It would be much easier to plan for the future if we knew what stock prices were going to do. Bank of America has a chart with seemingly solid evidence that stocks will lose a total of about 8% over the next 10 years. I’m going to show why this evidence is nonsense. But don’t worry; I’ll do it without making you try to remember any of your high school math.

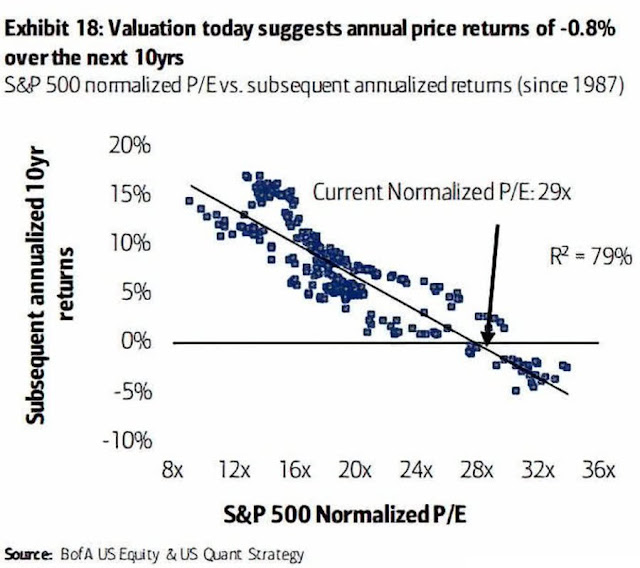

The Bank of America chart [shown on the left] looks intimidating to non-specialists, but I’ll summarize the relevant parts in easy-to-understand language. The basic idea is that for each month since 1987, they looked at how expensive stocks were that month and compared that to stock market returns over the 10 years following that month. They found that the more expensive stocks were, the lower the next decade of returns tended to be. The hope is that we can just use the chart to look up today’s stock prices to see what stock returns we’ll get over the next 10 years.

In the chart, each dot represents one month from 1987 to 2010. Notice that the dots are fairly close to forming a straight line. Statisticians get excited when they see a strong relationship like this. If the line were perfectly straight, we could just look up how pricey today’s stocks are (using a measure called the P/E or price-to-earnings ratio), and read off the average annual stock return we’ll get over the next 10 years.

The line isn’t perfectly straight, but it’s fairly close. One measure of how close to a straight line we have is called R-squared. For our purposes here, we don’t need to know much about R-squared other than 100% means a straight line, and as this percentage drops toward zero, the cloud of dots spreads out. The chart indicates an R-squared of 79%, which is a strong relationship.

Also indicated on the chart is the prediction that stocks will lose an average of about 0.8% each year over the next decade. However, if we imagine an oval surrounding the full range of dots, this chart predicts annual stock returns between about -3% and +2%. If we knew future stock returns really would fall in this range, most people would sell their stocks. But can we count on stock returns falling in this range? It turns out that we can’t because the chart is deeply flawed, as I’ll explain below.

Problems

The first thing to observe is that this chart is based on about 34 years of stock market data, a little over 3 decades. Because we’re talking about 10-years returns, you might wonder why there are more than 3 dots on the chart. The answer is that it uses overlapping periods. There is a dot for January 1987, then February 1987, and so on.

Consider the ten years of returns starting in January 1987 and compare this to the ten years of returns starting in February 1987. They are the same in 119 of 120 months. Each decade of returns starting monthly from 1987 to 2010 overlaps with 119 other decades. There is a huge amount of redundancy in the chart. Somehow we went from a 3-dot chart to one with hundreds of dots.

Using overlapping data isn’t always a bad thing, but it is in this case because there is just too little independent data to have any statistical significance. To show this, I ran some simulations. I created random stock market data and measured R-squared values.

The method I used for creating this simulated stock market data created returns that ignored stock valuations. This means that using P/E values to predict stock market returns is futile with this simulated data; the R-squared value of the underlying probability distribution used in the simulations is zero. To confirm this, I generated a million years of stock market data, and measured the R-squared value. In a thousand repetitions of this experiment, all R-squared values were less than 0.02%.

However, coincidences are common when you examine very small amounts of data. I ran simulations of 34 years of stock market data. I repeated this experiment 100 million times. Amazingly, in just over one-tenth of the simulations the R-squared value was above 79%, and in 51% of the simulations the R-squared was above 50%. These seemingly strong correlations are what you get with small amounts of random data, even though the underlying probability distribution has no correlation at all (R-squared equal to zero).

What can we conclude from these experiments? Continue Reading…