By Nick Barisheff

By Nick Barisheff

Special to the Financial Independence Hub

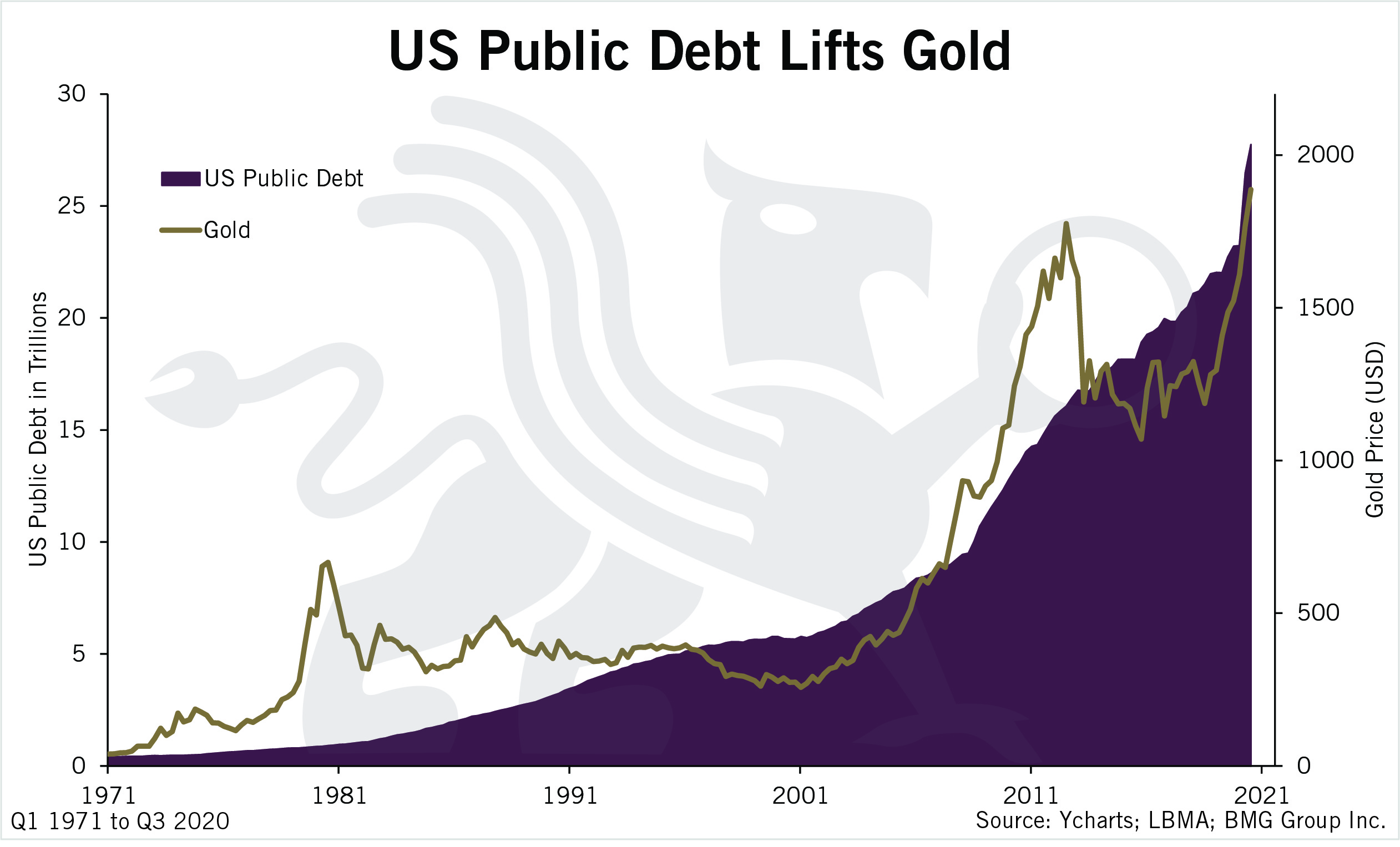

The world is awash in debt, an immense, unfathomable ocean of financial obligations. The stack of IOUs is so enormous, the balances so large, they will never be fully settled without dreadful consequences to the global economy. This tsunami of debt was unleashed in 1971, when Nixon ended the backing of the US dollar with gold.

Since 1971, US debt and gold prices have increased greatly. Traditionally, rampant increases in US debt occur when trying to pull the economy out of an economic downturn as displayed in the spikes that occurred in 2008 and 2020.

Considering the amount of debt that has already been taken on to combat the pandemic — combined with the rising uncertainty involving vaccinations and new strain variants — it can be anticipated that the worst is yet to come. As Democrats push towards passing an additional US$1.9 trillion stimulus package, governments are willing to take on previously unforeseen levels of debt to prop up the economy during the pandemic. This could lead to a promising future for the price of gold.

Manipulation of Precious Metals markets

This divergence has been caused by manipulation of precious metals. A great deal has been written about this and one of the best books on the subject is Rigged – Exposing the Largest Financial Fraud in History, by Stuart Englert.

Price manipulation never lasts, and when it ends there always tends to be a reset to inflation-adjusted levels. The biggest questions are: when and how high will gold and silver prices rise?

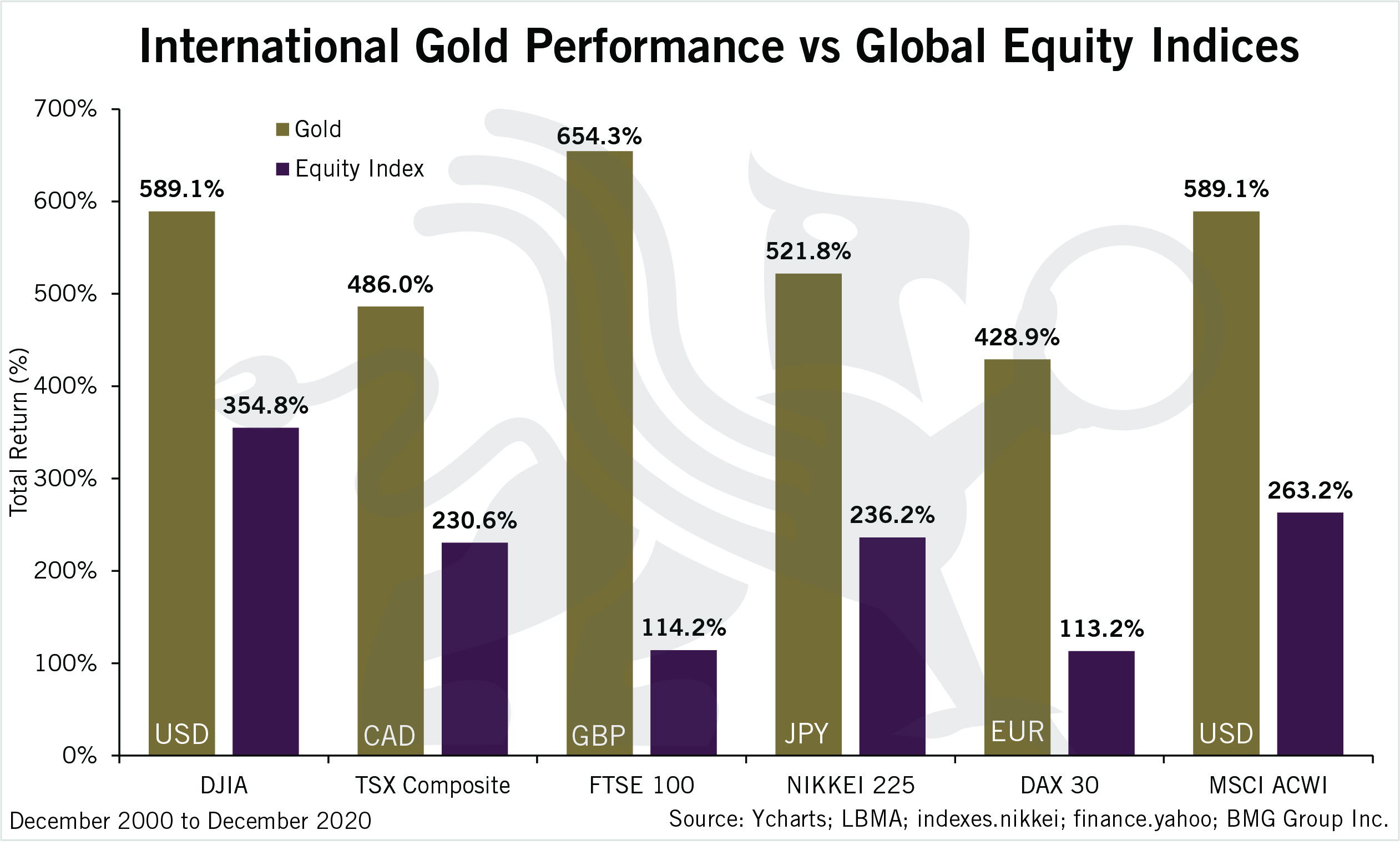

However, even with manipulated markets precious metals have outperformed traditional financial markets and have generated over 10% returns in all currencies over the last 20 years.

How soon precious metals rise to normalized levels depends on how rapidly governments and central banks inundate the world with debased dollars and other fiat currencies, and how quickly individuals and institutions lose faith in those increasingly worthless debt-based currencies.

How soon precious metals rise to normalized levels depends on how rapidly governments and central banks inundate the world with debased dollars and other fiat currencies, and how quickly individuals and institutions lose faith in those increasingly worthless debt-based currencies.

The US national debt alone is nearly US$28 trillion. This doesn’t include the $159 trillion of unfunded liabilities, which brings the total to US$187 trillion or about US$480,000 per American citizen. This number also doesn’t include the $21 trillion in unaccounted federal expenditures discovered by Prof. Mark Skidmore and his economic students at Michigan State University.

Global debt hits 365% of World GDP

Global debt hit $277 trillion last year, or 365% of world gross domestic product (GDP). Public debt as a percentage of GDP has soared to unsustainable and perilous levels. The US debt-to-GDP ratio hit 136% last year. Canada’s debt-to-GDP ratio increased by nearly 80% through the third quarter of 2020, the highest rate among developed nations.

When you translate these incomprehensible and burgeoning debt totals into per capita obligations, it is obvious that they will never be repaid. They can only be inflated away.

Combined with hundreds of trillions in unfunded government liabilities, swelling debt and unregulated financial derivatives form a bottomless abyss that eventually will engulf nations and swamp the entire financial system. Little wonder that in 2002, billionaire investor Warren Buffett dubbed derivatives — which essentially are debt instruments used as collateral to take on more debt — “financial weapons of mass destruction.” At that time derivatives totaled $100 trillion, whereas today they are in excess of $1 quadrillion.

Socialists maintain public debt is acceptable when borrowing is for the common good, and Modern Monetary Theory (MMT) advocates claim unlimited government spending is not a problem. They believe governments can create an infinite amount of currency to fund social services and public works projects. They fail to recognize that debt is not wealth and increasing the currency supply decreases its value and produces price inflation.