By Mark Seed, MyOwnAdvisor

Special to the Financial Independence Hub

The term “financial independence” has many meanings to many people.

To some, this means the ability to work on your own terms.

To others, it boils down to not working at all but instead having “enough” to meet all needs and possible wants.

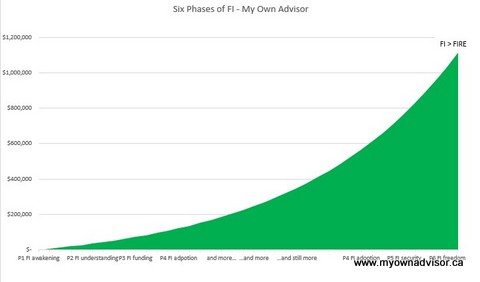

Where do I stand on this subject? This post will tell you in my six phases to financial independence.

Retirement should not be the goal: Financial security and independence should be

Is retirement your goal? To stop working altogether? While I think that’s fine I feel the traditional model of retirement is outdated and quite frankly, not very productive.

As humans, even our lizard brains are smart enough to know we need a sense of purpose to feel fulfilled. Working for decades, saving money for decades, only to come to an abrupt end of any working career might work for some people but it’s not something I aspire to do.

With people living longer, and more diverse needs of our society expanding, the opportunities to contribute and give back are growing as well. To that end, I never really aspire to fully “retire”.

Benefits of financial independence (FI)

In the coming years, I hope to realize some level of financial security and eventually, financial independence. For us, this is a totally worthwhile construct. The realization of FI can bring some key benefits:

- The opportunity to regain more control of our most valuable commodity: time.

- Enhanced opportunities to learn and grow.

- Spend extra money on things that add value to your life, like experiences or entrepreneurship.

Whether it’s establishing a three-day work week, spending more time as a painter, snowboarder, or photographer, or you desire to get back to that woodworking hobby you’ve thought about: financial independence delivers a dose of freedom that’s hard to come by otherwise.

FI funds time for passions.

FI concepts explained elsewhere

There are many takes on what FI means to others.

There is no right or wrong, folks: only models and various assumptions at play.

For kicks, here are some select examples I found from authors and bloggers I follow.

- JL Collins, author of The Simple Path to Wealth, popularized the concept of “F-you money”. This is not necessarily financially independent sums of money but rather, enough money to buy a modest level of time and freedom for something else.

- Various bloggers subscribe to a “4% rule”* whereby you might be able to live off your investments for ~ 30 years, increasing your portfolio withdraws with the rate of inflation.

*Based on research conducted by certified financial planner William Bengen, who looked at various stock market returns and investment scenarios over many decades. The “rule” states that if you begin by withdrawing 4% of your nest egg’s value during your first year of retirement, assuming a 50/50 equity/bond asset mix, and then adjust subsequent withdrawals for inflation, you’ll avoid running out of money for 30 years. Bengen’s math noted you can always withdraw more than 4% of your portfolio in your retirement years however doing so dramatically increases your chances of exhausting your capital sooner than later.

For simplistic math, such bloggers calculated your “FI number” could be approximately your annual expenses x 25. So, if you’re annual expenses are about $40,000 per year (CDN $ or USD $ or other), then your “FI number” is a nest egg value of $1,000,000.

Using that framework, there are levels of FI some bloggers have adopted:

- Half FI – saved up 50% of the end goal (in this case, $1 M).

- Lean FI – saved up >50% of end goal to pay for very lean but life’s essentials like food, shelter and clothing (but nothing else is covered).

- Flex FI – saved up closer to 80% of the end goal, this stage covers most pre-retirement spending including some discretionary expenses.

- Financial Independence (FI) – saved up 100% of the end goal, you have ~ 25 times your annual expenses saved up whereby you could withdraw 4% (or more in good markets) for 30+ years (i.e., the 4% rule).

- Fat FI – saved up at or > 120% of your end goal (in this case $1.2 M for this example), such that your annual withdrawal rate could be closer to 3% (vs. 4%) therefore making your retirement spending plan almost bulletproof.

- There is the concept of “Slow FI” that I like from The Fioneers. The concept of “Slow FI” arose because, using the Fioneers’ wording while “there were many positive things that could come with a decision to pursue FIRE, but I still felt that some aspects of it were at odds with my desire to live my best life now (YOLO).” They went on to state, because “our physical health is not guaranteed, and we could irreparably damage our mental health if we don’t attend to it.”

Well said.

My six phases of financial independence

To the “Slow FI” valuable points, since we all only have one life to live, we should try and embrace happiness in everything we do today and not wait until “retirement” to find it. Continue Reading…