By Dale Roberts

By Dale Roberts

Special to the Financial Independence Hub

The traditional balanced portfolio is built for the current economic environment. It is built upon the premise, or guess, that we will remain in a disinflationary environment. It is all that today’s investor has known. In a disinflationary environment US and Canadian stocks and other developed markets perform well. US and Canadian bonds perform well. As you will have noticed, if you have a sensible balanced portfolio or even a portfolio that is heavily weighted to stocks – you’ve done very well. But things could change. The economic conditions could change. For that possibility you might consider a portfolio that is built for any economic condition – the Permanent Portfolio.

The portfolio blind spot

I “got” the portfolio blind spot framing from a Canadian financial planner. The planner stated that for them, inflation was a blind spot. It was not something that the planner understood or knew how to address.

So if many portfolio managers and financial planners don’t consider serious inflation or the possibility for a change in economic conditions (economic regimes) it’s not surprising that the everyday retail investor would not ‘get it’.

And by the way, I am told that advisors and planners are not trained ‘on this.’ They are not trained to protect your wealth in all economic conditions. The word “stagflation” does not show up in their training materials.

And for the record, here are the economic possibilities and what works best in each regime. The chart is courtesy of ReSolve Asset Management.

When you have a blind spot you could get side swiped.

As I detailed in the lost decade for US stocks, there are periods (long periods) when stocks simply don’t work. They deliver no returns, or no real returns (when we factor in inflation) for extended periods – even a decade or more.

For example, US stocks delivered no real returns for a 15 year period from 1968 through 1982. You can thank inflation for that.

Each stock market is different (that is US vs Canada vs other International) but that trend and fact remains. Stocks don’t always work.

All positive US stock gains over the last 130 years have occurred in disinflationary periods.

Not only that, the traditional balanced portfolio can also deliver no real returns for extended periods. The chart is for US stocks and bonds, but the conditions would not change change materially when we substitute or add in other developed market stocks and bonds.

Where stock diversification would have helped (marginally) is in the early 2000’s period. Canadian and International developed markets did not suffer to the same degree, as did US stocks in the dotcom crash. It was the US stock market that suffered from greater euphoria and greater over-valuation “issues”. You mean, like today? You might ask.

So how do you build a simple portfolio to protect and prosper through all economic conditions?

The Permanent Portfolio

There are four economic conditions that can exist. The economy can grow or the economy can shrink – economic contraction. We can have inflation and we can have deflation.

And yes we can have periods of stagnation or muted movements for each of the above.

With inflation prices are increasing and so is your cost of living.

With deflation prices are falling and the cost of living is decreasing.

Putting it all together, we can have four quadrants or economic conditions.

- Inflation in a period of economic growth.

- Inflation in a period of economic contraction.

- Deflation in a period of economic growth.

- Deflation in a period of economic contraction.

Have another look that chart from ReSolve and you’ll see the economic conditions of the last 120 years and more.

Something is always working

The Permanent Portfolio is designed to hold assets that will perform in each economic environment. Something is always working.

Stocks for economic growth

- 25% in stocks to provide a strong return during times of prosperity.

Bonds for deflation

- 25% in long-term bonds, which do well during times of prosperity and during times of deflation (but which do poorly during other economic cycles).

Cash for economic contraction

- 25% in cash to hedge against periods of recessions or depressions.

Gold for inflation

- 25% in gold and precious metals to provide protection during periods of inflation.

An investor will rebalance between the portfolio assets on a quarterly, semi-annual basis. You might also choose to rebalance when one asset moves well above its 25% target. You would move those proceeds to the underperforming asset.

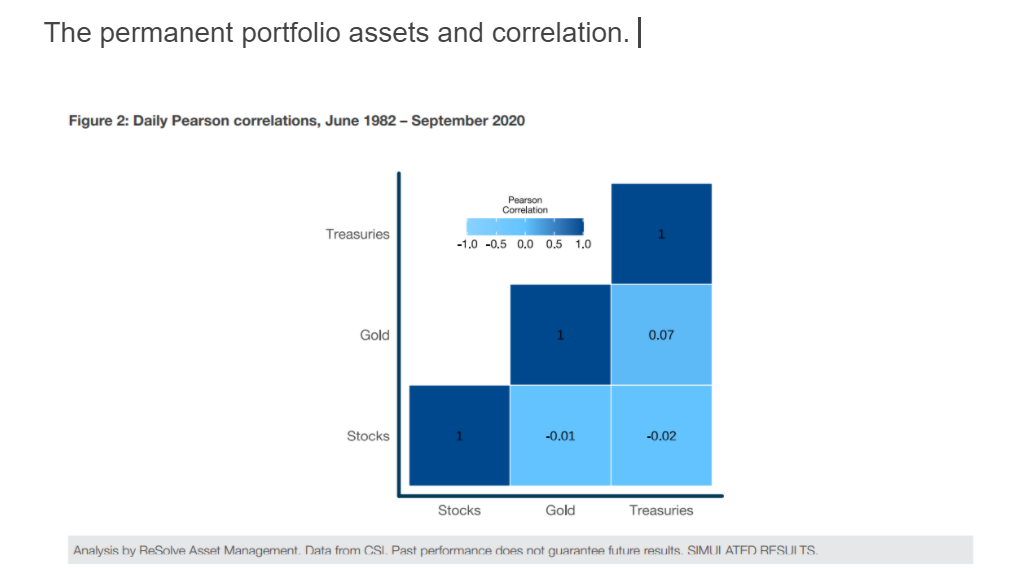

We can see that the assets are non correlated. They mostly move in opposite directions over time. Here, Resolve looks at Treasuries, gold and stocks.

Of course, having 25% of your portfolio in stocks is counterintuitive for most investors. It’s simply too conservative. And holding 25% in gold? Most would take a pass.

But given that, most would be giving up that inflation fight.

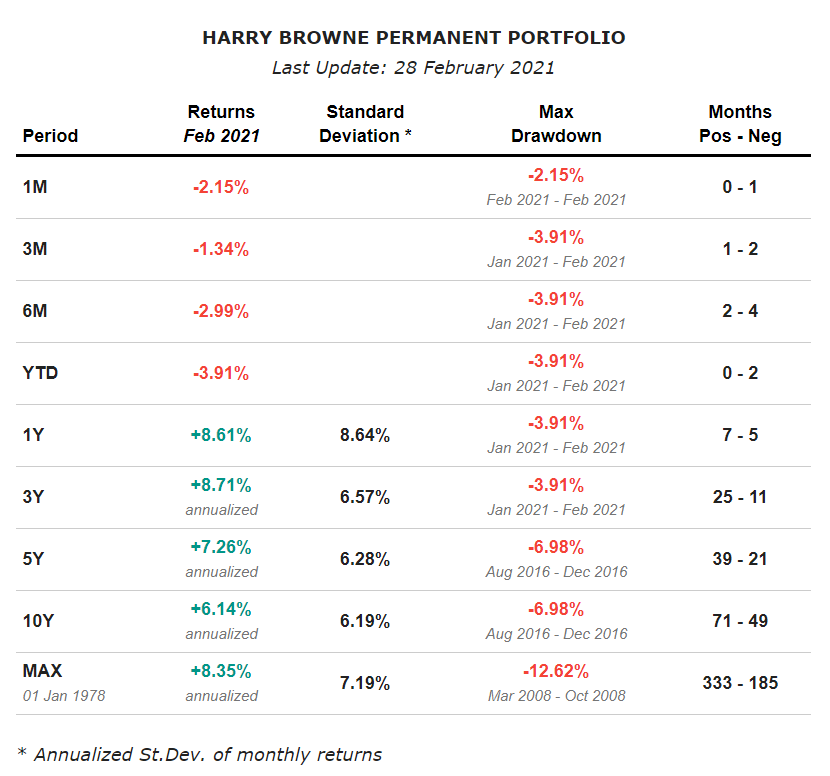

That said, the permanent portfolio would have delivered very solid results over the decades. Here’s a table courtesy of lazyportfolioetf.com. You’ll notice the name Harry Browne in the title. Mr. Browne popularized the Permanent Portfolio concept.

We see that those are traditional balanced portfolio returns in the area of 6%-8%. If you move back into the early 1970s and during a period of rampant inflation (stagflation), the permanent portfolio returns move towards 9% annual.

When we go back to the 70’s we enter and include the period of stagflation (when most everything failed). But not gold, it went up almost ten fold.

Stock-like returns with bond-like risk

So how do we get stock-like returns with the risk levels of bonds? And also with a portfolio that is only 25% stocks?

The magic is in the rebalancing. Once again as we move through various economic cycles and stock market and bond market shocks, different asset classes will take its turn in delivering greater, and positive returns. That value will be sold in stages and by way of rebalancing, it will be transferred to another (more out of favour) asset or assets that will be fully primed and ready to support the portfolio for when it’s time for that asset to shine. Something is always working, and the profits are harvested and redistributed.

That rebalancing creates additional returns beyond the sum of the total parts.

It is called the rebalancing premium.

2+2+2+2 = 9.

The US ETF Permanent Portfolio

Keep in mind that the original Permanent Portfolio has a US bias. That bias will add strengths in certain periods, and a weakness in other periods.

Here’s how the US ETF portfolio might look. 25% equal weighting.

- US stocks – IVV

- US bonds – TLT

- Gold – GLD

- Cash – SHY

You can certainly use an ultra short bond ETF or a cash ETF for that cash component.

The Canadian ETF Permanent Portfolio

We will remove that US stock home bias. Instead we will move to a global stock ETF offering. The ETF and index in use is currently overweight to the US market.

This is a Canadian Dollar portfolio. 25% equal weighting.

- Global stocks – XWD

- US bonds – ZTL

- Gold – KILO

- Cash ETF

There are many options in Canada for ‘high’ interest savings accounts, including this offering from Purpose. You might also choose to use an ultra-short bond ETF, or you can cheat a little bit with a 1-5 year bond ETF.

Investors can go with an option such as EQ Bank that is offering much higher rates. They offer RRSP and TFSA accounts.

The returns for the Permanent Portfolio from 2000

Using the US portfolio. From January of 2000 to end of 2020.

We see identical returns but with much less volatility. And certainly that is an unfortunate start date for a US stock portfolio. But that is the idea of managing risks, especially for a retiree or near retiree. Your retirement might land on a very unfortunate start date.

But what about in more recent times?

Surprisingly, we are not giving up much in 1-year to 5-year periods.

Here are the returns of the individual assets for the full period from 2000-2020.

And the monthly correlations, or make that non-correlations. Obviously gold can work for many reasons, it does not need stagflation to deliver. Gold is also not a perfect hedge for inflation in all inflationary periods.

Here is a terrific post on gold courtesy of Banker on Wheels.

Should you go Permanent Portfolio?

I won’t tell you how to invest. I put ideas on the table and you decide for yourself. From this blog post you can take away the big picture – protecting your portfolio from a change in economic regimes.

Today, most everyone suffers from a recency bias. Advisors and retail investors alike.

Whether or not you choose to protect your portfolio wealth from that potential for change is up to you. But to do nothing is a choice. Let’s turn to Neil Peart, drummer and lyricist for RUSH.

To do nothing (if you are not protected) is a bet that economic conditions will largely stay the same. It might be an expensive bet.

Check your portfolio assets against economic conditions. Check in with your advisor or planner. How are you protected? It is important to have that discussion.

If you are early in the accumulation stage it may be quite reasonable to keep an all-equity or stock heavy portfolio. If you have a high risk tolerance you can keep on buying at those lower prices when the stock markets correct. Stocks (owning great companies) are a wonderful long term growth asset, arguably the best of the bunch.

Fixing your portfolio holes

Should you decide that you want more protection from inflation you don’t need to blow up your portfolio and reshape it to an exact Permanent Portfolio. It’s easy to add cash and bonds. You can add a gold ETF to the mix. I will leave the portfolio weighting up to you, but historically it would take a serious weighting for gold to save the day in an event such as robust inflation or lasting stagflation.

If you already hold a traditional balanced portfolio, you could rebalance some assets to a gold holding over time. New monies could also then build that gold position. You could essentially bolt on gold to the existing portfolio. But keep in mind the magic of US long term treasuries in their ability to go up when stocks go down. They punch above their weight as stock market risk managers.

You’ll need some cash and/or very short term bond ETFs in the mix as well to help “Permanent” that portfolio.

If you hold a one ticket asset allocation ETF, you could sprinkle that one ticket with some gold.

My readers will know that I hold gold stock ETFs and physical gold hold ETFs and that I also invest in bitcoin. I see that bitcoin as a new gold, and perhaps a super gold. There is the risk bitcoin continues to steal attention from ‘real’ gold.

I am more than happy to hold old gold and new gold.

Protecting my retirement

I think that we will most likely stay in a disinflationary environment. Most of the economic forces are still disinflationary, but I will not put our retirement on the line. I will not invest based on that guess.

While I don’t hold a Permanent Portfolio, I have assets that will protect for each economic regime. I go at that process with a hybrid strategy.

I’ll be back next week with another post on all-season ETF portfolios including the 7-Twelve ETF portfolio. One might be able to do one better than the Permanent Portfolio.

Thanks for reading. Please offer your thoughts in the comment section. Are you protected for all economic conditions?

Follow me on Twitter, where I Tweet too much.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on March 27, 2021 and is republished on the Hub with his permission.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on March 27, 2021 and is republished on the Hub with his permission.

Thanks for this very interesting article. The percent of periods with a positive return table was enlightening. I’d be interested on your take on the Golden Butterfly portfolio.