There is a common misconception that starting a business is an expensive proposition. You need equipment, a website, an office, and staff to get the venture off the ground. Sure, in some instances, you will need all that and more: but there are ways to minimize your expenditure and secure funding to help you get going.

Why start a business?

Whether you have been ‘packaged out’ or are looking to transition into a new career, there has never been a better time to start a business. Working for yourself gives you unprecedented freedom. You can work flexible hours, from home if you choose, and any profit you make is yours. For anyone tired of working for someone else, while they reap the benefits, there’s a lot to like about being your own boss.

Financial support for entrepreneurs

There is a ton of support available for entrepreneurs. Fundera recently compiled a list of 105 different ways to secure money for your small business. You might not be eligible for all of them, but it’s worth taking a look.

Look for free loans first. These don’t need to be repaid, so it’s a win-win for you. If your startup is in a tech, science, or health niche, there are Federal small business grants available. These include the Small Business Technology Transfer Program and the Small Business Innovation Research Program. Check grants on offer in your state too, as there is less competition for state funding.

To check the full list of available grants and funding packages, click here.

Tools and equipment

Many businesses need tools and equipment to get started. For example, if you want to set up a handyman business, you’ll need a truck, basic tools, and possibly gardening equipment. Some of these you’ll likely already have, but you may need to purchase other items. Continue Reading…

There are myriad reasons why a malevolent actor would want to breach your small business’ data and info and/or attempt to defraud your company. Money (holding business info or operations ransom) is a big one, but your business also holds plenty of useful, sensitive data on customers, clients, business partners, trade secrets, and finances. Whatever the reason, data breaches are becoming the norm — not the exception — for small businesses around the world, and the cost can be substantial. Here’s what to do if you’ve been hit.

Plug the leak and and figure out what happened

If you are a network security pro or have your own in-house team that can perform this task, that’s great. However, the majority of small business owners feel lost and adrift following a security breach. The smart first step is to hire digital forensic specialists. These experts can do most of the technical work for you, from plugging up the initial breach point, tracking down the responsible parties (which is key for any sort of legal action), and finally doing the necessary legwork to shore up your defenses (so it won’t happen again).

This is also the time to contact your service providers. It’s highly unlikely that your breach exists in a vacuum. We’re talking your point-of-sale software company, internet provider, credit card processor, and accounting firm, so it’s wise to take the appropriate actions.

Boost security and consider Legal Representation

Your next step is to do what you can on your end to improve your data security. Employ the obvious, FTC-recommended actions like changing company passwords, security codes, and physical locks (yes, data breaches can occur when unauthorized people have actual, physical access to your workspace). Then, as the FTC suggests, “you may consider hiring outside legal counsel with privacy and data security expertise. They can advise you on federal and state laws that may be implicated by a breach.” Legal representation is vital for two major avenues — either taking action against those responsible or defending your business from liability (compromised personal data can put you in a serious legal pickle).

Make changes to prevent future breaches

A few solid ways to protect your small business from future security issues include separating personal and business accounts, beefing up your security and data permissions, and retraining employees about proper security protocols. The sad fact is that many security breaches are due to employees — whether malicious or unintentional. That’s why it’s absolutely critical that you take the time to carefully screen your hires to make sure they are reliable and trustworthy. This means holding quality job interviews where you ask the right questions to get an accurate sense of the candidates you’re vetting.

Notify those affected

Legal considerations aside (notification of a data breach may be forced based on state laws), being honest and upfront with your customers, clients, and business partners is always a good idea. It builds trust, for one. It also allows them to shore up things on their end, as security breaches are rarely just limited to the primary target.

Small businesses are generally easy targets for malicious actors for a variety of reasons. For one, they simply do not believe they are big enough to be hacked or breached. They also don’t have the time, money, or resources to devote to major cybersecurity. Knowing that you are vulnerable is half the battle, and the other half is staying calm but decisive when something does happen. Take these steps so you can recover and move on from a security breach.

Gloria Martinez loves sharing her business expertise and hopes to inspire other women to start their own businesses. Her brainchild is Womenled.org. Gloria’s vision is to help all women advance in the workplace and celebrate their achievements.

Changes are coming. Small business owners and professionals can feel it like a frosty winter breeze that lets you know winter is here. It’s time to get your winter tires on and prepare for longer hours commuting and shorter daylight hours. It’s time to understand and strategize for some cold Liberal government small business tax changes that may have a significant impact on your retirement plan through the changes to the income splitting and passive investment tax rules that will take effect in 2019.

You’ve worked extremely hard growing your business, for you, your family, and your employees. You’ve taken risks and sunk a lot of money and sweat equity into your company, and in your opinion, there should be a nice reward for taking this entrepreneurial path. And you may be right; but with rising costs, interest rates and tax rule changes, it’s getting harder to remember why you got in the business in the first place.

Maybe you don’t know how the tax changes will affect you and your family. Strategies for your business that have been implemented and worked in the past, may no longer work for you. To help you avoid being left out in the cold, let’s take a quick look at one relatively underutilized strategy that still exists for small business owners and professionals: it’s called an Individual Pension Plan (IPP).

It’s all about a level playing field

You are an incorporated small business owner, top executive, doctor, lawyer, veterinarian, or dentist, over the age of 40, consistently making over $200,000 gross/year and have been paying yourself T4 salary for a few years now. You likely know about the recent passive investment tax rule changes that make it even less enticing to save money within your corporation for retirement and you wish there was somewhere else you could save. You may be taking a T4 salaried income from your corporation instead of dividends to reduce your corporation’s gross taxable income. In turn you will lean on making RRSP contributions to reduce your annual personal tax bill.

The strategy discussed below can put you on the same playing field as a person with a Defined Benefit pension. If you were an employee of a company or government agency and qualified for a Defined Benefit pension program, you would be in a relatively rare and advantageous position. The IPP has different rules, but it is playing the same game.

A supersized RRSP

The IPP is often referred to as a “Supersized RRSP,” as in the IPP allows for you to contribute more annually than an RRSP. The extra contributions will allow you to save for their retirement like a Defined Benefit pension set up for one person. Establishing an IPP can provide you with greatly enhanced retirement benefits when compared to your regular RRSP contributions. The company is responsible for making the contributions and is a deductible expense.

What’s in it for you and your business

It is all about how much you can save, tax deferred, for your retirement and how much tax you can save in deductions for your company today. Continue Reading…

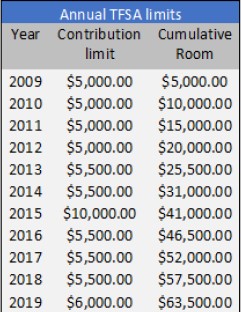

2019 TFSA limits will likely see an increase to $6,000 for 2019, up $500 from $5,500 in 2018. But is taking advantage of the TFSA the right choice for you?

The big story

Most Canadians still don’t understand the TFSA or know if it’s the right type of account for them. More room is great but according to the CRA in 2015, only 10% of Canadians are currently maximizing their TFSA limits1. Also, the CRA has looked to collect over $75 million in past audit penalties over improper use of the TFSA2.

The history

Starting in January 2019, annual TFSA room of $6,000 will be provided to each Canadian resident over the age of 18. Since 2009, Canadian residents have been able to contribute a small portion of their after-tax savings into this tax-free account. If you still are paying taxes on interest, dividends or capital gains on your investments in a non-registered account, it’s time to review the TFSA. If no contributions had been previously made, your TFSA room accumulates over time and a full $63,500 contribution could be made January 1, 2019.

The contribution you make today can grow without any tax implications in the future. If you over contribute, the CRA will penalize you 1% per month on any amount over the approved threshold. A best practice is to check first with the CRA to determine your personal TFSA limit for the calendar year.

Improper use

If you accidently, or purposefully, over-contribute to your TFSA, the CRA will impose a 1% per month penalty on the overage. This may be overstating the obvious, but over-contributing is a bad idea. You would have to reasonably expect your investments to grow higher than 12%/year (assuming simple math with a January 1stcontribution) to break even. Having TFSAs at two or more institutions may be a way you lose track of your contribution room. Ensure you check with the CRA to understand your annual TFSA contribution limit.

Another example of improper use could be frequently trading stocks within the TFSA, aka ‘day trading.’This may be considered a ‘business activity,’ as perceived by the CRA and you could be taxed personally on all the income, dividends and capital gains.

Spousal successor

An important but often overlooked benefit to utilizing a TFSA is as an estate planning feature: the spousal successor declaration. Continue Reading…

If you have a new business, then it is crucial that you organize it in the right way. Otherwise, you could end up missing out on more productivity.

So ensure that you get the most done possible during the day and increase profits while reducing problems with workflow. Set up your business for massive success by organizing your business better in the following three ways:

SOP (Standard Operating Procedure)

The first thing you need to do when organizing your new business is determine what kind of roles everyone has. There should be specific and unique classifications as to who is responsible for what.

The best way to do this is with SOPs. These are documents that show everyone what is expected of each role. You can have certain protocols as to how to handle consumer service, sales, and more.

The idea of the SOP is that anyone can plug right into your business and know how to perform that role without much hassle. It’s a step by step list of instructions so there is no confusion regarding what needs to be accomplished to deem that particular part of the business a success. Of course, this kind of thing won’t happen overnight!

It is best to sit down and make time to create your own SOPs. You might even read a few books or resources on the subject. This way, you have some guidance. There are a lot of different ways to do it, but you need to choose one that works for you.

For instance, some people find that they prefer to record a video and upload the files online. Then, it acts as a training resource. Others like to write down the procedures and share them in the cloud. Do whatever seems right for your new business.

The right software

We live in a world where software is more important than ever. It is vital that you use the right software tools or you could risk falling behind. Oftentimes, the right software will allow you to get more done, save time, save money, and stay on the cutting edge so you can generate new ideas for even more innovation. Consider the various types of software out there.

For instance, accounting software for nonprofits helps youkeep an eye on your transactions. This is crucial for a company. If you lose sight of what you need to be doing for your income or expenses, then it could come back to bite you later. This is true regardless of what kind of business you run.

Another type of software is a great CRM. Being able to communicate with your team and upload information about customers is invaluable. It shaves time off the communication cycle and gives everyone what they need in the cloud.

Sales and Marketing Automation

Long gone are the days where marketers had to sit down and write out a new email, post, or ad by hand. Today, you can use automation software to make these assets in a scalable way. After all, your team can’t be there every second of the day.

You want your team focused on the higher-level aspects, so let them do that. Enable them with marketing software that automates your funnels. It can test your ads right away. Continue Reading…