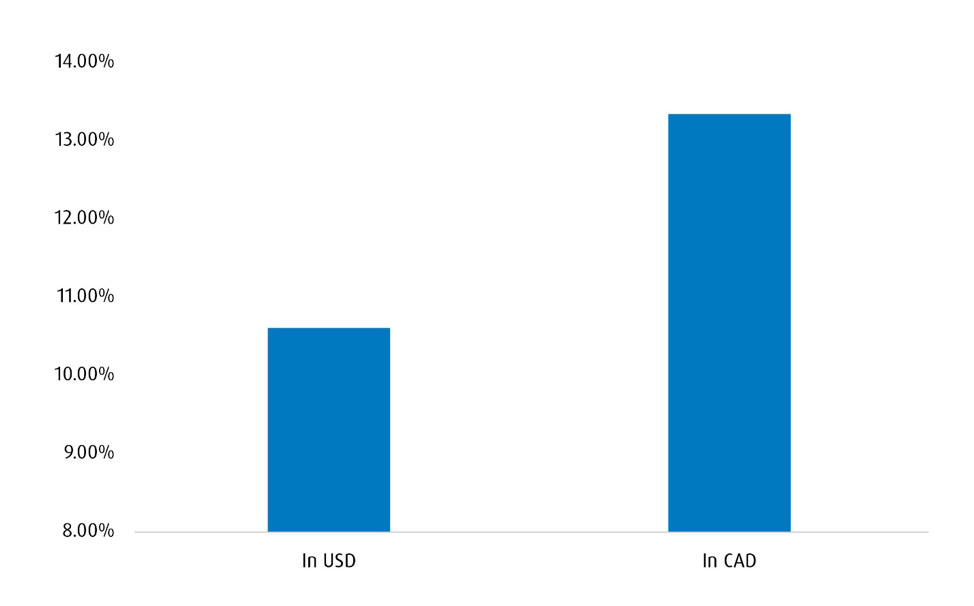

For illustrative purposes, consider Chart 1, which shows the total return for the S&P 500 in U.S. dollars (USD) and in CAD terms for Q1 of this year. In USD terms, the index was up 10.6% over that time frame, but since that period also corresponded to weakness in the CAD relative to the USD (or USD/CAD moved higher) the index outperformed in CAD terms (up 13.3%). That means that Canadian investors would have fared much better leaving their USD exposure unhedged ex ante.

Chart 1 – S&P 500 Total Return for Q1 2024

Source: BMO Global Asset Management

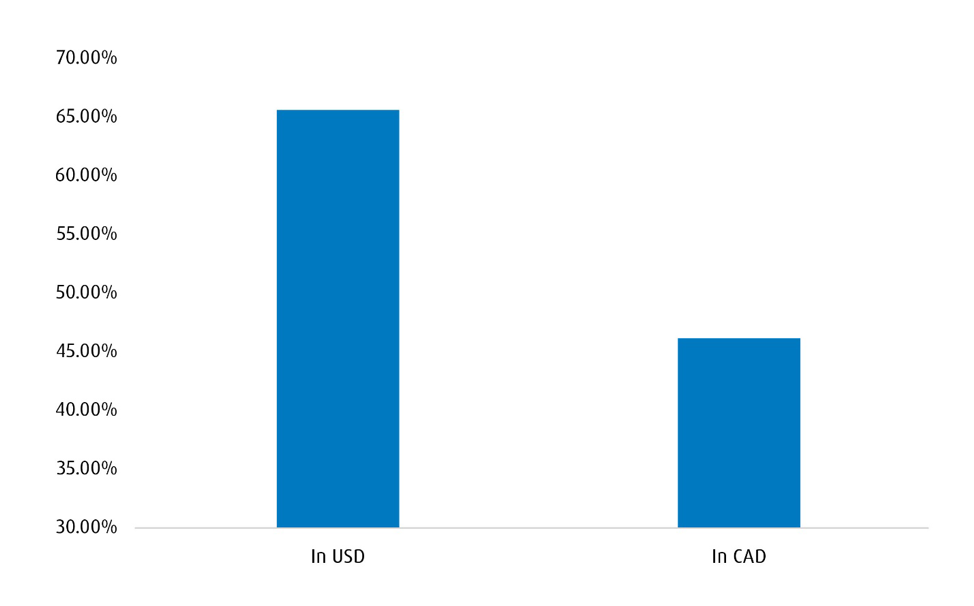

Now let’s look at an alternative period in which the CAD strengthened against the USD. Chart 2 shows a comparison of the total return for the S&P 500 from April 2020 to April 2021 (in which USD/CAD was lower by over 11%). During that period, the total return index outperformed in USD terms by close to 20%. In this scenario, an investor who had hedged their FX risk would have been in the optimal position.

Chart 2 – S&P 500 Total Return Between April 2020 – April 2021

Source: BMO Global Asset Management

As these examples show, currency risk is a key consideration for any investor who wants to look beyond Canada for diversification. That risk can cut both ways, which amplifies the importance of hedging decisions. In our minds, the decision to hedge foreign exchange (FX )risk (including the degree to which foreign exposure is hedged) comes down to the following:

- An investor’s view of the underlying currency pair

- Whether the currency pair is positively or negatively correlated2 with the underlying asset

In this note, we’ll make a brief comment on the first point but focus largely on the second one. as we feel that should be given more weight for hedging decisions.

FX Markets are Tough to Call

Taking a view on the underlying currency pair is easy to do — but difficult to capitalize on.

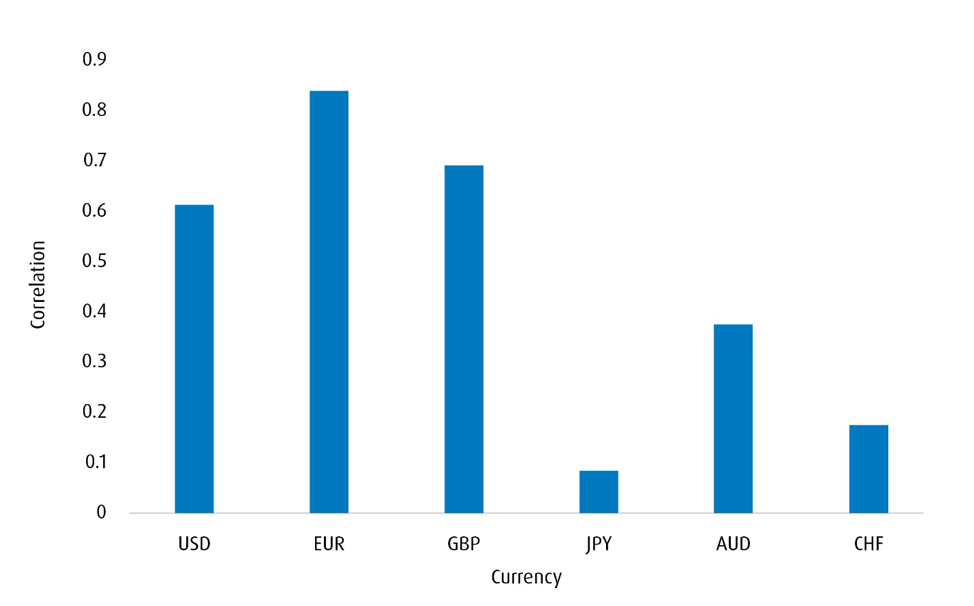

Indeed, foreign exchange markets are notoriously fickle. One reason why is the relationship between predictive factors and currency pairs is rarely stationary. For instance, a lot of market participants tend to use front-end (2-year) yield spreads as a proxy for central bank divergence in the spot FX market. Chart 3 shows the current correlation between those spreads and the different CAD crosses, and as expected, the relationship isn’t consistent from a cross-sectional perspective.

Chart 3 – Correlation Between Two-Year Spreads and the CAD Crosses

* * Correlation window is 2 years. The CAD is used as a base currency for this analysis. The spread is tabulated by subtracting the foreign 2-year yield from the CAD 2-year yield. Source: Bloomberg, BMO Global Asset Management.

We can also see this by looking closer at the relationship between a factor and a currency pair over time. Chart 4 shows the rolling 100-day correlation between USD/CAD and the price of oil (proxied by the prompt WTI contract3) going back ten years. Note how frequently the strength of the correlation (as well as the sign) changes over time. Continue Reading…