Vanguard Investments Canada Inc. has announced the listing of three new low-cost Asset Allocation ETFs that give investors one-stop shopping to the firm’s globally diversified strategies. They began trading on the TSX today (February 1, 2018.)

Both investors and advisors are asking for “simple yet sophisticated single-ticket investment solutions that provide well-diversified global equity and bond exposure within a low-cost ETF structure,” says Atul Tiwari, managing director for Vanguard Canada. The new ETFs offer investors three different risk profiles and regular rebalancing.

In effect, each ETF is a fund of funds although Vanguard describes them as having an “ETF of ETFs structure.” Each holds seven existing core Vanguard index ETFs (which I list in the postscript below). Each new ETF of ETFs has a management Fee of 0.22%. Vanguard says that when one of its ETFs invests in underlying Vanguard funds, “there shall be no duplication of management fees.” Spokesman Matthew Gierasimczuk said “There are no duplicate fees beyond the 0.22 management fee, other than a basis point or two for operating expense and the trading fee for buying or selling the ETF.”

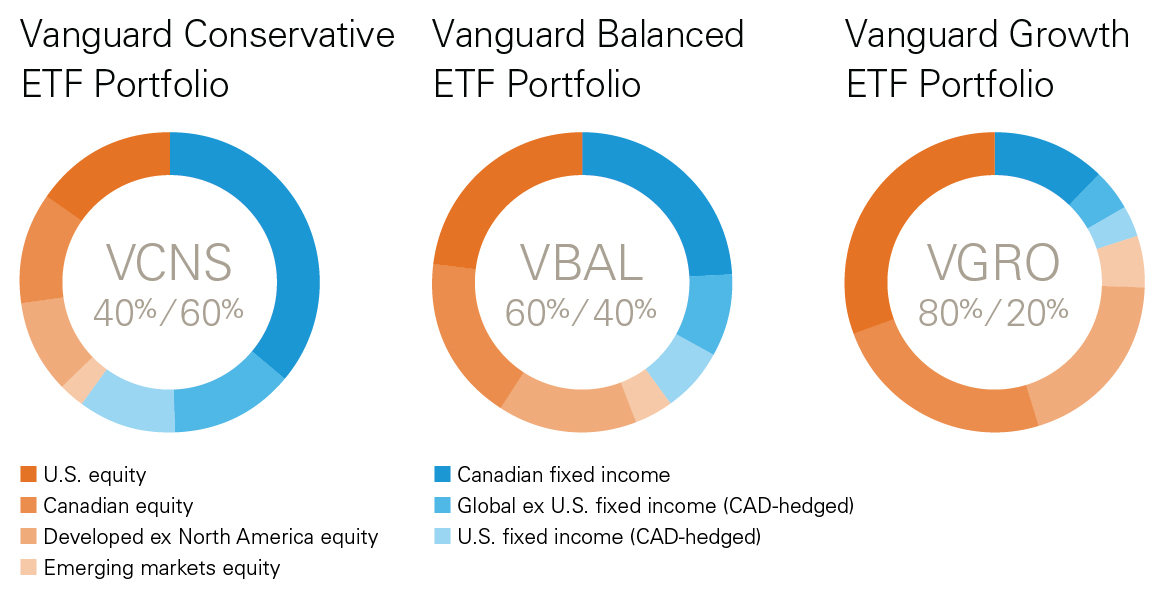

The three asset allocation ETFs cover the normal range from Conservative to Balanced to Growth, as reflected in the product names. Equity weights range from 40% for the Conservative offering, to 60% for the Balanced and 80% for the Growth.

Here are the 3 ETFs and their ticker symbols on the TSX:

Vanguard Conservative ETF Portfolio (VCNS) seeks to provide a combination of income and moderate long-term capital growth by investing in equity and fixed income securities with a strategic allocation of 40% equities and 60% fixed income.

Vanguard Balanced ETF Portfolio (VBAL) will provide long-term capital growth with a moderate level of income split 60% equities to 40% fixed income.

Vanguard Growth ETF Portfolio (VGRO) provides long-term capital growth by investing in equity and fixed income securities with 80% equities and 20% fixed income.

In a press release, Vanguard Canada head of product Tim Huver said the ETFs offer “a simplified and scalable solution for financial advisors, and a one-stop globally-diversified and transparent option for investors … Investors can rely on Vanguard’s global investment experts to continuously assess their portfolio’s exposure and rebalance it back to its intended risk level.”

With the three new ETFs, Vanguard Canada now offers 36 ETFs, with C$14 billion in assets under management. Vanguard Investments Canada Inc. is a wholly owned indirect subsidiary of The Vanguard Group, Inc.

You can find more at Vanguard Canada’s website.

Postscript: My Take

After sleeping on this announcement, it strikes me as more significant than I had initially perceived. In essence, the middle (Balanced) of the three Asset Allocation ETFs is the equivalent of the global balanced fund, which I’ve argued in the past should — in theory anyway — be the only investment fund you need. Similarly, while Vanguard’s ETFs are invariably components of the robo-adviser services out there (along with BlackRock iShares), any of these three new ETFs could serve as a one-size-fits all alternative to them. It also compares with Franklin Templeton’s Quotential.

The difference is that at 22 beeps and change, the three Vanguard products are quite a bit less costly: less than half the robo services at least, which typically come in at 50 beeps plus the underlying ETF fees. (NestWealth.com being a possible exception, since it uses a monthly subscription fee, making it cost-effective for high-net-worth investors).

I’ll be interested to hear what Boomer & Echo’s Robb Engen has to say about this, because in a popular 2015 post he famously described his dramatic personal shift from picking individual dividend-paying stocks to an all-ETF portfolio. You can find the republished Hub version here: Why Boomer & Echo’s Robb Engen dumped stocks to be 100% an indexer.

Certainly for do-it-yourself investors who no longer want to be constantly watching the markets and the disparate movements of individual stocks, any of these three new ETFs could be a good substitute and means for getting your life back. Younger people should pick the Growth version with 80% stocks, cautious mid-career people could favour the balanced 60/40% stocks version and older investors and retirees could choose the conservative version with only 40% stocks.

Since it’s arguable even retirees need that high a proportion of stocks to hedge against the possible future ravages of inflation, it too makes sense, although 40% stocks may be a tad high for older retirees. Alternatively, they could put half in the Conservative ETF and another half in ladders of two-year GICs, taking the combined equities down to a very conservative 20%.

It’s not clear to me whether fee-based advisors will flock to these products, although here too it would free them up to do true financial planning, deal with taxes, estate planning and other minutiae. The really good ones might well gravitate to it; the asset gatherers not so much.

Ideal for TFSAs

I also see this as a core holding in Tax-free Savings Accounts (TFSAs), since the $5,500 current annual contribution limit constitutes a relatively small “ticket” and these give you all the world and all asset classes in a single punch of the ticket. Check to see more about the seven underlying ETFs by clicking on the link below but the Growth version (VGRO) certainly has healthy exposure to both Canadian and global securities, both stocks and bonds.

According to the fact sheet you can get to by clicking on this link, it is 30.1% in the Vanguard U.S. Total Market Index ETF, 24% the Vanguard FTSE Canada All Cap Index ETF, 20% in the Vanguard FTSE Developed All Cap ex North America Index ETF, and 5.9% in the Vanguard FTSE Emerging Markets All Cap Index ETF. That’s exposure to the whole world’s stocks. The 20% fixed income comes from 11.7% in the Vanguard Canadian Aggregate Bond Index ETF, 4.7% in the Vanguard Global ex-US Aggregate Bond Index EFF (CAD Hedged), and 3.6% in the Vanguard U.S. Aggregate Bond Index ETF (CAD Hedged). All rebalanced regularly!

Because TFSAs can still be added to into advanced old age — my 101-year old friend Meta still contributes to hers! — I’d lean to going with the Growth or Balanced versions, and view the Conservative one as more appropriate for RRSPs and RRIFs, particularly the latter once forced annual minimum withdrawals commence (and therefore need to generate cash).

Finally, for couples where one spouse is the “finance” person and the other disinterested, this kind of product seems ideal for older do-it-yourself investors who are beginning to worry that dementia and related ills might impair their cognitive skills for investing.

In the case of a financially literate wife and a financially uninterested husband, if the wife were concerned about her dying first and wishing to put the collective portfolio on autopilot, the Balanced or Conservative version might also do the trick, short of just handing the whole lot over to a professional money manager.

A significant announcement indeed!

Great article on an extremely low-cost, globally diversified and auto-rebalanced portfolio that will potentially be a very viable option as a core holding for many investors. Thanks for this.

Great thoughts. Like the autopilot idea for the later years.

I’m not surprised this sort of thing is coming out, but, is the 0.22% fee high? I get the application, justification, etc, and it totally makes sense, except I can cobble together those at a much-reduced rate. Fees are the bane, so is this a concern? If fees for good ETFs are under 0.10%, this seems high. Thoughts?

I love this product from such a reputable firm. I totally see getting into this.

How tax efficient would the VGRO be in a non registered account?

Good question and one I will pose to Vanguard. My guess is that since it’s only 20% fixed income, fairly tax efficient but perhaps not as much as a pure Canadian dividend fund. Perhaps you’ve identified a future product need here.

Hi. Great article as always. Would it be possible to include the symbols for the component funds specifically in the VCNS ETF. Because VCNS will have no history for a year, it would be good diligence to see the history of the ETF’s that comprise it.

Enjoyed your Findependance book.

Hi Johnathan. No mention of the dividend rate. Assume it hasn’t been established yet?

Probably pretty tax efficient but no issue using this in a registered account (RRSP or TFSA). In a non-registered account, there are other options in building a tax-efficient portfolio. I like total return swap funds that follow the major indices, like those offered by Horizon (e.g. HSX for the S&P500). No tax implications until shares are sold, and then it’s at the lowest rate (capital gains).

Great that Vanguard is finally offering something akin to what has been around in the US and UK for a while with their Lifestrategy mutual funds. What I don’t get is why these ETFs were not structured as mutual funds like they’ve done in the US/UK.

Until all brokers finally abandon fees (and restrictions) to buy ETFs I can’t see the robo-advisor market being under threat as dripfeeding RRSP/TFSA is too expensive.

Good article and something to consider. Thanks Jonathan

Hello Jonathan,

Great article as usual. These are really very interesting ETF’s indeed.

My only question is how tax efficient these etf’s will be in a taxable account.

Hopefully we will get the answers….

Cheers

Frank

Working on it!

Thanks for the article–and I am drawn to the simplicity and no fuss re-balancing. But , regarding tax efficiency, I’m also interested to know how these funds are viewed when it comes to foreign withholding tax.

Great info as usual Jonathan. Thank you. I’m on the list for foreign withholding tax and bond inclusion info as well in non reg.

I’m 71, retired and not well at the moment. Traded down and have a good amount in residue for non reg investment. It will be legacy for kids and Gkids. This sounds like the answer to me. No rrsp or tfsa room.

Diversity, No muss no fuss and rebalancing with reasonable index returns. Best I’ve seen lately.

My wife has no interest in finances and would hand it off if I disappeared. :)

Cheers

Doc

Hey Jonathan were you able to find out how tax efficient these funds are going to be.

Not yet, so view as registered products primarily.

iShares offerings are at 0.18% hopefully vanguard counter