Wohlner (@rwohlner on Twitter) cites a recent survey that found 52% of those approaching retirement said they wish they started saving for the future sooner. 47% wished they had saved more of their pay check and 34% regretted not saving more aggressively. As a result of all this, more than two thirds (68%) of those nearing retirement said they’re not prepared for what’s to come. Therefore, 42% of those between 55 and 64 plan to keep working, at least in a part-time job.

Here are the 7 tips. Click on the link above for full detail on each tip.

View from the Editor-at-Large’s Home Office: May 2014

Now that half a year has passed since my Findependence Day arrived in May, I’ve gotten more clarity about certain misconceptions some may have about the concept of Findependence (aka Financial Independence).

I may even have harboured some of these myself at one point in my full-time career. Here are five myths I’ve become aware of: this is not necessarily a definitive list and may be revisited in the future.

Myth 1: After you’re findependent, you’ll play golf all day, or bridge, or read, or travel.

I doubt this will happen for many unless you really burned out in your career. Depending on the degree of your findependence (see the MoneySense Findependence archives for more on this) and how much work you wish to do, you’ll soon settle into a routine. Most of your tasks may be self imposed, but impose them you will! Between 2004 and 2011 or so, while still working full time at the Financial Post, I devoted many nights and weekends playing to online bridge. Oddly, now that I have more time, I no longer play online bridge, although I do make a point of religiously reading Paul Thurston’s bridge column every day on the “Diversions” page of the National Post. Even with no time lost in a downtown office and getting to and from it, I still don’t have time for online bridge. I may resume once I’m “fully retired” later in my 60s but I can’t seem to find the time for it in semi-retirement!

Myth 2: There’s no distinction between weeks and weekends.

For me, at least, the week and weekend routine still operates at most levels. If you’re familiar with my concept of the 4-hour day (normally practiced from Monday to Friday), then on weekends I do not feel obligated to put in either a four-hour or even just one two-hour stint on money-making or creative activities. Of course, you could redirect at least two hours per weekend from money making to creative fun long term projects you’ve always wanted to accomplish. Because at the end of the weekend, once the workweek resumes for everyone else, longer term projects tend to get crowded out by more imminent matters and deadlines.

That said, it’s also true that – at least if you work from home – you tend to attend to some errands like shopping in the workweek lunch hour, if only as a break and a way to get out of the house. So instead of a large weekend grocery shop, I tend to run two or three times a week on specific shopping missions, but add in a few items I know we’ll need soon. The grocery bills tend to be lower on any given shop but of course you’ll have plenty more of them.

Myth 3: Findependence is an all-or-nothing proposition involving a certain “Big Number.”

Ah, big numbers. Lee Eisenberg wrote a bestseller on that called The Number. If your initial Number was $X million or $Y100 thousand, you may find you continue to push even once it’s achieved. It may become 2X or 3Y. The moment you can declare findependence may be a moving target, depending on financial markets, employers, health and many other considerations. You need to be flexible.

Myth 4: The government won’t be there for me (or employer pensions).

I think whether in U.S. or Canada that the boomer generation can count on the promised social programs and probably the same will hold for succeeding generations. Benefits may not be as generous, may not be inflation hedged, may become means-tested and so on. And yes, these days, it’s hard to count on any one employer pension plan, be it Defined Benefit or newer hybrids that expose workers to some market risk. The whole point of findependence is to establish multiple income streams, which may include part-time earned income or consulting work. That’s a major point Wes Moss makes in his excellent book: You Can Retire Sooner Than You Think.

Government pensions is one basket and an employer pension is a second one but you know what they say about putting all your eggs into any one of them. If I were counting 100% on Social Security (or OAS/CPP in Canada) then I’d be apprehensive about this. And Moss finds the unhappiest retirees are those who can count on only a single source of income.

But as a single potential flow of income that might account for 20 to 60% of the total, the more you have alternatives, the better. RRSPs/IRAs and other savings are one other vehicle, as are taxable accounts and TFSAs/Roth IRAs. But there are also book or music royalties, real estate investment properties, part-time work and finally the subject we wrote about here last week: Internet marketing and entrepreneurship. The Internet has so much potential for creating multiple streams of findependence income that I almost envy the young people now who would far rather become laptop millionaires than salaried employees

. Myth 5: The act of declaring Findependence is irrevocable.

If you’ve left a job or sold a business, you may think the act of declaring your Findependence is irrevocable. It’s not. The truth is you can rejoin the workforce if you wish, though most of the “findependent” people I know who got there before me show not the slightest inclination for returning to another stint on the 9-to-5 treadmill. Lately, I’ve been listening to a Valdy song, Coming Home, which contains the lyric, “I’m going back to places that I couldn’t wait to leave.” When the odd notion comes into my head that it might be fun being full time again in magazines or newspapers, that lyric can’t help but run through my mental iPod.

So those are 5 myths. I’ll revisit this list periodically and probably add to them. Reader input always welcome. Email me at jonathan@findependenceday

This audio clip is from the More Than Money radio show from Calgary, recorded shortly after the Hub launched. The focus was on a MoneySense blog I’d written after the question “Will your retirement date be a surprise?” was posed in a Sun Life poll. But we also touch on the longevity theme that is the focus of the Longevity & Aging section here at the Hub. There’s also an update on the launch of the Hub and the recent e-books.

When you get to the show’s link, just press the small “Play” icon next to my name, or indeed the same icon next to any of the other guests’ names there.

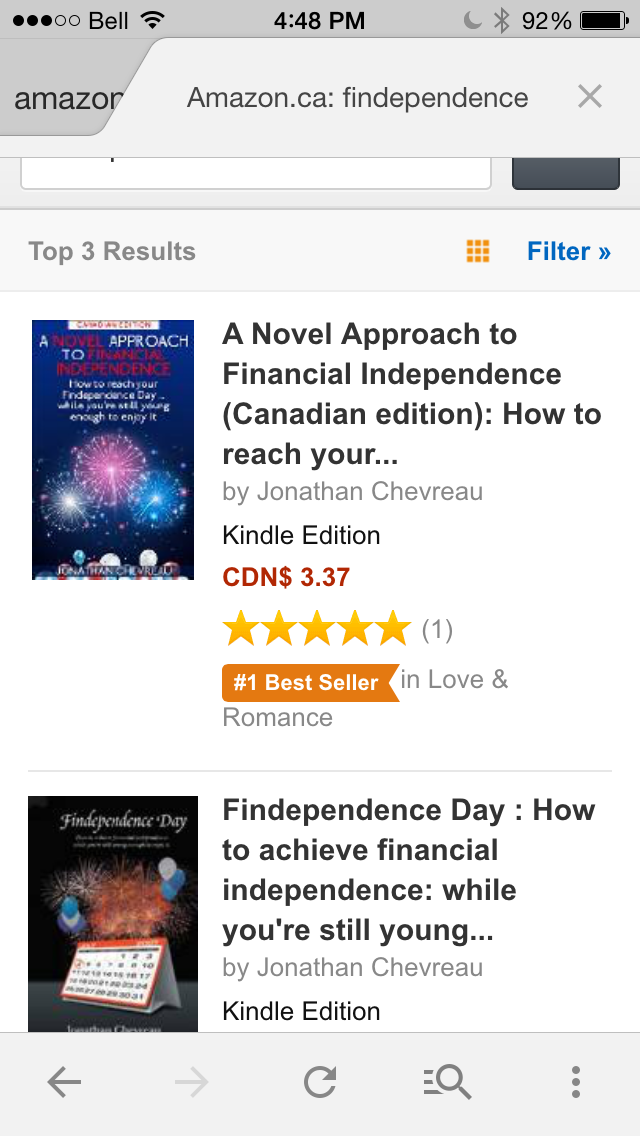

A Novel Approach to Financial Independence is one of the bestselling e-books in Amazon.ca’s Love & Romance category this weekend, as you can see in the screen shot to the right. Here’s the link to Amazon’s listing.

Love & Romance? What about personal finance? Well, I’ve always described the original Findependence Dayas a financial love story so it’s not as out of the box as it may seem at first blush. Click on the red link in the title above to find out more about the Romance plot that’s at the heart of the original novel.

The full book features a couple, Jamie and Sheena, who are 28 at the start and follows their ups and downs as a couple over 22 subsequent years. It takes a “life cycle” approach to personal finance and centers around Jamie’s declaration that he will become financially independent (“findependent”) by the time he turns 50. There are numerous setbacks along the way, including business failure and betrayal, separation, children and more.

As CTV Senior Financial Commentator Patricia Lovett-Reid says in the foreword to both the original book and the e-book, money troubles are often the cause of marital disharmony. You can read that foreword, by the way, for free because it’s near the start and Amazon lets you “look inside.”

e-book is a “Coles Note” synopsis of the novel

I liken the e-book to a “Cole’s Notes” synopsis of the original book, summarizing the plot but focusing more on the content on financial independence. It’s short (15,000 words) but costs only C$3.37. Amazon lets you designate purchases as gifts and with Christmas just around the corner, you have to admit it’s pretty cost-effective! Especially if you can change a young person’s life for the better, as we say in the ad below (also shown on the front page of Findependence.TV).

There is also a U.S. edition of the full novel available here, as well as a U.S. edition of the e-book, which you can find on the main page of this site.

The System Worked was published earlier this year, bearing the tantalizing subtitle: How the World Stopped another Great Depression. I ordered it from the library after reading a New York Times review on it and several related books.

I have to admit it took some time to wade through it, in part because I returned my copy to avoid lugging physical books through Turkey, where I spent three weeks in October. But on my return, I borrowed it again and finished the book.

The author, Daniel Drezner, is a senior fellow at the Brookings Institution and a professor of International Politics at Tufts University. I found his prose somewhat dull but the ideas underlying them are worth mining.

U.S., Europe and China pulled together

In book publishing it’s probably harder to sell an upbeat title than a pessimistic one. (When was the last time a newspaper led off an issue with “No planes fell from the sky yesterday?”) And The System Worked is decidedly upbeat about how governments around the world coordinated their response to what could have been a global economic and stock-market disaster in 2008 and its aftermath. It credits this coordination primarily to the United States first and foremost, ably assisted by the Eurozone and China. Japan, it seems, slipped into a second tier throughout this struggle to avert what otherwise was shaping up to be another Great Depression.

Daniel Drezner (Oxford Press)

The early chapters recap the common perception (a false one in the author’s view) that the system did NOT in fact work: this after Drezner lays out his case for why it did indeed work out splendidly. Those who claim otherwise cite specific trouble spots like the escalation of Europe’s sovereign debt crisis or the failure of climate-change negotiations. Here is a typical upbeat Drezner quotation:

“Even though the initial drop in output and trade levels was more acute in 2008 than in 1929, by any measure the global economy has rebounded more robustly over the past five years than it did during the Depression … The liberal economic order proved to be more robust than expected.”

Certainly, Drezner’s optimism has been justified through late November of 2014. Friday’s twin events of China cutting its interest rates and the ECB’s stimulus talks suggests that the world’s central banks continue to fight the good fight against deflation, depression and other horrors.

But can the system work for more than these first five years?

All of which makes the book’s final chapter all the more tantalizing. Entitled “Where do we go from here?” Drezner repeats his main theme when he says that on policy grounds, both TARP (Troubled Asset Relief Program) and the related Federal Reserve programs were “huge successes” in how they “greatly eased the credit crunch faced by the banks.” This despite the fact TARP “has remained political poison.”

Well, the skeptical reader may say at this point, we may have survived the first five years but can we keep it up? Drezner concedes “there are valid reasons to be concerned about the future.” There is still much fragility in the global economy and the Eurozone “has still not found a viable way to fix the internal imbalances between Germany and southern Europe.” A global recession is quite possible, he admits, and “there are a lot of ways in which things could go wrong” but “given what has happened since 2008, it is safer to conclude that they won’t.”

A big part of his faith is based on what he terms “the enduring strengths of the United States.” These include healthy demographics, geographical security, a dynamic pop culture and excellence in higher education and innovation. Add to that lower oil costs and the fact he believes America will be “the world’s leading oil producer some time before 2020.”

Meanwhile its chief rival, China, is reforming its development model so that “its domestic economy more closely resembles that of the United States.”

Drezner closes with the admission that in the world of international affairs punditry, pessimism sells. Nevertheless, he closes with this:

“Pessimism has spread just as widely as financial contagion did in 2008. It is wrong and needs to be corrected … Going forward, a healthy dollop of optimism is in order.”

From the Chicago Financial Planner, Roger Wohlner, comes these seven retirement savings tips designed to stave off regret.

From the Chicago Financial Planner, Roger Wohlner, comes these seven retirement savings tips designed to stave off regret.