By Bob Lai, Tawcan

By Bob Lai, Tawcan

Special to the Financial Independence Hub

It is always great to see innovation and new products in the banking and investing industry. A few months ago, CIBC introduced the Canadian Depositary Receipts (CDRs) on the NEO Exchange as a way to provide Canadian investors with yet another option for investing in non-Canadian companies.

Canadian Depositary Receipts, or CDRs, may not be a familiar name for many readers. However, some readers may be aware of American Depositary Receipts, or ADRs. ADRs have been trading in the US for many years as a way for investors to buy shares of companies that are listed outside of the US. For example, we own Unilever PLC via the Unilever ADR listed on NYSE. In case you’re wondering, there are many ADRs available on the NYSE.

With CDRs becoming increasingly more popular, a few readers have emailed me about whether it makes sense to invest in CDRs instead of directly trading US stocks.

What are Canadian Depositary Receipts (CDRs) and what are the benefits?

Canadian Depositary Receipts are created to allow Canadian investors to buy US stocks in Canadian dollars. For now, CDRs represent shares of US companies but are traded on the NEO Exchange. Since CDRs are traded on a stock exchange, you can view them like traditional stocks. Owning CDRs means you would receive dividends (if the company pays dividends) and have voting rights to the underlying company you’re holding.

What makes CDRs very attractive is the fact that you can buy them in Canadian dollars. You no longer need to convert CAD to USD and pay the extra currency conversion costs or perform Norbert’s Gambit. By buying CDRs in Canadian dollars, it is more cost effective. In addition, there are no management fees associated with CDRs.

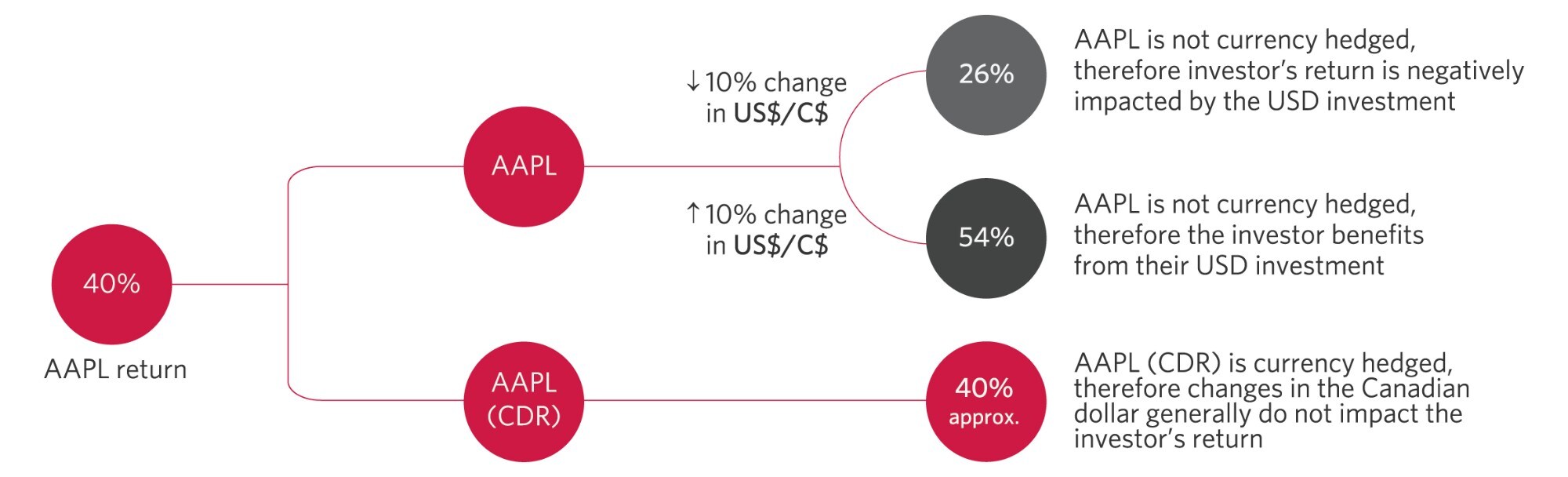

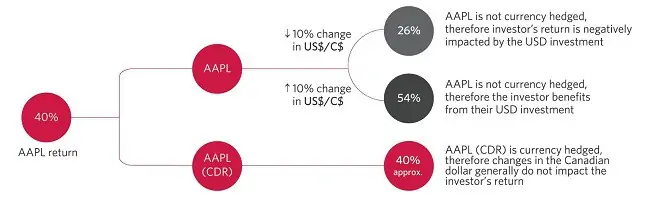

There is a built-in currency hedge in CDRs which eliminates the impact of exchange rate fluctuations over time. Therefore, in theory, the returns of the CDRs are tied directly to the performance of the underlying stocks and you do not have to worry about currency fluctuations.

Since the initial price for each CDR is around $20, CDRs allow Canadian investors to own fractional shares of the underlying stocks at a much lower cost. Essentially, CDRs utilize a ratio called the CDR ratio to represent the number of shares of the underlying stock. The CDR ratio is adjusted automatically daily to account for the currency hedge. If the Canadian dollar increases in value compared to the US dollar, the CDR ratio is adjusted to represent a larger number of underlying shares. The reverse is done when the Canadian dollar weakens.

In other words, rather than buying one share of Amazon at around $3,500 USD or $4,500 CAD, you can hold a few shares of Amazon CDR at around $20 per share at a much lower overall cost. You would still get all the equivalent benefits as a regular Amazon shareholder.

What stocks are available as Canadian Depositary Receipts?

When CDRs were launched in July 2021, CIBC had only a handful of CDR stocks available to trade. Since then, CIBC has added more and more CDR stocks. At the time of writing, there are 18 CDRs available on NEO Exchange:

| Symbol | Name | Price | Trades | Volume |

| AMZN | AMAZON.COM CDR | 21.5 | 352 | 53,220 |

| GOOG | ALPHABET INC. CDR | 25.05 | 382 | 73,588 |

| TSLA | TESLA, INC. CDR | 32.66 | 1,779 | 207,169 |

| AAPL | APPLE CDR | 25.34 | 342 | 56,092 |

| NFLX | NETFLIX CDR | 25.11 | 125 | 10,358 |

| MVRS | META CDR | 18.68 | 181 | 8,509 |

| MSFT | MICROSOFT CDR | 24.94 | 437 | 64,181 |

| PYPL | PAYPAL CDR | 14.6 | 348 | 44,410 |

| VISA | VISA CDR | 20.13 | 292 | 33,288 |

| DIS | WALT DISNEY CDR | 18.32 | 339 | 24,460 |

| AMD | ADVANCED MICRO DEVICES CDR | 28.21 | 197 | 9,498 |

| BRK | BERKSHIRE HATHAWAY CDR | 22.1 | 147 | 25,926 |

| COST | COSTCO CDR | 25.67 | 155 | 8,254 |

| IBM | IBM CDR | 19.24 | 31 | 4,391 |

| JPM | JPMORGAN CDR | 22.48 | 25 | 1,143 |

| MA | MASTERCARD CDR | 21.97 | 111 | 14,719 |

| PFE | PFIZER CDR | 24.79 | 147 | 6,796 |

| CRM | SALESFORCE.COM CDR |

As you can see, there are some really big name, very popular stocks like Apple, Tesla, Alphabet, Netflix, Meta, and Berkshire Hathaway available as CDRs. I am virtually certain that CIBC will add more CDRs on NEO Exchange going forward.

Where can I buy Canadian Depositary Receipts?

Since CDRs are traded like normal stocks on the Canadian stock exchange, you can purchase these CDRs through any online discount broker, such as TD Direct Investing, Questrade, and National Bank Direct Brokerage. You can also trade CDRs on WealthSimple Trade.

Because these CDRs have the same symbols as the US equivalent, you need to pay extra attention to make sure you select the correct stock symbol when purchasing. For example, when you search Apple on WealthSimple Trade, Apple listed on NASDAQ and Apple CDR listed to NEO Exchange both will show up. If you do not pay attention, it is easy to select the Apple listed on NASDAQ and put in a buy order.

It would be a shame to end up buying US listed shares and incur currency exchange fees when that was the very opposite of what you intended to do.

Should you invest in CDRs?

It is always positive to have options, so I think overall CDRs are great for Canadian investors. Should you invest in CDRs? Well, that depends on your situation and preference. Continue Reading…