“the financial press has gone on a feeding frenzy in response, serving up heaping helpings of negativity upon negativity.”

Everyone loves a Perma-Bear

Whether by traditional channels or social media streams, amplifying extreme news is in large part what the popular financial press does.

They’re not entirely to blame; we consumers tend to gobble it up with a spoon. That’s thanks to a behavioural bias known as loss aversion, which causes the average investor to dislike losing money approximately twice as much as they enjoy gaining it. Our “fight or flight” instincts basically prime us remain on constant high-alert when it comes to protecting our life’s savings.

Media outlets know that, and routinely round up a stable of talking heads to scratch that behavioural itch. Their “regulars” even earn catchy nicknames:

Perma-bear

Back in 2012, economist David Rosenberg put together a presentation called 51 Signs the Economy Is a Total Disaster. (What, only 51?) We know that reality begged to differ. He tried again in 2019, when he declared: “We’re going into a recession … I think it will be this coming year.” It didn’t happen.

Dr. Doom

Whenever the press needs a fresh Armageddon forecast, they know they can call on “Dr. Doom” economist Nouriel Roubini. It doesn’t seem to matter that he’s been mostly wrong far more often than not. As recently as early July, Roubini was predicting a 50% freefall in the stock market. So far, not so much (thankfully).

“The tweets that get shared and liked the most are the ones that fit with how we feel the most … Twitter is an enormous mirror.”

If you look closer, you might spot a card hiding up these soothsayers’ sleeves: with a large, random group of “experts” loudly predicting doom and gloom nearly all the time, basic statistics informs us: a few of them are going to be right every so often, with seemingly uncanny accuracy. Their fortuitous timing makes them look super smart, which earns them even more fame. The cycle continues.

Going on a Financial Media Diet

On many fronts, times are indeed disheartening, and we’re as worn out as you are by the weight of the world. That said, there are already way too many outlets cramming worst-case scenarios down our throats and crushing investment resolve. To offset a bitter pill overdose, following are a few more nutritious news sources to reinforce why we remain confident that capital markets will continue to prevail over time, and that long-term investors should just stick to their plan.

Stock Markets Grow

The following chart is one of our favorites, as it shows at a glance that which the bad news bears routinely disregard: Stock markets have gone up nicely, and far more frequently than they’ve gone down. We have no reason to believe current trends are going to alter this uplifting, nearly century-long reality.¹ Continue Reading…

Thinking about buying a home? As of late 2021, there were 646,053 active home listings, according to Rocket Mortgage. More homes are likely to come on the market in spring and summer, which are hot selling seasons. Investing in a home purchase can afford buyers an asset that, ideally, should maintain or, hopefully, increase in value. Some buyers simply want a place to hang their hat and call their own. Whether you’re raising a family, need space for your dogs, or are ready to tackle the responsibilities of maintaining a house, you can rely on this guide to provide you with the essential information you need to know before you buy one.

Are you ready to buy a House?

Buying a house is a big commitment — living in a specific location, paying a mortgage for decades, and maintaining a property (in order to preserve its value). Many people either aren’t ready to settle down into a home of their own or simply prefer to rent, leaving property maintenance to property owners. You’re likely ready to buy if you:

Are annoyed or tired of renting: typically, renting involves loads of rules stipulated by landlords, annual rent increases, and a lack of privacy (mainly if you live in an apartment complex).

Want to invest in real estate: investing in real estate is a common reason why people buy houses. Unlike rent, which is gone once you pay it, your mortgage payments are applied to the home’s purchase. In typical cases, you’ll retain that money in the form of your asset or recoup it when you sell the house.

Have a family and want more room: if you have a family, you may wish to purchase a home that offers space for each member of your household as well as a backyard that provides outdoor living space.

Pre-purchase Considerations

Before buying a house, there are various factors to consider before you sign on the dotted line of a purchase contract. A home tends to be a long-term investment. To make the most of it, it’s essential to understand the challenges associated with the buying process and the obligations related to property ownership. By exploring the personal and financial areas of your life, you can arrive at the right decision for you.

Personal Considerations

Ask yourself if you are ready to commit to living in a specific area. A mortgage is generally a 30-year commitment (unless you choose to sell the property). What are your plans for the future? Do you expect to relocate soon for your job? Do you wish to have children or to expand your family? These considerations may impact your decision to buy as well as the type of home to buy.

Remember, everything regarding the care of the home will rest on you: and your partner if you are purchasing together. Not only is there the monthly mortgage to cover, but there are also the inevitable home maintenance and repair costs that come into the bargain. In short, understand the financial obligation before you as you contemplate your decision.

Financial Considerations

There are other financial factors to reflect upon too. To qualify for a mortgage, you will need a good credit score as well as a down payment. As banks consider your loan request, they will examine your debt. Do you have existing debt, and is it enough to impede your home buying plan? Also, banks will evaluate whether your income is enough to pay the monthly mortgage payment. Look closely at your financial picture because, rest assured, any lender you choose will definitely examine your finances closely.

The Psychology of Buying a Home

You might not realize it, but engaging in the home buying process can be an emotional roller coaster. It’s easy to get your hopes up that a seller will accept your bid. You might fall in love with the perfect house only to realize that the seller accepted another buyer’s bid. You might also find a home with great potential only to find that it has severe flaws like a cracked foundation. It’s important to keep your emotions in check to make a sound investment decision.

There are other psychological aspects of buying a house that you might not have thought about before. For instance, some people bring cultural superstitions to the process and don’t want to live in a house with specific numbers in the address or are opposed to a particular street name.

Other people might struggle with the perceived value of a home, believing that interior wall colors will substantially affect its worth. The reality is that cosmetic changes are easy and often inexpensive to fix in cases like this.

If you find yourself contending with psychological factors like these, take a step back and think them through. If they’re going to impede your long-time enjoyment of the home, you may want to keep house hunting. If, however, you think you can spend a decade of your life on “Elm Street,” you may be glad that you didn’t allow a horror movie from the 1980s to sabotage the purchase of your dream home.

Searching for a Home

Speaking of needs, you’ll need to consider them closely so that you can confine your search to homes that satisfy them. Before you begin your house hunting adventure, you should consider:

House size: how much square footage will suit you/your household?

House exterior: what architectural styles appeal to you? Bungalow, cape cod, modern?

Bedrooms: what’s the minimum number of bedrooms you need?

Bathrooms: how many bathrooms do you prefer your home to have?

Heating and cooling systems: how efficient are these systems? Will they need to be replaced soon after you buy the house?

Basement: do you want a home with a basement or cellar?

Attic: do you want to purchase a home with a finished attic that offers usable living space?

Garage: how much space do you want your garage to have?

How to Choose the Right Neighborhood

The neighborhood of your home is also an important consideration. A great home in a community that you don’t find agreeable can make for an unhappy situation. When you choose a neighborhood to shop for a home, you should consider:

Safety: investigate the area’s crime rates, affecting property values.

Community services: do you require public transportation? Do you want to live near shopping centers, medical facilities, or parks?

Public schools: be sure to assess the quality of area schools if you have school-age children.

Amenities: what are some local amenities in the area? Is there a local swimming pool, forest preserves, entertainment venues like theaters? What about restaurants?

Top Home Buying mistakes

Many buyers have stumbled into pitfalls when shopping for and buying a house. Try to learn from their mistakes. Here are some of the most common home-buying mistakes to watch out for:

Partnering with a real estate agent who doesn’t “get” your needs and preferences.

Failing to get pre-approved for a mortgage.

Making an offer on the first house you visit.

Getting only one rate quote from one lender instead of shopping for a more competitive lender.

Buying a house that is more than you can afford.

Using all of your savings as a down payment.

Not investigating the HOA if the area has one.

Failing to look into first-time homebuyer programs.

Not researching the community extensively.

Waiving a home inspection.

Special terms for New Home buyers

Is this your first time buying a house? In that case, you’ll undoubtedly want to find out about first-time homebuyer programs and special incentives that can alleviate some of the financial stress associated with buying a home. You may also qualify for programs based on your income or veteran status. An experienced real estate agent will be able to inform you about any programs or incentives that you might qualify for. As a first-time homebuyer, some of the special terms you may be eligible for include: Continue Reading…

By Bilal Hasanjee, Senior Investment Strategist, Vanguard Canada

Special to the Financial Independence Hub

In the current record-breaking inflation and rising interest rate environment across all major markets, stocks and bonds have declined in values simultaneously.

As a result, many analysts and commentators have speculated on the death of the 60% stock/40% bond portfolios. But we have seen this before. Based on Vanguard’s research, balanced portfolios have proved critics wrong before and we believe they will prove them wrong, again. Here are five reasons why a 60% stock/40% bond portfolio is NOT dead.

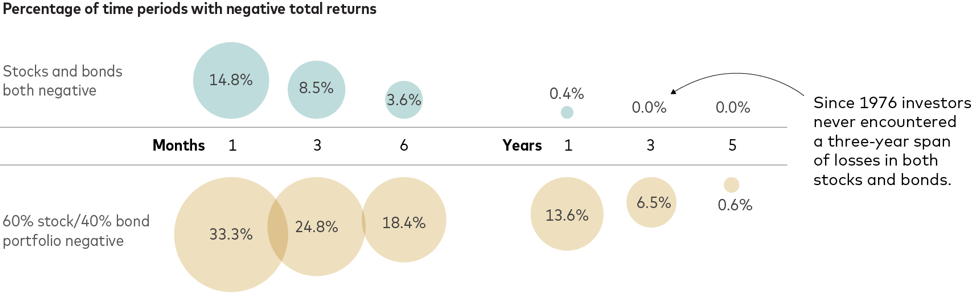

Reason 1: Stock-bonds simultaneous decline is not long lasting

A simultaneous decline or positive correlation in stocks and bonds has typically not lasted long and the phenomenon has never occurred over a three-year span. A similar trend is visible on a 60/40 (stocks/bonds) portfolio.

Drawdowns in 60/40 portfolios have occurred more regularly than simultaneous declines in stocks and bonds; however, their frequency of occurrence also declines over longer periods. More regular occurrence is due to the far-higher volatility of stocks and their greater weight in that asset mix. One-month total returns were negative one-third of the time over the last 46 years. The one-year returns of such portfolios were negative about 14% of the time, or once every seven years or so, on average.

Figure 1

Source: Vanguard

Data reflect rolling period total returns for the periods shown and are based on underlying monthly total returns for the period from February 1976 through April 2022. The S&P 500 Index and the Bloomberg US Aggregate Bond Index were used as proxies for stocks and bonds.

Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

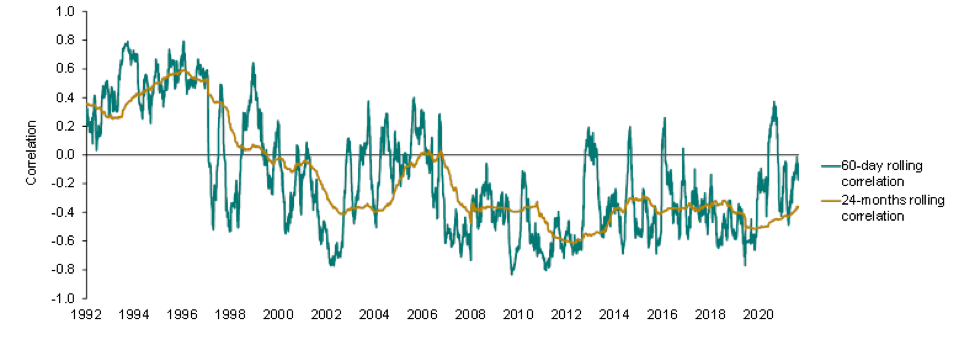

Stock-Bonds correlation remains negative in the long term

Our study of 60-day and 24-month stock-bonds rolling correlations from 1992 to 2022 suggests that over a long-term, correlation between stocks and bonds remains negative. That said, long-term inflation is one of the determinants of correlation between the two asset classes

Figure 2: Long-term correlations expected to remain negative

Notes: Rolling correlations are calculated on total returns of the S&P 500 Index and the S&P U.S. Treasury Bond Current 10-year Index, using daily return data for the period between 1989 and May 31, 2022.

Sources: Vanguard, using data from Refinitiv, as of May 31, 2022. Past performance is no guarantee of future returns.

The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Reason 2: Long-term expected returns from 60/40 are still achievable

The goal of a 60/40 portfolio is to achieve long-term annualized returns of roughly 7%. This is meant to be achieved over time and on average, and not every year. The annualized return of 60% U.S. stock and 40% U.S. bond portfolio from January 1, 1926, through December 31, 2021, was 8.8%.1 On a forward-looking basis, Vanguard Capital Markets Model (VCMM) projects the long-term average return to be around 7% for the 60/40 portfolio, over the next 10 years. Market volatility means diversified portfolio returns will always remain uneven, comprising periods of higher or lower: and, yes, even negative returns.

The average return we expect can still be achieved if periods of negative returns (like this year) follow periods of high returns. During the three previous years (2019–2021), a 60/40 portfolio delivered an annualized 14.3% return, so losses of up to –12% for all of 2022 would just bring the four-year annualized return to 7%, back in line with historical norms.

Our forecast points to improved stocks and bond returns

On the flip side, the math of average returns suggests that periods of negative returns must be followed by years with higher-than-average returns. Indeed, with the painful market adjustments year-to-date, the return outlook for the 60/40 portfolio has improved, not declined. Driven by lower equity valuations and higher bond yields, our 10-year annualized average return outlook for the 60/40 is now higher by 1.3 percentage points than before the recent market adjustment.

Reason 3: Selling bonds in a rising rate environment is like selling low and buying high (in short, don’t try to time the market)

Chasing performance and reacting to headlines are doomed to fail as a timing strategy every time, since it amounts to buying high and selling low. Far from abandoning balanced portfolios, investors should keep their investment programs on track, adding to them in a disciplined way over time. Continue Reading…

A look at the “Top Dividend” stock list on the TMX website will show an investor a selection of the highest yielding investment funds and stocks available in Canada. That list features some astronomically high numbers on investment funds: yields upwards of 20%. An income-seeking investor might look at those numbers and rush to buy, believing that with a 20%+ yield, their income needs are about to be met.

As attractive as the highest-yielding investments might appear, there are a wide range of other factors for investors to consider when shopping for an income paying investment fund. Investors may want to consider the crucial details of how, when and why that yield is paid as income: as well as their own risk tolerances and investment goals. This article will outline how an investor can assess those factors when deciding what income investment fund is right for them.

Looking ‘under the hood’ of the highest-yielding investment funds

If you see a big yield sticker on an investment fund in excess of 20%, you may want to look more closely at the details of its income payments.

Because income from investment funds is not always solely derived from dividends, the income characteristics will be listed under the term “distributions.” Information like the distribution frequency and the distribution history will tell a prospective investor a great deal about a particular investment fund’s high yield.

Investment funds will pay their distributions monthly, quarterly, or annually. By looking at the distribution frequency of an investment fund, investors can assess whether an investment fund meets their particular cashflow needs.

A useful way to assess the track record of an investment fund is by looking at the distribution history page published on its website. This will show how much income was paid on each distribution. Some funds have very consistent distributions history, while others fluctuate frequently over time. The distributions history can be a useful way to assess the reliability of the income paid by an investment fund.

Assessing these characteristics can be a useful first step in deciding whether an income investment is right for you. But investors should also consider why the yield number next to an ETF is so high.

Is the high-yield number temporary?

The yield numbers next to investment funds on a resource like the TMX “Top Dividend” list reflect the most recent distribution paid by an investment fund or stock. In the case of investment funds, that distribution could have been a one-off ‘special distribution.’

A special distribution could be the result of a wide range of factors. For example, one of the fund’s holdings could have paid a significant dividend that is being passed on to unitholders. Special distributions are often accompanied by a press release. Continue Reading…

In August of 2020 we asked if Canada’s energy dividends were in trouble? Of course that was before energy prices and energy stocks were dominating the headlines. At the time Canadian oil prices were about $30 a barrel and energy dividends were under a lot of pressure due to collapsed earnings.

Today, that price has more than tripled and has been above $100 and now sits near $92 (May 2022). You’ll notice when you compare the Western Canadian Select price to Brent (closer to $105) just how much Canada’s energy dividends and earnings would benefit from not having to discount relative to world price! That said, that gap in price has been closing. And the generous oil prices have fuelled incredible earnings and dividend growth.

source: https://oilprice.com/oil-price-charts/

Those higher oil prices are wonderful for Canadian oil producers, mostly operating or active in the Canadian oil sands, but many of the producers also have global operations. They have already become free cash flow gushers. More investors, fund managers and retail investors are going along for the ride.

Over the last year, the returns for the TSX Capped Energy Index are more than 90%. If we go back to the start date of this Canadian energy stock series (August 2020) the energy index is up over 300%.

On my site, I had suggested last October that investors consider Canadian oil producers.

I offered …

“The Canadian energy sector has been beaten up. Foreign investors have given up and so have many Canadian investors. Where there is incredible pessimism there can be incredible rewards. But there is certainly no guarantee that the pessimism for the Canadian energy patch is not deserved.

That said, it is also certainly possible that the pessimism has jumped the shark. There may be incredible value in the energy sector for Canadian investors.”

Canadian investors who went against the flow were rewarded handsomely, and it was not as big a risk as many would think. The macroeconomic and energy-specific story was quite simple.

Economic activity and energy usage was certain to pick up as we made our way through the pandemic. Canadian energy producers were made more lean and mean by the tough years in the energy patch. They had already spent the required amounts (CAPEX investments) to make their oil projects viable and profitable at lower oil prices. If prices do get to $50 a barrel and more, they have a license to print money.

As you can tell from the chart above, if you’re a risk averse dividend investor, Canada’s pipeline’s are a much more stable bet (although potentially with much less of an upside) over the medium- and long-term.

Mike Heroux – the man behind DSR – is a CFA and has been studying Canada’s dividend players for several decades. His free webinars on the value of the mid-stream pipeline companies (they’re not building any more of them) versus the mercurial nature of the oil companies themselves really makes sense. You can read our full Dividend Stock Rocks review here.

Visit DSR Now & Get Our Exclusive Discount

The Long-term Strength of Energy Stock Dividends

The story on energy stocks has evolved, in that our green desires do not match the energy reality. Today there are reasonable fears of an energy crunch that could turn into an energy crisis. The renewable energy transition will take a decade or two.

In the meantime we have increasing demand for oil and gas and greatly decreased CAPEX: there’s little desire to look for more oil and gas. In fact, it’s politically unfashionable to suggest that we need more oil and gas, or to spend the time and money necessary to find and produce more oil and gas.

That sets up a secular and positive trend for traditional oil and gas. It is an unfortunate reality.

The story goes back to the most basic economic principle: supply and demand.

On the bullish side, Eric Nuttall, portfolio manager at NinePoint Partners, suggests it is a generational investment opportunity. Eric often reminds us that the free cash flow that many of these companies produce is beyond generous, it is ridiculous. They can quickly pay down debt, buy back shares and return more value to shareholders by way of generous dividend increases.

The Big Oil Stocks Idea

Looking at returns for Canada’s “Big 3” oil stocks over the last year have been eye-opening.

Here is the portfolio income chart from that post, with a hypothetical starting amount of $10,000. It is an equal weight portfolio of The Big 3. We see that there was no oil drought, no oil recession for the investor that went ‘big’ with their Canadian energy stock selection.

Source: Portfolio Visualizer

The big oil stock consideration was and is Canadian Natural Resources (CNQ), Suncor (SU) and Imperial Oil (IMO). In Million Dollar Journey’s post on the top Canadian Dividend Growth Stocks you’ll find ‘The Big 3’.

In August of 2020 I noted that the dividends had held up reasonably well.

Canadian Natural Resources (CNQ) had maintained its dividend and offered a yield of almost 6.3%.

Imperial Oil (IMO) has maintained its dividend and at the time delivered a yield of almost 3.8%.

After a dividend cut of 55% Suncor (SU) was down to a yield of 3.7%.

But the free cash flow is now feeding sweet dividend increases, or should we say dividend gushers.

In April of 2021 CNQ increased its dividend by 10.6%, followed by 25% and 27.7% increases

In July of 2021 IMO increased its dividend by 22.7% followed by a 25.9% increase

In December of 2021 SU increased its dividend by 100% (in June of 2022 they gave it another 11.90% boost.

The Canadian Energy Stocks Dividend Growth Scorecard

From the time of the first energy stock article on MDJ.

CNQ, 0.425 to 0.75 an increase of 76.5%

SU, 0.21 to 0.47 an increase of 123%

IMO, 0.22 to 0.34 an increase of 54.5%

The Big 3 offered an average of 84.7% dividend growth over less than a 2-year period.

I had suggested that the oil and gas sector has the potential to be the greatest source of dividend growth within the Canadian market. That is playing out in spades. Of course Canadian investors were also keeping an eye on Canadian bank stocks.

Regulators had forced the banks to suspend dividend increases and share buybacks during the pandemic. Those restrictions were removed, and we were treated to double digit dividend growth for Canadian banks and financials.

We expect more dividend growth announcements this month.

What if you had Investedin the Big 3 Oil Stocks?

From that time of that post you would have seen some generous and growing income. That said, you would also have total returns that would have almost tripled the total returns compared to the TSX Composite.

Source: Portfolio Visualizer

You’ll also see the pipelines in there. Those are my two pipe holdings, Enbridge (ENB) and TC Energy (TRP). You’ll find those companies in the portfolio that focuses on Canadian Wide Moat Stocks and are stellar Canadian dividend all stars.

They matched the returns of the market for the period. They have been offering a wonderful inflation hedge as well. While the pipes don’t have the torque of the energy producers, they have delivered returns of over 16% in 2022, to the end of April.

Source: Portfolio Visualizer

Back in 2020, I had suggested that I would stick with being a toll taker, collecting tolls and dividends by way of those pipelines that move the oil and gas around North America. Of course, Enbridge and TC Energy are much more diversified and do have energy producing operations as well. Continue Reading…