Once you stop working you may want to simplify your investment strategy. Your objective shifts from growing your investment portfolio to generating income. Flat and unpredictable markets, combined with historically low interest rates, can make this a challenging time in terms of creating retirement income.

One idea for creating a reasonably consistent level of monthly income is with a Monthly Income Fund. These funds have been around for quite some time. They hold a variety of government, municipal and corporate bonds, preferred shares and dividend stocks, and the payments come from a combination of interest and dividends, and sometimes, return of capital.

With these investments, cash flow is based on the number of units you own, not on the market value of the assets.

In non-registered accounts, the distributions can be more tax efficient than interest earned on GICs and bonds. However, keep in mind that there can also be taxable distributions in December (just as in other mutual funds) in addition to the monthly payout amounts.

Comparison of monthly income funds

Monthly income funds are sold by Canadian banks and mutual fund companies, and are also available in ETF versions.

The following chart is a comparison of some funds sold by Canadian banks as well as two popular ETFs. Continue Reading…

Once they move from the wealth accumulation phase to “decumulation” retirees and near-retirees start to focus on how to boost Retirement Income.

The latest instalment of myMoneySense Retired Money column looks at five “enhancements” to do this, all contained in Fred Vettese’s about-to-be-published book, Retirement Income for Life, subtitled Getting More Without Saving More. You can find the full column by clicking on this highlighted headline: A Guide to Having Retirement Income for Life.

You’ll be seeing various reviews of this book as it becomes available online late in February and likely in bookstores by early March. I predict it will be a bestseller since it taps the huge market of baby boomers turning 65 (1,100 every day!): including author Fred Vettese and even Yours Truly in a few months time.

That’s because a lot of people need help in generating a pension-like income from savings, typically RRSPs, group RRSPs and Defined Contribution plans, TFSAs, non-registered investments and the like. In other words, anybody who doesn’t enjoy a guaranteed-for-life Defined Benefit pension plan, of the type that are still common in the public sector but becoming rare in the private sector.

The core of the book are the five “enhancements” Vettese has identified that help to ensure that those seeking to pensionize their nest eggs (to paraphrase the title of Moshe Milevsky’s book that covers some of this ground) don’t outlive their money. Vettese says many of these concepts are current in the academic literature but have been slow to migrate to the mainstream, in part because few of these “enhancements” will be welcomed by the typical commission-compensated financial advisor. That in itself will make this book controversial.

Each of these “enhancements” get a whole chapter but in a nutshell they are:

1.) Enhancement 1: Reducing Fees

By moving from high-fee mutual funds or similar vehicles to low-cost ETFs (exchange-traded funds), Vettese explains how investment fees can be cut from 1.5 to 3% to as little as 0.5% a year, all of which goes directly to boosting retirement income flows. One of his takeaways is that “Tangible evidence of added value from active management is hard to find.”

2.) Enhancement 2: Deferring CPP Pension

We’ve covered the topic of deferring CPP to age 70 frequently in various articles, some of which can be found here on the Hub’s search engine. Even so, very few Canadians opt to wait till age 70 to collect the Canada Pension Plan. Because CPP is a valuable inflation-indexed guaranteed for life instrument — in effect, an annuity that you can never outlive — Vettese argues for deferral, although he (like me) is fine with taking Old Age Security as soon as it’s available at age 65. He argues that for someone who contributed to CPP until age 65, they can boost their CPP income by almost 50% by waiting till 70 to collect. “You are essentially transferring some of your investment risk and longevity risk back to the government, and you are doing so at zero cost.” Continue Reading…

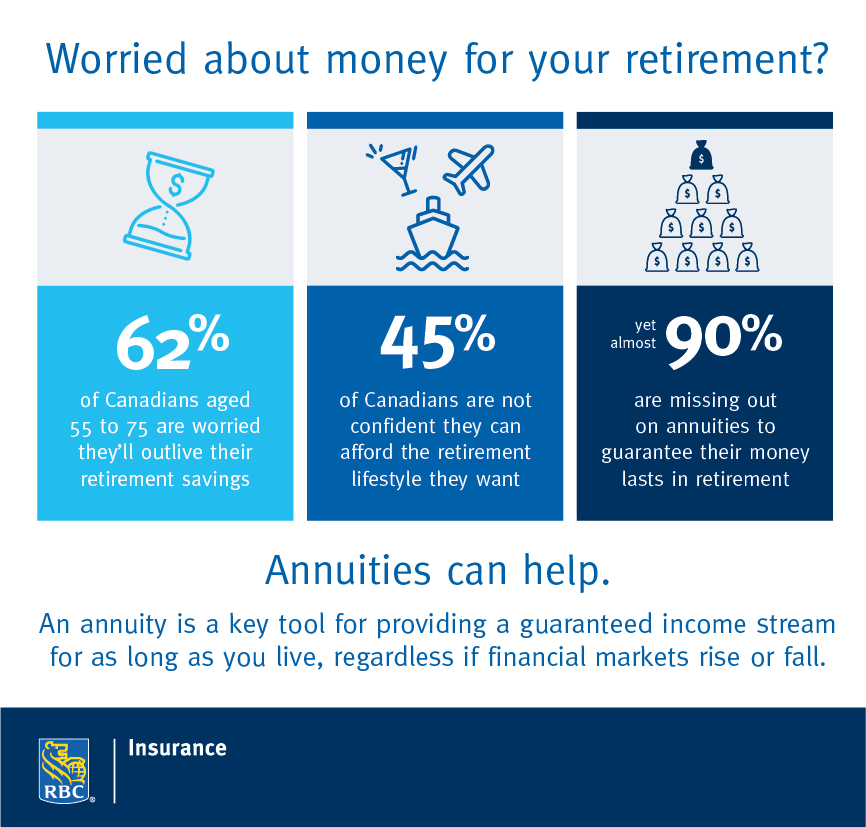

By Jean Salvadore, Director, Wealth Insurance, RBC Insurance

(Sponsored Content)

Summary: While Canadians want to live a full lifestyle in their retirement, a majority (62 per cent) are worried about outliving their retirement savings. The majority are missing annuities in their portfolio that can help guarantee an income stream in their retirement.

If you’re like most Canadians, your vision for retirement includes a full roster of activities such as travel, dining out and shopping for the things you want. But while many of us look to our retirement years as a time to enjoy life to the fullest, having enough money to support that lifestyle is a real concern. Canadians are living longer than ever before and, according to a recent survey by Ipsos for RBC Insurance, the majority (62 per cent) are worried that they’ll outlive their retirement savings.

In fact, even with various financial tools in place such as RRSPs and TFSAs, almost half of Canadians are still not confident that they will be able to afford the lifestyle they want. And perhaps not surprisingly, what’s most important to that lifestyle is keeping a sense of independence. Among those between the ages of 55 to 75, eight out of ten want to live at home for as long as they can and 72 per cent say it’s important to own a car. On top of that, almost three-quarters (68 per cent) would like to be able to travel at least once a year, shop for the things they want (62 per cent), and go out for lunch or dinner a few times a week (53 per cent). Continue Reading…

To decide if an investment belongs in your portfolio for retirement, you need to take a close look at its attributes or features. But, just as important, you need a close look at how well the investment suits your needs. A superficial look can steer you in the wrong direction.

From time to time, for instance, investors say “Now that I’m retired, I can’t invest in stocks any more. I can’t risk a 30% to 40% drop in the value of my portfolio.” But these same investors may buy annuities without considering the fact that annuity rates are related to bond yields. Both are at historically low levels. A revival of inflation could do extraordinary damage to the purchasing power you get from the fixed returns on bonds or annuities.

Retirement planning and four key factors to consider when investing for retirement

Retirement planning is the process of setting retirement goals, estimating the income needed to meet those goals and assessing your potential sources of retirement income. These days, more investors suffer from what you might call “pre-retirement financial stress syndrome.” That’s the malady that strikes when it dawns on you that you don’t have enough money saved to be able to earn the retirement income stream you were banking on. The best way to overcome this is with sound investing.

Additionally, here are four key factors to consider for retirement saving:

How much you expect to save prior to retirement;

The return you expect on your savings;

How much of that return you’ll have left after taxes;

How much retirement income you’ll need once you’ve left the workforce.

Should you consider investment products in your portfolio for retirement?

The financial industry has created income-producing investment products to cater to investors who are wary of stock-market uncertainty. These products can provide steady income that’s higher than bond interest, or dividend yields from stocks. However, these products are almost always subject to hidden fees and risks that continually drain your capital, or leave it vulnerable to unexpected losses.

Successful investors understand that occasional market plunges are normal and unavoidable. A drop of 30% to 40% in stock prices is rare. But after the plunge ends, stocks bounce back and eventually recover. Meanwhile, if you follow our Successful Investor approach, you’ll still have dividend income. What’s more, you don’t need to (and probably won’t) sell at the low in prices.

You can maintain reserves for your cash flow needs by selling some stocks every year, during times of high and low prices.

“The more bells and whistles, the lower the monthly income,” from annuities, says Caring for Clients’ Rona Birenbaum,

My latest MoneySense Retired Money column looks at the case for laddering annuities in order to avoid the problem of committing funds to annuities at interest rates that are only now coming off their historic lows. You can retrieve the whole article by clicking on the highlighted text: A low-risky annuity strategy to beef up your retirement cash flow.

Many investors are already acquainted with the concept of “laddering” guaranteed investment certificates (GICs), or bonds with different maturities. Maturity dates are staggered over (typically) one to five years, so each year some money comes due and can be reinvested at prevailing interest rates. This minimizes the likelihood of investing the whole amount at what may turn out to be rock-bottom interest rates, only to watch helplessly as rates steadily rise over time.

The same applies when it comes time for retirees or near-retirees to annuitize. At the end

of the year you turn 71 you must decide whether to convert your RRSP into a RRIF,

cash out and pay tax (few do this), or thirdly to annuitize.

Fortunately, annuitization isn’t an all-or-nothing decision. You can convert some of your RRSP to a RRIF and some to a registered annuity. You can take a leaf from the GIC laddering

concept and buy annuities gradually over five, ten or even more years. As regular Hub contributor Patrick McKeough observes in the piece, laddering annuities can reduce the potential downside: “You could buy one annuity a year for the next five years. That way, your returns will increase if interest rates rise, as is likely.”

Tally up how many annuities you may already have

Mind you, few observers believe in converting ALL your disposable funds into annuities. After all, as another Hub contributor — Adrian Mastracci — notes, you need to take inventory of the annuity-like vehicles you already may have, or expect to have: such as employer-sponsored Defined Benefits, CPP or OAS. Some investors may have a high component of annuity-like income without realizing it, and many families may already have five or six such sources of annuity-like income.

Certainly you need to consider both the benefits and drawbacks of annuities. The main benefit is they are a form of longevity insurance: making sure you never outlive your money no matter how long you live. There’s a case for having enough annuities that your basic “survival expenses” (shelter, food, heat, transport etc.) are taken care of no matter what. Finance professor Moshe Milevsky is also quoted in the article to the effect there are compelling financial and psychological reason to at least partly convert to annuities. And Milevsky is famous for making a distinction between “REAL” pensions (like DB pensions) that behave like annuities, as opposed to vehicles like RRSPs and TFSAs, which provide capital that only have the potential to be annuitized. Hence the title of Milevksy’s excellent book, Pensionize Your Nest Egg.

But annuities are not perfect. Apart from the common reluctance to commit to buying annuities at today’s still-low interest rates, there’s also the matter of the irreversible nature of the decision to convert some capital to an annuity. You’re handing over a large chunk of change to an insurance company and should you die earlier than expected, they in effect “win,” to the partial detriment of your estate. If on the other hand you live to 120, then YOU “win.”

Once you stop working you may want to simplify your investment strategy. Your objective shifts from growing your investment portfolio to generating income. Flat and unpredictable markets, combined with historically low interest rates, can make this a challenging time in terms of creating retirement income.

Once you stop working you may want to simplify your investment strategy. Your objective shifts from growing your investment portfolio to generating income. Flat and unpredictable markets, combined with historically low interest rates, can make this a challenging time in terms of creating retirement income.