By Aman Raina, Sage Investors.com

Special to the Financial Independence Hub

We’ve been hearing a lot of a new type of investing management model. A “Robo-Advisor” is an online-oriented service that automatically selects and manages a portfolio that is conducive to an investor’s risk tolerance.

There has been a lot of commentary about the prospects of this type of service gaining traction, especially with younger people or those with minimal assets but who want to get exposure to the overall stock market without doing all the legwork.

Much of this revolves around offering investors more transparency as it pertains to costs as well as back-office efficiencies and back-office savings that investors can leverage. The robo-advisor investment ideology revolves around a passive investment strategy by utilizing low commission Exchange Traded Funds (ETFs) allocated across various asset classes and that are held for long periods of time. Periodically, the asset mix is automatically adjusted if certain percentage makeups become too high or too low. A wealth of research has shown that a passively managed portfolio of ETTs can outperform a portfolio of actively managed assets.

This is all well and good. Ultimately, what will drive this service is the performance of these algorithm-managed portfolios. Instead of writing about these services in theory, I thought I would put my money where my mouth is and actually invest some money with a Robo-Advisor service and blog about the whole experience. More importantly, I will track the performance and costs these services generate.

Expect the banks to jump in

In Canada there has been a surge of start-up/independent companies offering Robo-Advisor services. At this point they are mostly independent companies but at some point I wouldn’t be surprised to see the big brokerage companies and banks jump in with similar offerings. For my test drive, I selected one service, which I ‘m not going to name for one main reason:

I don’t want to endorse any one service as more superior than another, as this is not intended to be a Consumer Reports exercise. There is enough commentary by other financial observers on the pros and cons of each respective service. These observations are about the effectiveness of the Robo-Advisor portfolio management process and strategy.

I selected this particular service (which I will herein call ROBO) because they had a low minimum contribution required and management fees that appears to be competitive versus other service. Finally, this service appears to have some people behind the “Robo” veil. ROBO is staffed by professionals, which is like having a dedicated financial advisor that can answer questions and provide more information on products.

The minimum investment required for ROBO is $5,000 with no commissions charged on asset values up to $5,000. When the portfolio crosses the $5,000 mark the management fee is then 0.50% of assets in excess of the $5,000. In other words if your portfolio value increases to $5,500 than you would pay 0.50% on the $500 which would be $2.50 for the year. The 0.50% management fee covers the associated trading costs for the portfolio. In addition there is a Management Expenses Ratio cost that is charged by each ETF held in the fund and varies in cost depending on asset type. I’ll have more to say about costs later.

The Journey Begins – Step 1: Registration

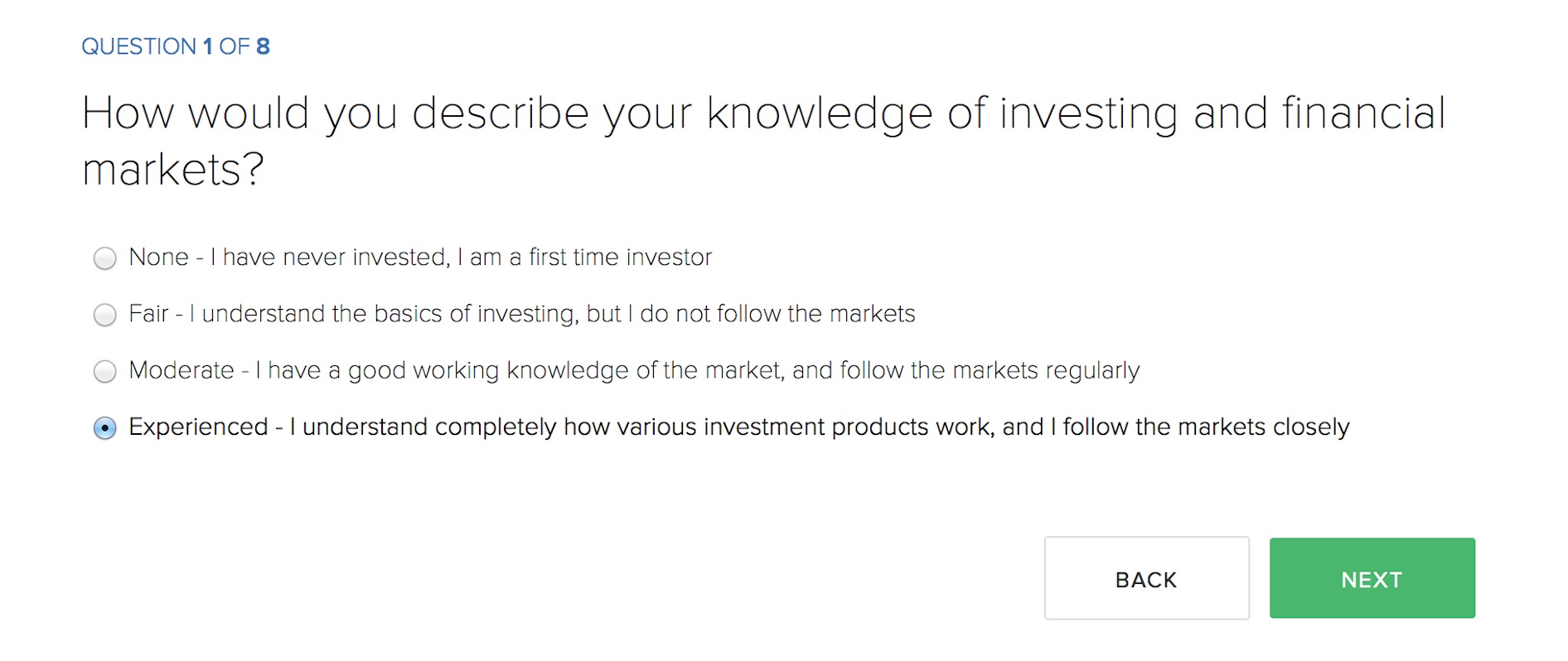

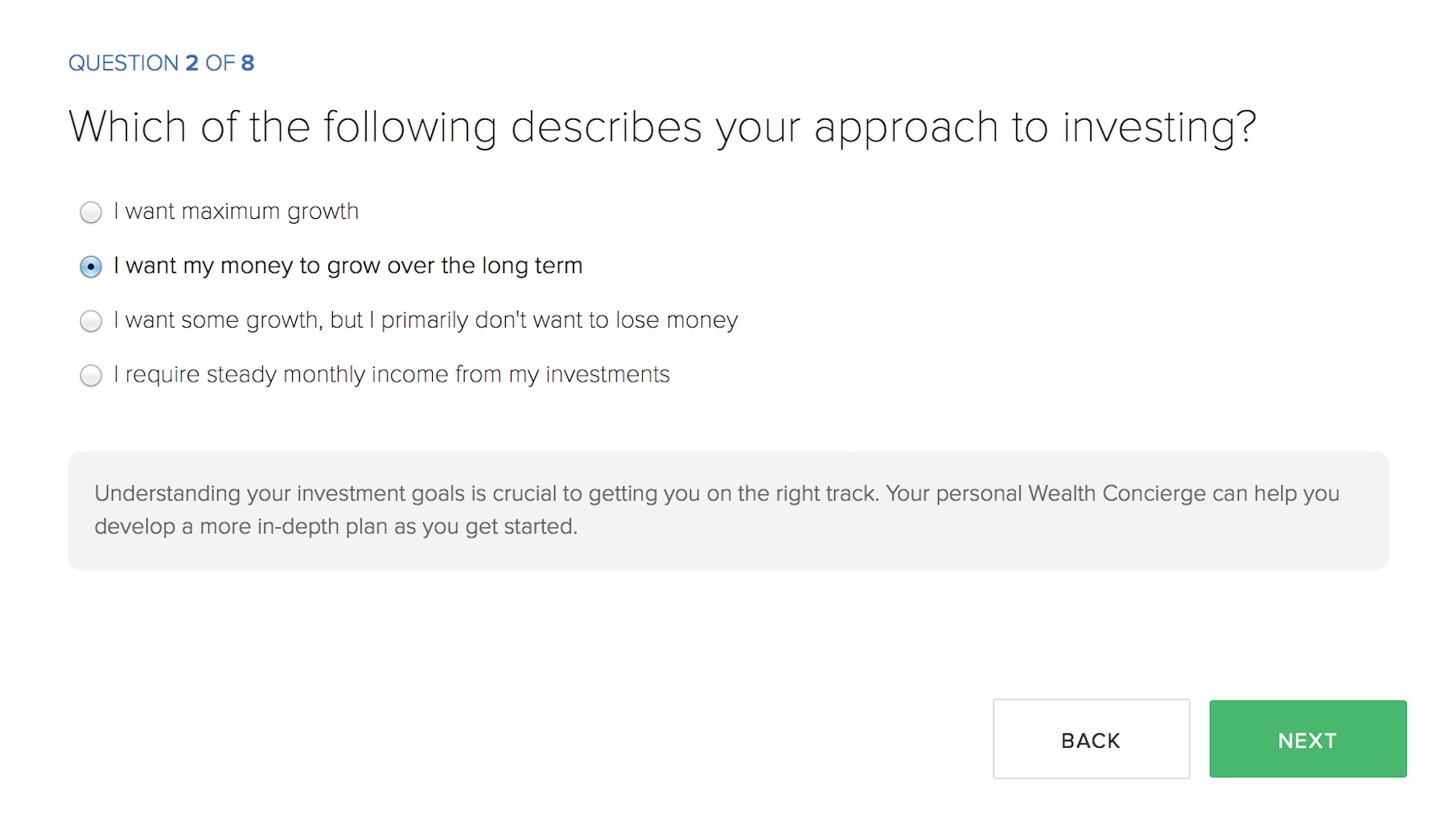

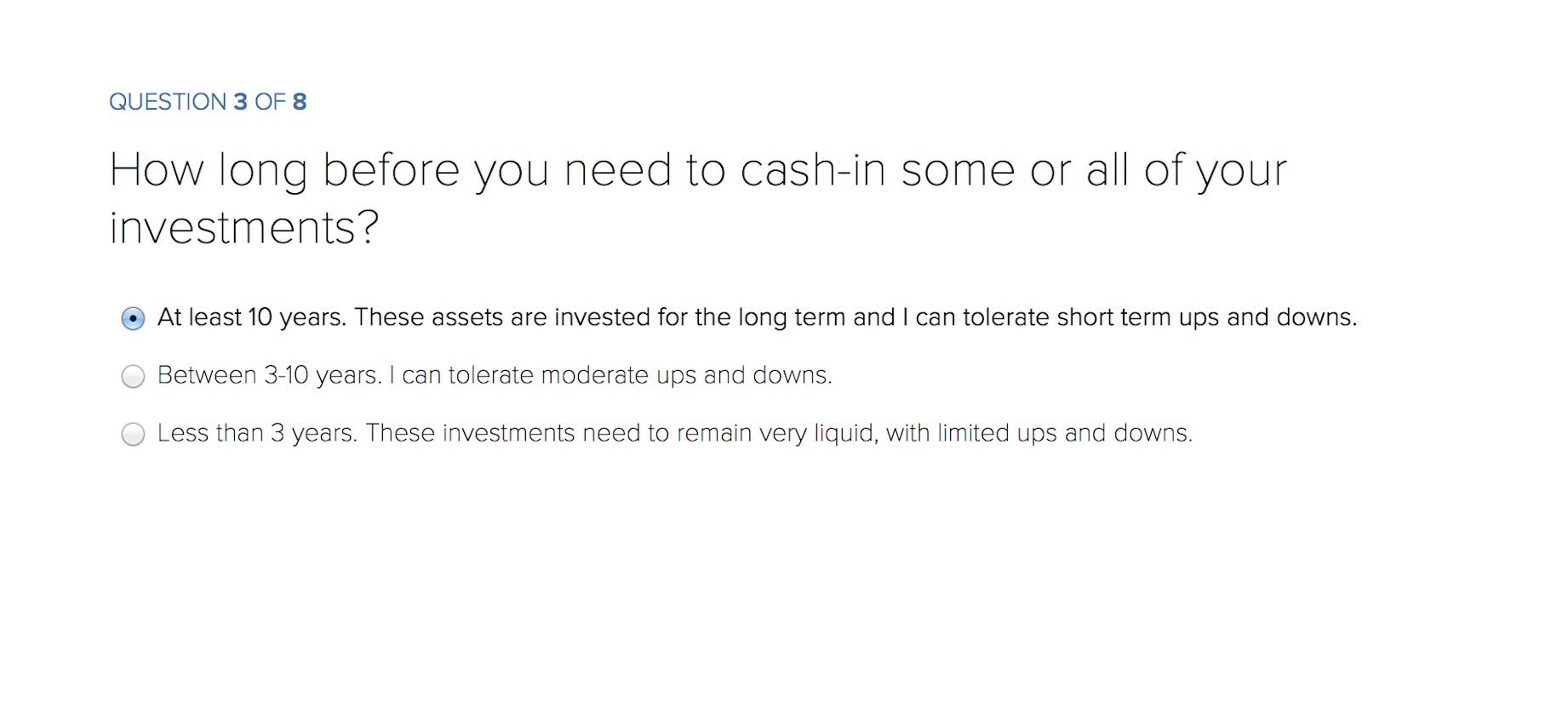

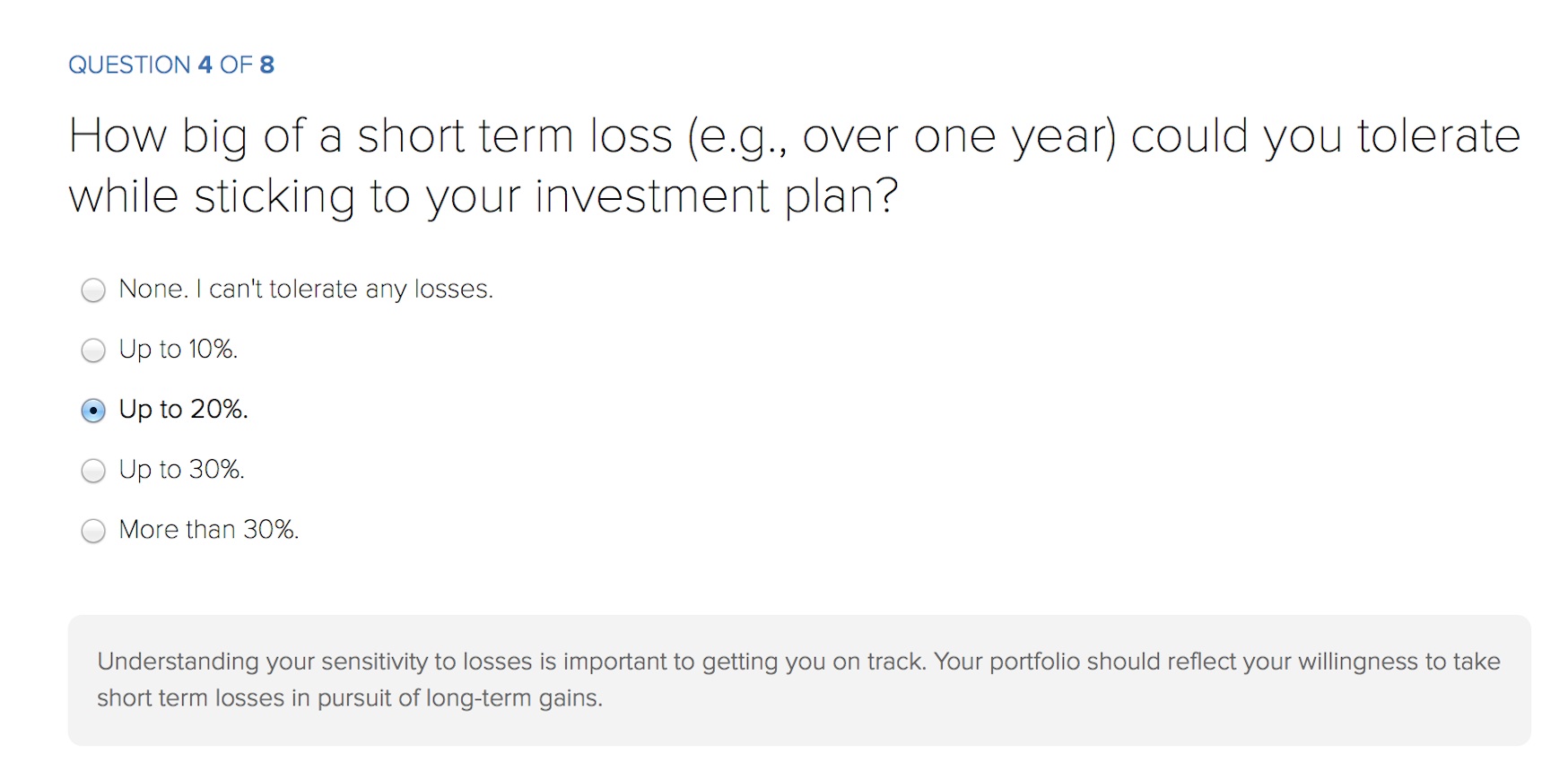

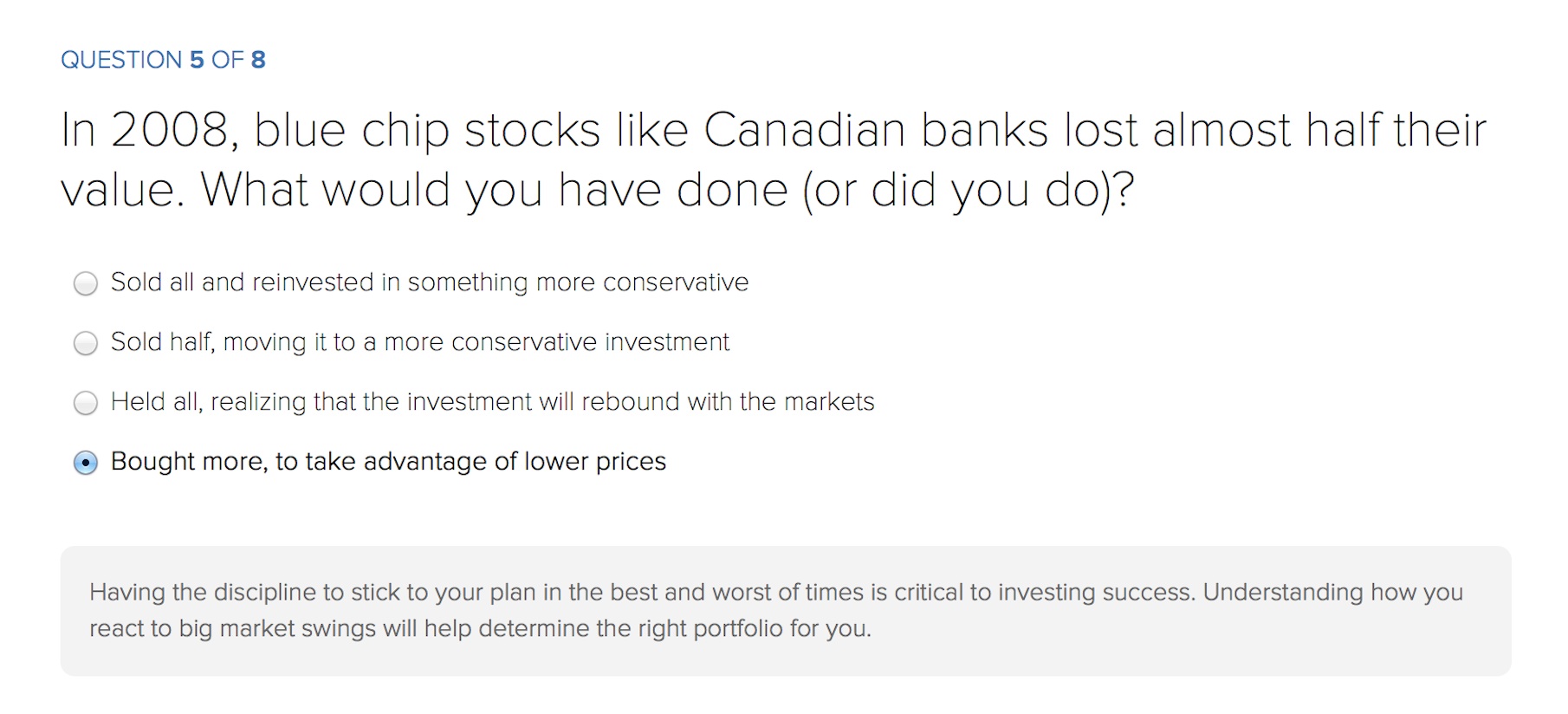

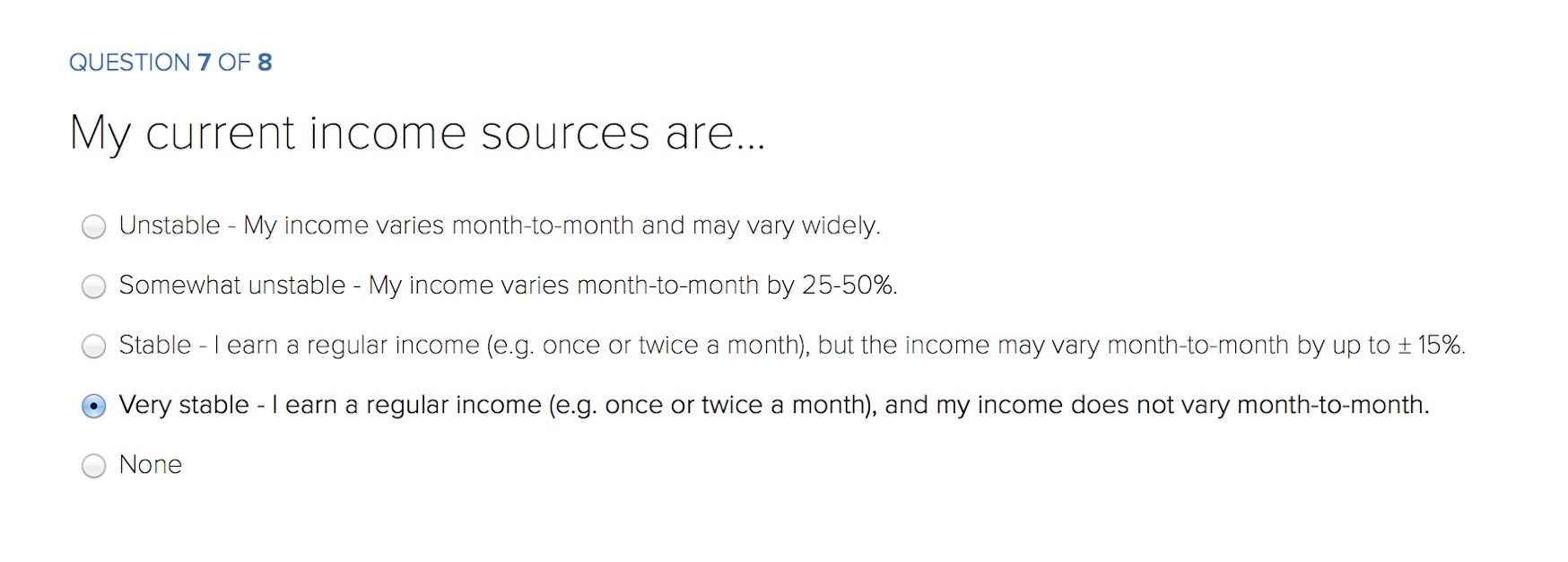

The entire registration process was done online. First, I had to answer a series of questions that gauged my risk tolerance level as well as my literacy of various financial concepts. Below are some of the questions I was asked. I did my best to answer these questions as honestly as possible.

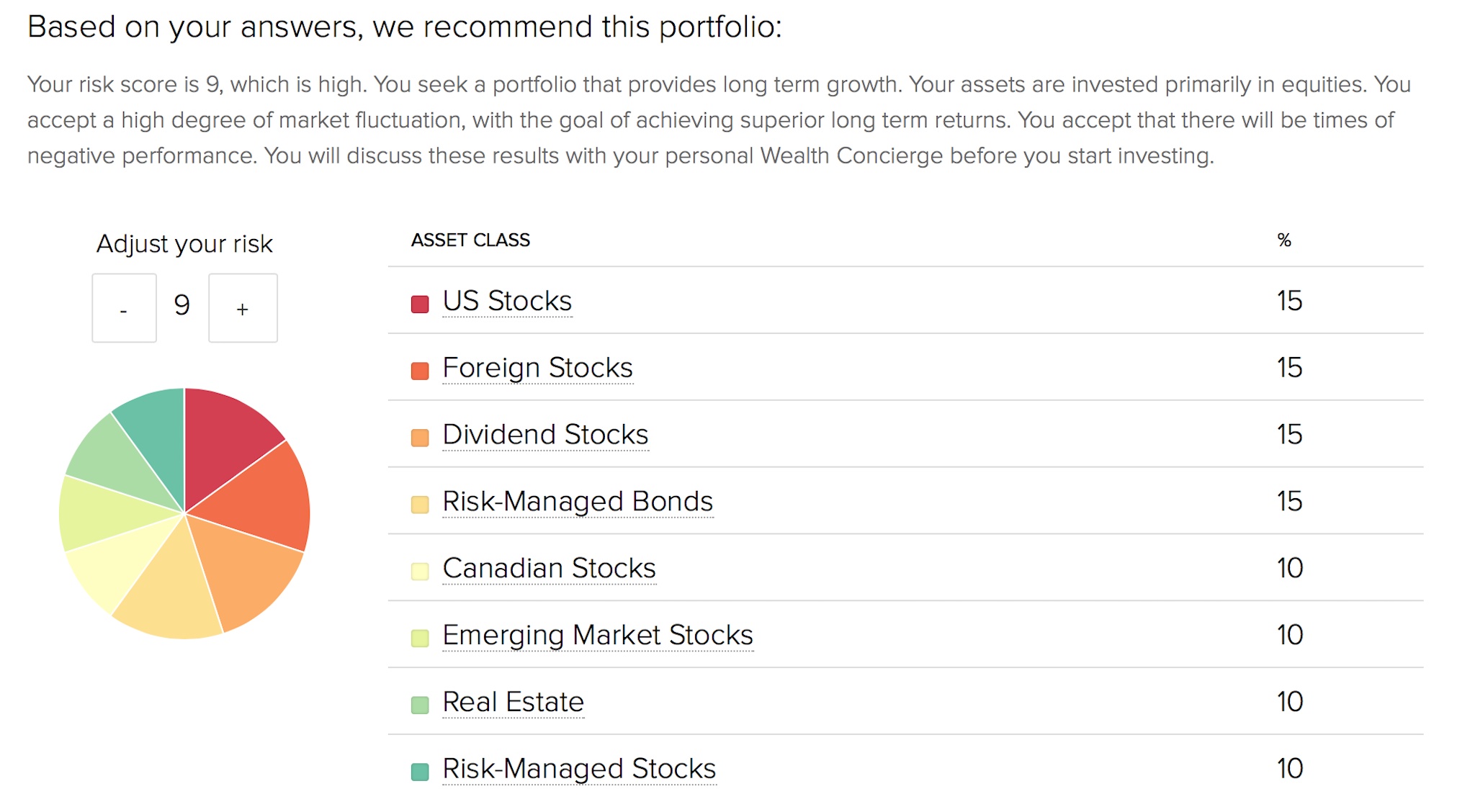

Step 2: My Recommended Portfolio.

Step 2: My Recommended Portfolio.

In a short period time after completing the survey, the site produced a summary of what kind of portfolio would reflect my risk tolerance. Below is the portfolio. From what I can read from the ROBO’s website, the portfolio created was selected from a series of canned reports that have been created by the ROBO. The report shows the breakdown of how much will be invested in each asset classed expressed as a percentage of total assets. In addition the report presents a score outlining my risk tolerance. You have the option of adjusting the score upon which the portfolio will adjust its percentage allocation dynamically. My risk profile came in at 9, which I thought was fine so I kept it at that level. I will go into more detail on the composition of the portfolio in my next post.

Step 3: Administration

Next I needed to formally complete the registration process by filling out the form to setup my account with the brokerage company who will be undertaking transactions on my behalf. Again this was all done online. Even the signatures were done online so it was all very seamless and painless. I also made sure to save a soft copy of the form for my own personal records.

Step 4: Schedule Meeting With Virtual Advisor

After filling out and signing off on the account registration documents, my final task for the moment was to schedule an appointment with one of the ROBO’s financial advisors. They would be my goto person to answer any questions. What will be interesting to observe going forward will also be what in the way of advice they provide. Again the site provides you with a list of blocked time available over the next several days so all you do is select what works for you. The appointment is done on the phone or through a video chat platform like Skype.

After scheduling the appointment, I received 3 emails that confirmed the following:

- Confirmation of appointment with ROBO advisor

- Confirmation of receipt of a test deposit. The ROBO will send you a small electronic deposit (In my case it was $0.56) to the bank account number you provided in your registration. I guess it’s a way for them to verify the account is legit. To complete the process, they ask you to send the money back via electronic payment. Essentially it’s a way to setup a link for the future when you will ultimately be transferring money into the ROBO portfolio.

- Finally, I received an email that confirmed my account has been setup and is ready to have funds transferred.

Step 5: Interview with ROBO Advisor

In the registration process, you are required to schedule an appointment with a ROBO financial advisor who is available to answer questions and explain the overall process. My meeting lasted about 20 minutes and was done on the phone.

In my meeting the ROBO Advisor asked some basic questions about how I found out about the service. The person (hereafter referred to as “he”) asked what kinds of investment accounts I have and my motivations for registering for their ROBO service. For the rest of the meeting, it was basically me asking questions to get some clarification on various elements, which I’ve highlighted below:

Question: How does rebalancing work?

My initial contribution would be invested in a variety of ETFs that invest in different asset classes. Based on the model portfolio created for me, my contribution is allocated on a percentage basis to these different asset classes. For example, the Canadian Equity component in my portfolio represents 20% of the overall portfolio, so 20% of my money will be invested in that asset class. When the percentage composition of the Canadian Equity component exceeds that 20% level and crosses a threshold (for example to 25) then some shares in the Canadian Equity ETF are sold automatically to bring the allocation down to 20%. The proceeds are then made available to allocate to another asset class who’s percentage allocation has fallen below their allocation level. This is called rebalancing. By keeping the asset allocations at the same level, it should provide a greater opportunity for the portfolio to yield a maximum return that is consistent with my risk profile. We’ll see if this is true. The ROBO explained that these rebalancing transactions on average would be executed 1-2 times per year, assuming deposited money once a year. Other situations where rebalancing could occur would be if you were making monthly contribution as well when income is paid into the fund from capital gains and dividends within a specific ETF. What I found interesting is that ROBO would not disclose what the threshold percentage level is because they fear people will front run and trade off the allocations on their own portfolios. The advisor said that these rebalancing transactions will be disclosed on my online account so I will know when these transactions occur. They are working on an implementing an email/text message alert system as well in the future.

Question: Can you provide some clarification on the fee structure?

The ROBO charges two types of fees. One is by the ROBO itself to cover trading and administration costs. The other is a Management Expense (MER) that is charged by the ETF company itself for the management and administration of the ETF product.

As mentioned previously, the fee charged by the ROBO covers all trades that are done within the portfolio. It is calculated on a percentage of assets basis. The ROBO has 4 levels of pricing. For assets under $100,000 the fee is 0.50% of total assets. For assets between $100,000 and $250,000 the fee is 0.50% but they also add a service call Tax Loss Harvesting which is some tweaking of your portfolio to make it more tax efficient. The rate falls as to as low as 0.35% for assets over $1 Million. For assets below $5,000 there are no management fees. Essentially they are letting you invest the first $5,000 commission free.

For the MER expenses that are charged by the ETF company, the ratio varies depending on the asset. My advisor told me that on average investors pay 0.25% in their portfolio. This charge is done behind the scenes so you will not see it directly coming out of your account.

Factoring in these two costs, my total costs for the portfolio on inception would be:

At most, goal costs will be 0.25% + 0.50% on any excess over the $5,000. So if I had $6,000 at the end of the year, my fees would be 0.25% x $5,000 + (6000-5000) x 0.50% = $17.

If it falls below $5,000 then my costs will initially be 0.25% of balance. For example, if the balance was $4,000, the fees would be $10.

While these fees are higher than what I’m paying to manage my own portfolios, they are still much cheaper than owning mutual funds that charge 2 – 4% of assets plus other annoying charges like deferred sales charges.

Question: How do I get statements and transcripts for my account?

The advisor informed me that all statements and transcripts as well as any tax-related slips will be available online and I can download and review at any time.

Question: What is your process for ETF selection and more specifically selection of specific ETF products from various companies (Vanguard etc)?

ETFs are the primary investment vehicle. The advisor explained that the ROBO uses ETFs that have the broadest exposure to the asset class. For example for the US exposure, the ROBO may use an ETF that invests in the S&P500 index or an ETF that invests in a more broader market of smaller and larger companies. In terms of products, the ROBO uses primarily a combination of iShares and Vanguard for equity positions but also would consider other index products such as the BMO line. For income-related components of the portfolio, the ROBO uses Purpose Investments for income-related components of the portfolio.

Question: What is the churn/turnover rate of the ETFs in the portfolio?

ROBO indicated that there should not be any meaningful turnover of the portfolio except in circumstances where a product is a better fit for the portfolio from a cost/return perspective. The advisor also made it clear that a new product would be added to the portfolio with existing positions continuing to be held to minimize transaction costs.

I will be watching this aspect of how ROBO manages the portfolio closely, as one of the big issues with active management was the continuous turnover of products in a portfolio that generated unnecessary commissions. Great for the manager. Lousy for the investor. The basic premise of this service is that investments are held for long periods of time with minimal churn.

Impressions of Registration Process

Overall, the process was very clean and seamless. I didn’t find myself getting bogged down in any area. I found the wordings to be easily understandable and probably would be understandable for someone with little financial experience. If I were to compare it to a process for setting up a trading account at a big bank, I would say the ROBO experience was much more tolerable. It pretty much met my expectations based on what other financial writers have commented about Robo Advisors. They appear to be pretty strong on the back office/administration side. They have to be and that is good. The reality is I’m not engaging in this type of service to help maintain a back office. I’m using a Robo Advisor to make money. This is where it all will shake down. In my next post, I will review the portfolio that was created for me.

Aman Raina, MBA is an Investment Coach and founder of Sage Investors, an independent practice specializing in investment coaching and portfolio analysis services.