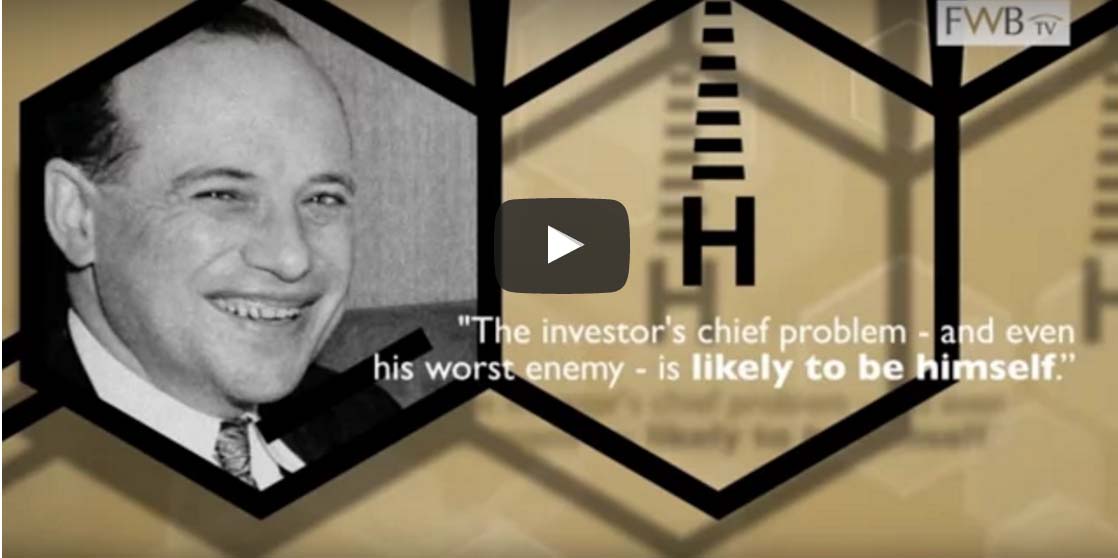

If you’re an investor, there’s a good chance the real enemy is the face you see every morning while shaving (or applying makeup!). The pithy quote in the screen shot is of course from legendary value investor Benjamin Graham.

The main point of this 4-minute video is that successful investing is about controlling what you can. You can’t control what the market does, but you can control what you do in response. In our experience, a person’s returns depend less on whether they pick great investments than on whether they can manage their emotions.

One of the experts in the video describes the physiology of stress that investors suffer during — well, times like the past few weeks! In the heat of volatility, particularly the downward variety, our emotions can get the better of us. There’s a reference to a Cambridge University study of 142 students, all male, who were invited to play a game about trading stocks. They found that the more testosterone they found in the subjects, the greater the risks they took on. Such surges of chemicals and emotion can actually affect your perception of the future, and seldom for the better!

Implications for actively managed funds

Since the Evidence-based Investor Videos largely sing the praises of passive or index investing, you might not be too surprised by a statement that this research may have some implications for investors who use actively managed funds. One source asserts that the investment industry is a stress competitive arena and many fund managers tend to be young males. The decisions they make under pressure and stress may cause them to be overconfident about the stock bets they place on your behalf.

The video concludes that investors may benefit by doing business with a rational, use unemotional advisor.

After watching the video if you want to learn more, download the free guide, 12 Essential Ideas For Building Wealth.

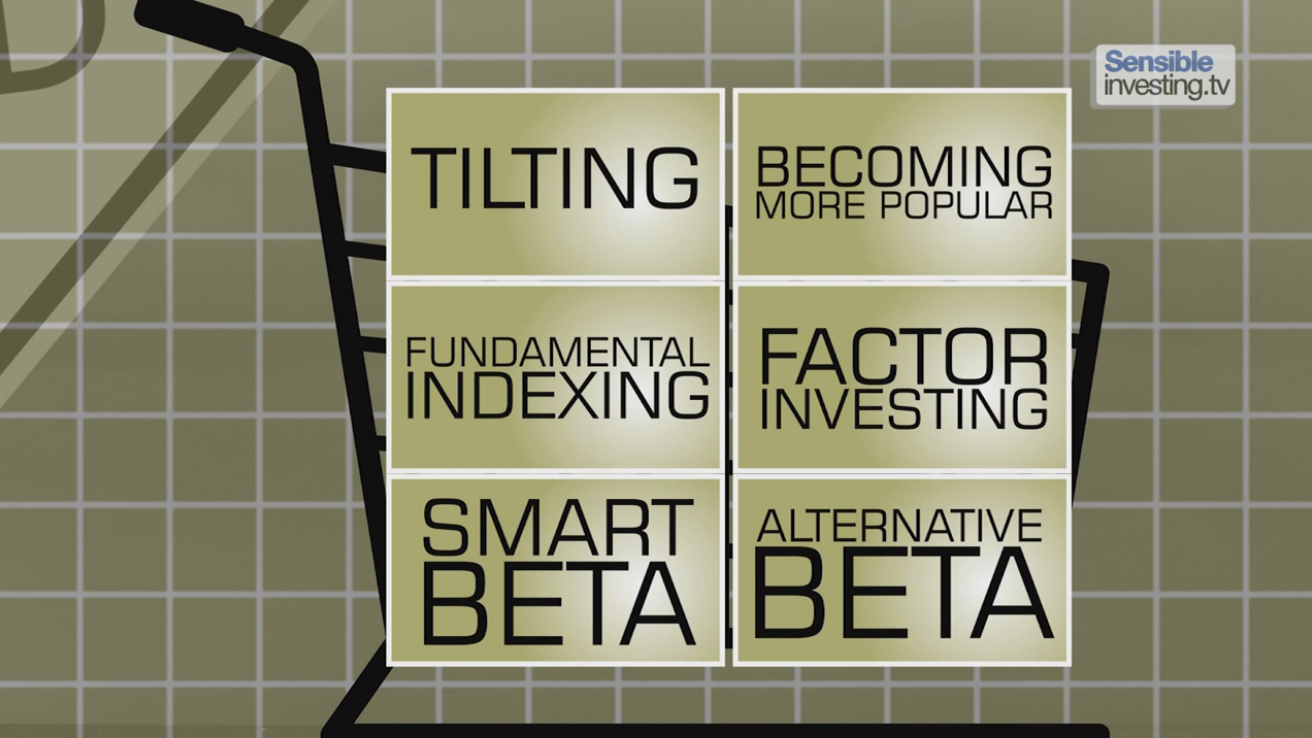

How to Win the Loser’s Game, Part 7

In addition, SensibleInvesting.TV has put up part 7 of the How to Win the Loser’s Game series of videos. While indexing is a relatively simple way to invest, there are still important questions index investor need to ask. Crucially, they need to ensure they are invested in a diverse range of assets that reflects their attitude to risk. They might also want to “tilt” their portfolios to particular risk factors — small-cap or value stocks, for example. While more volatile, these have been shown to deliver higher returns over the long term.

In addition, SensibleInvesting.TV has put up part 7 of the How to Win the Loser’s Game series of videos. While indexing is a relatively simple way to invest, there are still important questions index investor need to ask. Crucially, they need to ensure they are invested in a diverse range of assets that reflects their attitude to risk. They might also want to “tilt” their portfolios to particular risk factors — small-cap or value stocks, for example. While more volatile, these have been shown to deliver higher returns over the long term.