Want to pay less tax? The year-end brings with it your last chance for legitimate, allowable opportunities for tax planning that can lower your taxes payable to the Canada Revenue Agency (CRA) for 2016.

1.) Timing of Expenses

Taxpayers in business should accelerate expenses to make purchases that can be deducted this year rather than waiting for 2017. Employees can claim tax depreciation (CCA) on cars, planes, and musical instruments. Tradespersons and apprentices are permitted to deduct the cost of their tools up to a limit. Individuals planning on purchases should do so now to enjoy the benefit of depreciation claims this year.

Plan to purchase any capital property before the tax year-end to be able to claim CCA (at 50% of full rate) this year.

2.) RRSPs

RRSPs are a key tool for tax planning and allow Canadians to receive a deduction for the amount contributed, while also allowing the capital to accumulate tax-free until retirement.

Even though the deadline is March 1st, 2017, taxpayers should contribute to their RRSPs as soon as possible for compounded growth.

3.) Open TFSAs

While deposits to a Tax-free Savings Account (TFSA) are not tax deductible like RRSPs, accrued profits in the account are not subject to tax when earned or when withdrawn. Consider lending funds to a spouse or children to allow them to make their own TFSA contributions. Continue Reading…

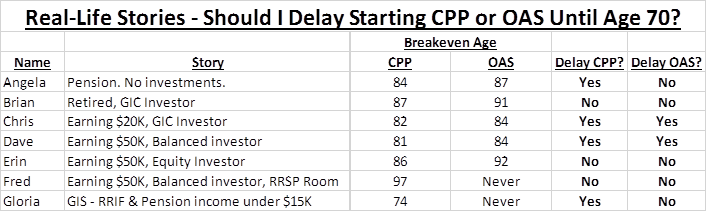

Here you will see that the single most important factor in deciding whether to delay CPP after age 65 is: Will you withdraw more from your investments if you delay starting?

A quick review of the facts:

Delayed CPP Rules

The maximum CPP benefit in 2016 at age 65 is $1,092.50 per month, or $13,110 per year.

You can delay starting up to age 70 and you get 8.4% more for every year after age 65. If you start at age 70, you get 42% more for life, so the maximum is $18,616 per year.

New rules in 2012 allow you to start CPP even if you are still working.

If you are over 65 and still working, you can choose whether or not to pay into CPP.

Your 8 lowest earning years since age 18 (plus years when you had kids under age 7) are “dropped out” in calculating how much CPP you get.

Delayed OAS Rules

The maximum OAS benefit in 2016 at age 65 is $578.53 per month, or $6,942 per year.

You can delay starting up to age 70 and you get 7.2% more for every year after age 65. If you start at age 70, you get 36% more for life, so the maximum is $9,442 per year.

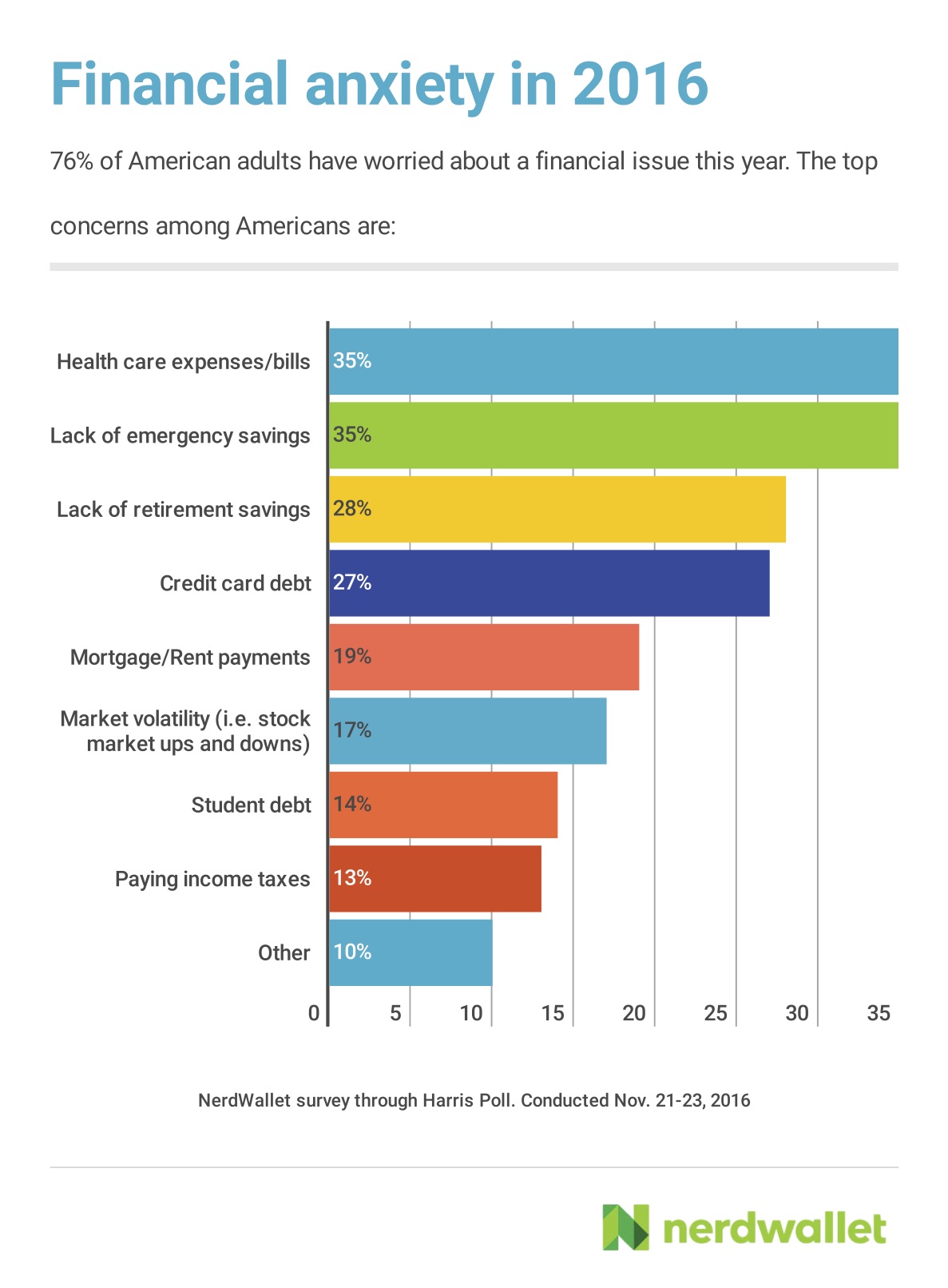

While 70% of Americans say they saved for retirement in 2016, many are anxious about the level of their savings and the need to direct money towards other goals and expenses, says a Harris Poll of 2,000 American adults conducted by the personal finance site NerdWallet. You can find the full results here.

Other major financial concerns include lack of emergency funds (cited by 35%), health care expenses (also 35%)and credit-card debt (27%). Retirement remains the most commonly cited savings priority (mentioned by 28% surveyed) but only 29% feel confident they saved enough in 2016, while one in three aren’t saving for retirement at all (including 43% of Millennials aged 18 to 24). Lesser forms of financial anxiety in 2016 include making mortgage or rent payments (19%), stock market volatility (17%), student debt (14%), and paying income taxes (13%).

Next year may not be much better: of those with workplace pensions, only 32% plan to increase their contributions in 2017. Older Americans aged 45 to 54 are most likely to report concern about lack of retirement savings (40% surveyed), while only 20% are confident they saved enough this year.

Savers should favour tax-advantage accounts over savings accounts

You can balance Health & Wealth with advisors on both

By Sandy Cardy

Special the Financial Independence Hub

The Holiday season is a very personal balancing act. Every year we experience the same thing – multiple events featuring gut-bloating menus and Boxing Day blow outs followed by crash dieting for both your waist-line and your bottom line. How do you find that sweet spot between making the season joyful and memorable while avoiding the perils of two to three weeks of over-eating and spending followed by a blizzard of credit card debt?

It’s no secret that Canadians, particularly Baby Boomers in their sixties, are doing a poor job of managing their retirement savings, falling well short of amassing enough retirement funds. Canadians still find it difficult to apply one of the simplest financial planning principles: pay yourself before you pay for anything else.

If, like many boomers, your retirement plan is increasingly looking like harnessing yourself to a full-time job as long as possible, what happens if you fall sick? And when you gaze with furrowed brow at your bloated credit card balances in January, not only are you even further from any savings goals, the sheer shock of the amount owing can add an unwelcome dollop of stress to already overtaxed minds and bodies. Never knowing when enough is enough, there aren’t any checks and balances on our impulse to over-consume.

Here are some tips to get re-balanced for 2017:

Every money decision you make, even the little ones, will have an impact on your retirement. Perhaps what you need now is a qualified advisor to help you achieve your goals: someone you trust wholeheartedly. A good advisor will ensure you are realizing all cost savings, and applying tax minimization strategies to build your net worth. Put it this way: it’s much more difficult to neglect simple investment principles when a financial planner is looking over your shoulder.

Healthcare advisors as important as financial advisors

Similarly, having one or more health care advisors available is essential. Whether you encounter a health crisis or want to pursue preventative health, it’s key to find nurturing and optimistic healers, either conventional or alternative, ones that involve you in your health care discussion.

“We’re on a bit of a crusade to change the way our society thinks about retirement.” — Jonathan Chevreau & Mike Drak

Mike Drak and Jonathan Chevreau, co-authors ofVictory Lap Retirement(published, October 2016) are not the first to head out on this crusade. Apart from the material on the larger subject of aging and longevity, in my library I must have at least 19 books, in addition to the stacks of reports, studies and new models on the subject of Retirement.

Over the twenty years in the career services industry, where I worked directly with business executives in their later life transitions – leaving the corporate crow’s nest, as I call it, I can appreciate where Mike and Jonathan are coming from in their take on this. I have produced three retirement programs since 2001, and in the process suffered from metaphor madness, developing novel ways of reframing the concept of retirement and our later life journey.

However, this Drak & Chevreau volume is a welcomed new addition to this crusade. The book, by way of its novelty, weaves the conversation from the threads of a concept called Findependence, as the cornerstone of aVictory Lap Retirement. So here we go. Rather than a traditional book review, here in this blog post, I present views of the authors as shared through interview questions with them in late October.

Authors Interview

Mark’s Q: Your co-authored book, early on, takes a shot across the bow at the “financial media & financial services industries” in the way they persist to push “Retirement” as if it were some final destination. (There seems little shift between the 1970’s London Life’s Freedom 55, to Prudential’s 2016 Race for Retirement campaigns for example.) What one new key message should marketers take from reading Victory Lap that could become a differentiator in their marketing?

Mike: The industry is using the same commercials that they used 40 years ago. The only difference is that they are now in color. The world of retirement has changed significantly over the years and most people cannot afford nor do they want to live the lifestyle portrayed in their commercials.

Banks assume more money equals better retirement, which is wrong thinking. Banks are good with the investment piece but they need to become more involved with the lifestyle piece. How can you ever know if you have enough if you do not have a firm handle on what type of retirement lifestyle you want in retirement and what that lifestyle will cost?

Mark’s Q: At one point in Chapter 3, you make the point that: “Compounding the problem is the lack of financial education our children receive in school.” You also say in Chapter 4 that the importance of financial independence is a prerequisite to the new stage of life you call “Victory Lap Retirement.” Let’s play here. What do you think about an opportunity for you to design/deliver a “Findependence” course relatable to high school teenagers that didn’t use the word Retirement? What then would the main message sound like to them?

By David Rotfleisch

By David Rotfleisch