As Didi says in the novel (Findependence Day), “There’s no point climbing the Tower of Wealth when you’re still mired in the basement of debt.” If you owe credit-card debt still charging an usurous 20% per annum, forget about building wealth: focus on eliminating that debt. And once done, focus on paying off your mortgage. As Theo says in the novel, “The foundation of financial independence is a paid-for house.”

We think Now is a bad time to Buy Bonds … Here’s Why

Recently a friend asked, “Pat, I see that several prominent Canadian investor advisors recently wrote articles that said it’s a bad time to buy bonds right now. Do you agree?”

He was surprised when I told him I haven’t bought any bonds for myself since the 1990s. I haven’t bought any for our Portfolio Management clients in the last couple of decades, except on client request.

In the 1990s, I used to buy “strip bonds” for myself and my clients, as RRSP investments. This was the Golden Age of bond investing. Back then, high-quality bonds yielded almost as much, pre-tax, as the historical returns on stocks. In addition, they were more stable than stocks and provided fixed income that simplified financial planning.

Bonds have tax disadvantages, of course. But you can neutralize those disadvantages by holding your bonds in RRSPs and other registered plans.

The big difference back then was that bond yields and interest rates were much higher than usual. That’s because we were still coming out of (or “cleaning up after,” you might say) the inflationary bulge of the 1970s and 1980s.

In the 1980s, government policies pushed up interest rates and took other measures to hobble inflation, and it worked. But interest rates stayed high for a long time after the government policies broke the back of inflation: kind of like finishing the antibiotic prescription after the infection goes away.

Long-time readers know my general view on the stocks-versus-bonds dilemma. When interest rates are as low as they have been in recent decades, high-quality stocks on the whole are vastly superior to bonds. However, you have to understand the differences between the two. For one thing, stocks are more volatile than bonds. But volatility and safety are two different things.

Volatility refers to sharp price fluctuations, often due to short-term uncertainty and the randomness of short-term market movements. Safety refers to the risk of permanent loss.

Bonds improve portfolio stability but cut investment returns

You might say that what you get from bonds is the opposite of what you get from the stock market.

Inflation near-automatically reduces the purchasing power of bonds. Inflation can also hurt the returns you make in the stock market, of course. However, companies you invest in can take steps to cut the costs of inflation. They can pass on cost increases to their customers. They can introduce new processes and equipment to improve productivity and cut their costs. Continue Reading…

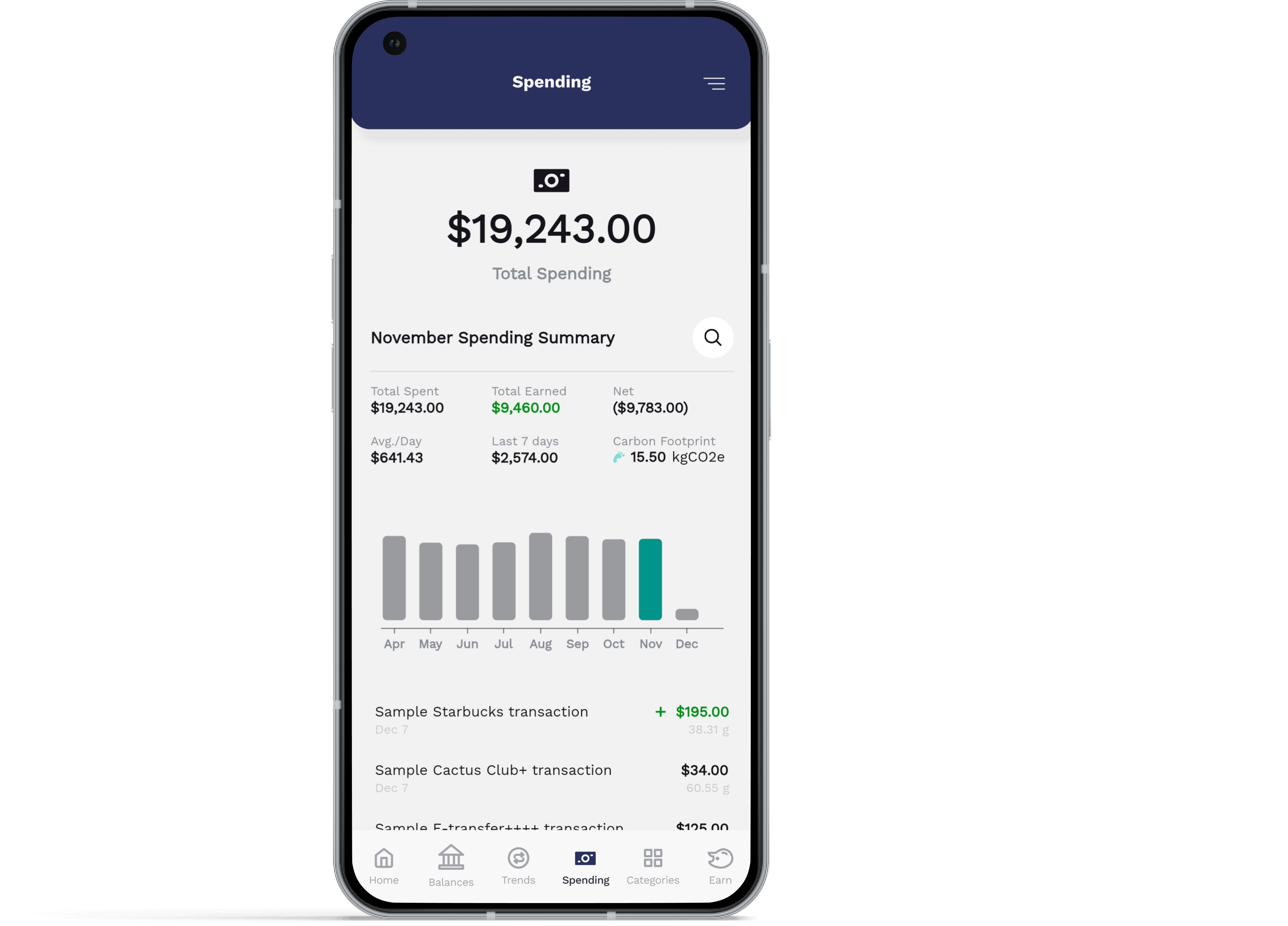

In the realm of personal finance, understanding where your money goes is essential for financial success. Tracking expenses provides valuable insights into spending habits and empowers individuals to align their finances with their goals. Whether you’re a seasoned budgeter or just starting your financial journey, mastering expense management is key.

Most people have multiple financial institutions, credit cards, store cards, etc., making expense tracking complicated. It’s also easy to lose track of automatic subscriptions that renew on a monthly basis, like that local gym you joined but have got out of the habit of using.

Luckily, there are tools available to simplify our ever-increasing complex financial lives. For many years Mint was a popular budgeting tool owned by Intuit. But as of March 23, 2024, Mint is being decommissioned, leaving many people searching for a free replacement.

One tool that has recently launched as a replacement for Mint in Canada is Wilbur, a free budgeting app that automatically connects to your bank account. In addition, Wilbur allows people (at no obligation) to answer surveys for a little extra side cash.

The personal finance experts at Wilbur have put together the following series of tips to help people get a handle on their finances.

1.) Assess Your Accounts

Begin by reviewing your financial accounts, including bank statements and credit card transactions. Take note of recurring expenses and identify patterns in your spending. Understanding your financial habits lays the groundwork for effective expense tracking. Wilbur has a handy feature in that it automatically identifies those recurring subscriptions, giving you the necessarily information to plan for the payment or simply cancel it to save money!

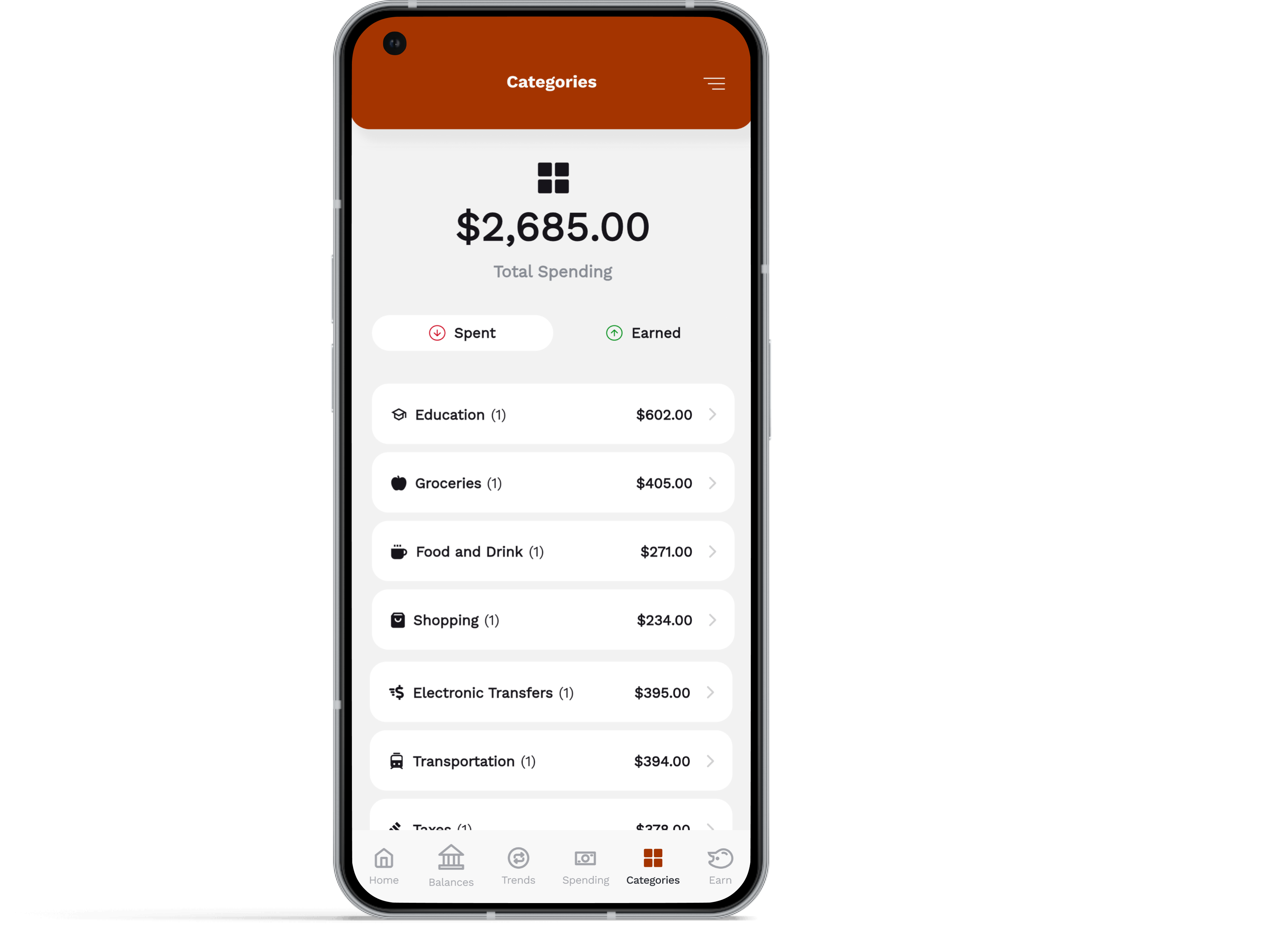

2.) Categorize Your Expenses

Organize your expenses into categories to gain clarity on your spending habits. Categories may include essentials like housing and utilities, as well as discretionary spending on entertainment and dining out. Utilize features in apps like Wilbur to automatically categorize transactions and simplify the process.

3.) Craft Your Budget with Wilbur

Once you’ve categorized your expenses, create a budget that reflects your financial priorities. Allocate funds for necessities, wants, and savings/debt repayment using the 50/30/20 budgeting method. Use the budgeting app to track expenses and set budgeting goals for each expense category.

4.) Consider a Side Gig

If you find you’re not making ends meet, find a side hustle. A survey by H&R Block in March 2023 found that 28% of Canadians had some kind of side gig. Side hustles are found everywhere, even in the Wilbur budgeting app. Wilbur offers the opportunity to earn between $1 and $5 by answering a survey, simply by clicking a link from within the app. It’s a convenient way to monetize a spare 10 minutes of your day. Clearly not going to get rich off it, but in today’s inflationary times, every little bit counts. Continue Reading…

Years of capital appreciation due to decades of compounding and proper money management has paid handsomely in the growth of our net worth and financial wellbeing. Now, 33 years later, do we still need to be diligent in monitoring our spending and outflows, or is now the time to seize the day and go first class? Eat in trendy restaurants, be seen and show off our wealth?

This is definitely not our style …

Flying under the radar living abohemian lifestyle is more like us, and we’re still herelivin’ the dream.

In fact, some family members and friends consider us “poor” as compared to their consumer-based standards. That’s fine with us. We have not owned a car for years and we tend to live in foreign countries where we can geographically arbitrage value for money spent. We prefer experiencing cultures and cuisine as compared to a shiny new car, club membership and debt payments.

We are just trying to make it to Friday

There are many ways to live a life, and our choice is unique to us. It’s a lifestyle not a vacation and our approach is one that we created based on our personal values and interests.

We now use more private drivers than chicken buses, stay in pricier hotels (not always a better choice), and we’ve set up a stable, semi-permanent home base in Chapala, Mexico.

We donate freely, giving our time and money, helping others less fortunate, as well as teaching people better money management and life skills.

There are needs everywhere and we do our best to contribute. As always, we want results rather than throwing money at a problem to feel good and brag about it.

Checking back in with the 4% rule, we took a look at what that number would be for us today and both of us asked “How would increasing our spending to that amount change our lives?” Granted, it’s not Bill Gates’ level, but how much more can we eat, drink, travel, be merry and give away?

But that’s us.

What about you?

Is it time for you to flip the switch from saving and being frugal for your future – to enjoying a higher standard of living and giving back to the community?

Below are a couple of suggestions which might clarify this question for you.

Know where you are

Life circumstances change.

None of us know our exit date from this planet. As each day passes, we are one day closer to the end of our adventure. But you could check some actuarial tables to see where you stand in general. We are not saying throw caution to the wind and start “X-ing” out days on your calendar. Rather, utilize this bit of information to get a clearer picture of where you might be.

Imagine if you knew your Date of Death. Would that change your spending habits or the way you live?

Other thoughts

Have you or your spouse had an awakening in regards to health? Do you want to open a foundation that produces results and wealth? Begin a new business or leave a particularly handsome legacy for your grandchildren? Continue Reading…

Exploring the critical role of budgeting in debt reduction and the journey to financial independence, we’ve gathered insights from founders and CEOs among others.

From the disciplined approach of discipline and frugality through budgeting to the strategic perspective of budgeting and debt management for independence, here are the diverse experiences of ten professionals who’ve successfully navigated their finances.

Discipline and Frugality

Debt Reduction and Savings

A Financial Compass

Fiscal Success

Navigating Finances

Clarity and Control

Financial Stability and Empowerment

A Roadmap to Financial Freedom

Enhanced Financial Control

Debt Management for Independence

Discipline and Frugality

Being in a financial crisis is not uncommon for the average person; we have all seen people in our lives suffer under the massive weight of debt and how it subsequently affects our quality of life. To get out of debt, you need to be disciplined and frugal. Following a budget needs to become a regular part of your life so that you can achieve financial freedom sooner rather than later.

When you budget, following a rule like 50/30/20, it helps you manage your income in a way that reduces your debt and allows you to live a fulfilled life while still preparing for any unexpected hiccups in the future.

When you budget following a ratio rule, you need to be flexible with the money allocated for “wants,” i.e., the 30 in the ratio. This means cutting out anything in your life that isn’t necessary—such as buying the extra coffee, eating takeout daily, or subscribing to services that you don’t use.

So, don’t allow yourself to fall into the lifestyle-creep trap. By cutting these non-essentials out, you can funnel the extra money into your essentials and debt repayments—which loosens the burden for you and your future.

That being said, you don’t have to make yourself burnt out from budgeting; it’s okay to treat yourself and splurge a little as a reward for doing well with your financial goals. You just need to know your limits and where to draw the line. — Zach Robbins, Founder, Loanfolk

Debt Reduction and Savings

Budgeting is hugely important for reducing debt and achieving financial independence because it can help you determine how much you can contribute each paycheck toward these goals. For instance, with a budget, you can learn exactly how much you have left over each month after essential expenses, such as rent, groceries, and electricity. Once you have this number, you can allocate a portion of your remaining income to reducing debt and savings.

For me, personally, budgeting helps me realize when I’ve overspent in certain areas and need to rein it in so that I will have enough to put towards savings or debt payoff. — Meredith Lepore, Content Strategist/Editor/Writer, Credello

A Financial Compass

Budgeting plays a crucial role in reducing debt and achieving financial independence. By ensuring you spend within your means, it acts as a financial compass.

For instance, when I faced a mounting credit card debt, which mirrored the national average of around $6,000, budgeting became my lifeline. It wasn’t just about tracking expenses but making conscious choices about spending.

This approach helped me not only clear my debt but also build a savings habit, leading to a more secure financial future. — Tobias Liebsch, Co-Founder, Fintalent.io

Fiscal Success

Budgeting is the financial roadmap to success. As a tech CEO, it’s been my steering wheel on the road to fiscal independence. An example would be when we faced a financial bottleneck. We reevaluated our costs, cutting back on non-essential company perks, and reallocated those funds towards paying down our debt.

Thanks to strategic budgeting, we were debt-free in less than a year. Therefore, proper budgeting isn’t just number-crunching; it’s crucial for cuts, savings, and gains, propelling us toward the land of fiscal freedom. — Abid Salahi, Co-founder & CEO, FinlyWealth

Navigating Finances

The importance of budgeting in the journey toward reducing debt and achieving financial independence cannot be overstated—it’s the financial equivalent of a compass on a voyage across the open sea. Without it, you’re essentially navigating blind, at the mercy of the winds and currents. But with it, you can chart a course to your destination, making informed decisions that keep you on track.

There was a time when my financial situation felt like a sinking ship—credit card debt and personal loans were the water flooding in, and I was desperately bailing it out with a leaky bucket. I realized that if I wanted to reach the shores of financial independence; I needed a better strategy.

That’s when I embraced budgeting with open arms. I started by laying out all my expenses and income, categorizing them with the meticulousness of a librarian. It was eye-opening to see where my money was actually going, rather than where I thought it was going. I discovered leaks in my spending—money trickling away on things that, frankly, weren’t adding much value to my life, like a gym membership I barely used or subscription services that just piled up.

Armed with this knowledge, I began to plug these leaks, reallocating those funds toward paying off my debt. Every dollar saved was like a bucket of water thrown overboard, lightening the load and bringing my ship higher in the water.

But budgeting did more than just help me manage my debt; it empowered me. It transformed my relationship with money from one of anxiety and scarcity to one of control and abundance. Through disciplined budgeting, I was able to pay off my debts significantly faster than I had thought possible. More importantly, it laid the foundation for building savings and investments, guiding me toward the ultimate goal of financial independence.

The journey wasn’t always smooth sailing. There were months when unexpected expenses threw me off course, but because I had a budget, I could adjust my sails and get back on track. Budgeting gave me the flexibility to deal with financial storms without capsizing. — Michael Dion, Chief Finance Nerd, F9 Finance

Clarity and Control

Budgeting is absolutely critical for getting out of debt and achieving financial independence. When I first started trying to pay down my student loans and credit card debt in my early 20s, I felt completely overwhelmed. I was living paycheck to paycheck and had no idea where my money was going each month. Continue Reading…

When cash, high quality bonds, and other safe assets offer little yield, investors get caught between a rock and a hard place. They can either (1) accept lower returns and maintain their allocation to safe assets or (2) liquidate safe assets and invest the proceeds in riskier assets such as equities, high yield bonds, private equity, etc.

Using history as a guide, when faced with this dilemma many people choose the second option. This decision initially produces favorable results as the increase in demand for stocks pushes prices up. However, as this reallocation progresses, prices reach levels which are unreasonable from a valuation perspective, and the likely returns from risk assets do not compensate investors for their associated risk. At this juncture, committing additional capital to risk assets becomes akin to picking up pennies in front of a steam roller. For the most part, this narrative is what played out across markets following the global financial crisis of 2008.

Following the global financial crisis, near-zero rates pushed investors to take more risk than they would have in a normal rate environment, which entailed making outsized allocations to stocks and other risk assets.

Unable to bear the thought of receiving negligible returns on safe assets, people continued to pile into risk assets even as their valuations became unsustainable.

Had central banks not begun raising rates aggressively in 2022 to combat inflation, it is entirely possible (and perhaps even likely) that stocks would have continued their ascent, valuations be damned!

Instead, rising rates provided risk assets with some worthy competition for the first time in over a decade, which in turn caused investors to rethink their asset mix and shed equity exposure.

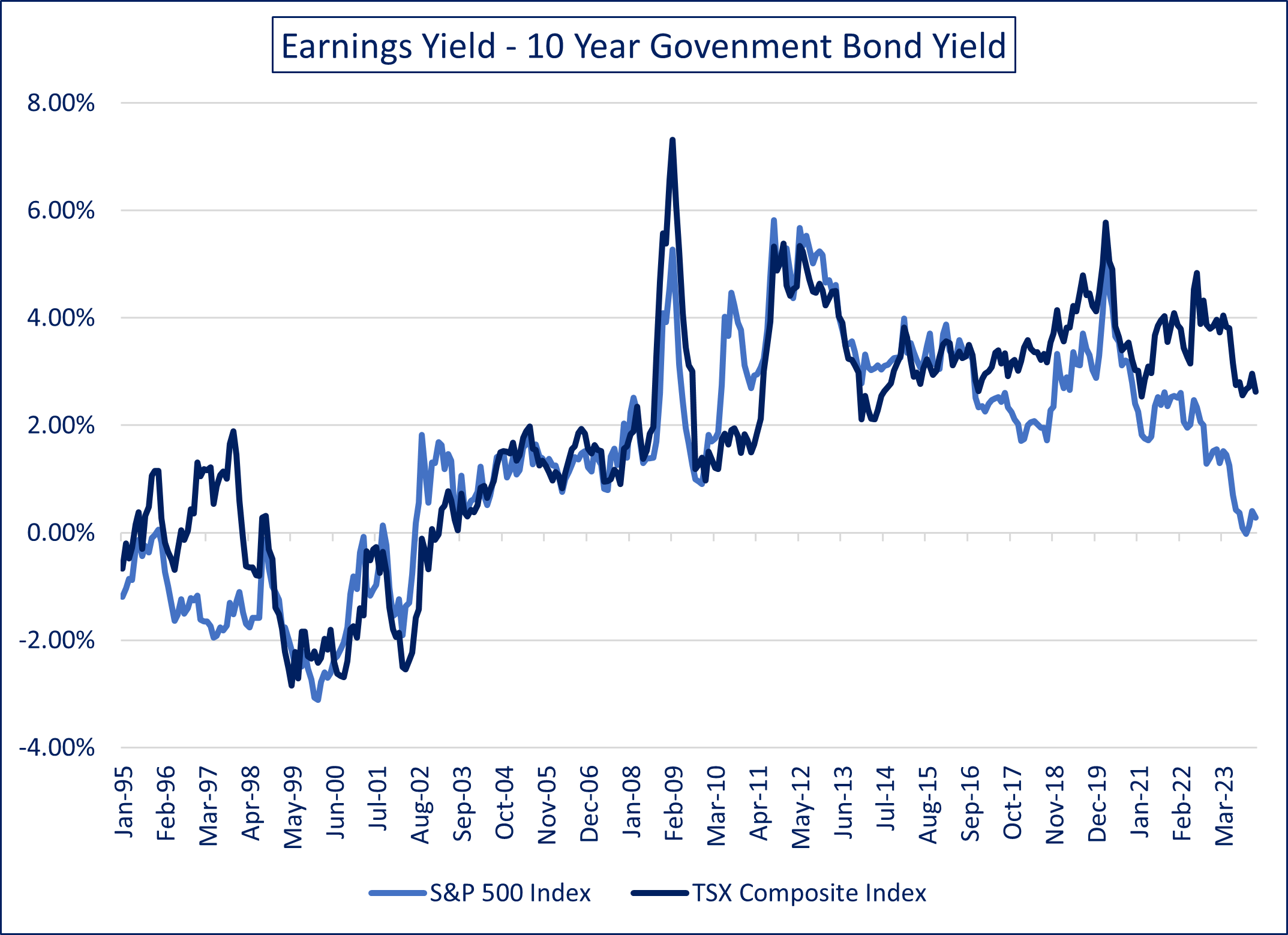

The Equity Risk Premium: A Stocks vs Bond Beauty Contest

The equity risk premium (ERP) can be loosely defined as the enticement which investors receive in exchange for leaving the safety of Uncle Sam to take their chances in the stock market. More specifically it is calculated by subtracting the 10-year Treasury yield from the earnings yield on stocks. For example, if the P/E of the S&P 500 is 20 (i.e. earnings yield of 5%) and the yield on 10-year Treasuries is 3%, the ERP would be 2%.

Historically, stocks tend to produce higher than average returns following elevated ERP levels. Intuitively this makes sense. When valuations are cheap relative to the yields on safe assets, investors are getting well compensated for bearing risk, which tends to portend strong equity markets. Conversely, at times when stock valuations are rich relative to yields on safe assets and investors are getting scantily compensated for taking risk, lower than average returns from stocks have tended to ensue.

Chart courtesy Outcome

At the end of 2020, the S&P 500 Index’s PE ratio stood at 20 (i.e. an earnings yield of 5%), which by no means can be considered a bargain. However, stocks were nonetheless rendered attractive by ultra-low rates on cash and high-quality bonds. It’s easy to look good when you have little competition!

By the end of 2021, the Index’s PE ratio was above 24 (i.e. an earnings yield of 4.2%). Stocks were even less enticing than valuations suggested, given that 10-year Treasury yields had risen from 0.9% to 1.5%. This set the stage for a decline in both prices and valuations in 2022.

From an ERP perspective, 2022’s decline in valuations did not make stocks less stretched vs. bonds. The contraction in multiples (i.e. increase in earnings yield) was more than offset by a rise in bonds yields, thereby causing the ERP to be lower at the end of 2022 than it was at the start of the year.

In 2023, the S&P 500’s PE ratio expanded from approx. 18 to 23, which was not accompanied by any significant change in 10-year Treasury yields. By the end of the year, U.S. stock multiples had nearly regained the lofty levels of late 2021, despite the fact that Treasury yields had actually increased by over 2% during the two-year period.

In contrast, the relative valuation of Canadian stocks vs. bonds currently lies at levels that are neither high nor low relative to recent history.

Low Rates: The Growth Stock amphetamine

Growth companies, as the term implies, are those that are projected to have rapidly growing earnings for many years. Whereas an “old economy” stock such as Clorox or General Mills might be expected to grow its profits by 2%-10% per year, a juggernaut like NVIDIA could be expected to double its profits every year for the foreseeable future. Continue Reading…