Global stocks are expected to outperform U.S. stocks bonds significantly over the next ten years while US and global bonds will be in the range of 1.3% to 2.4% annualized ,

Here are Vanguard’s 10-year annualized return projections:

- Global equities: 5.2% – 7.2%

- U.S. equities: 2.3% – 4.3%

- Global bonds: 1.3% – 2.3%

- U.S. bonds: 1.4%– 2.4%

The report issued by Valley Forge, PA-based Vanguard is titled Striking a better balance: ironic given its projections for performance of balanced portfolios.

“The road ahead for investors promises to be a challenging one,” said Joe Davis, Vanguard’s global chief economist and co-author of the report. “Global markets will test investors’ discipline as they navigate the risks of unwinding monetary policy support, slower growth, and rising real rates.”

In an advance webinar aired last Thursday, Davis said: “Wage inflation will dictates the pace of rate hikes in 2022.” He said the US Federal reserve is likely to raise rates to at least 2.5% this cycle in order to maintain price stability. As for stocks, we are in an era of “high valuations and low rates,” which creates a “fragile backdrop for markets ….[which] will chip away at future returns.” Better valuations are in developed markets outside the US, small-caps and Value. More stretched valuations are in Emerging Markets, the US, Growth and Large-cap, Davis said.

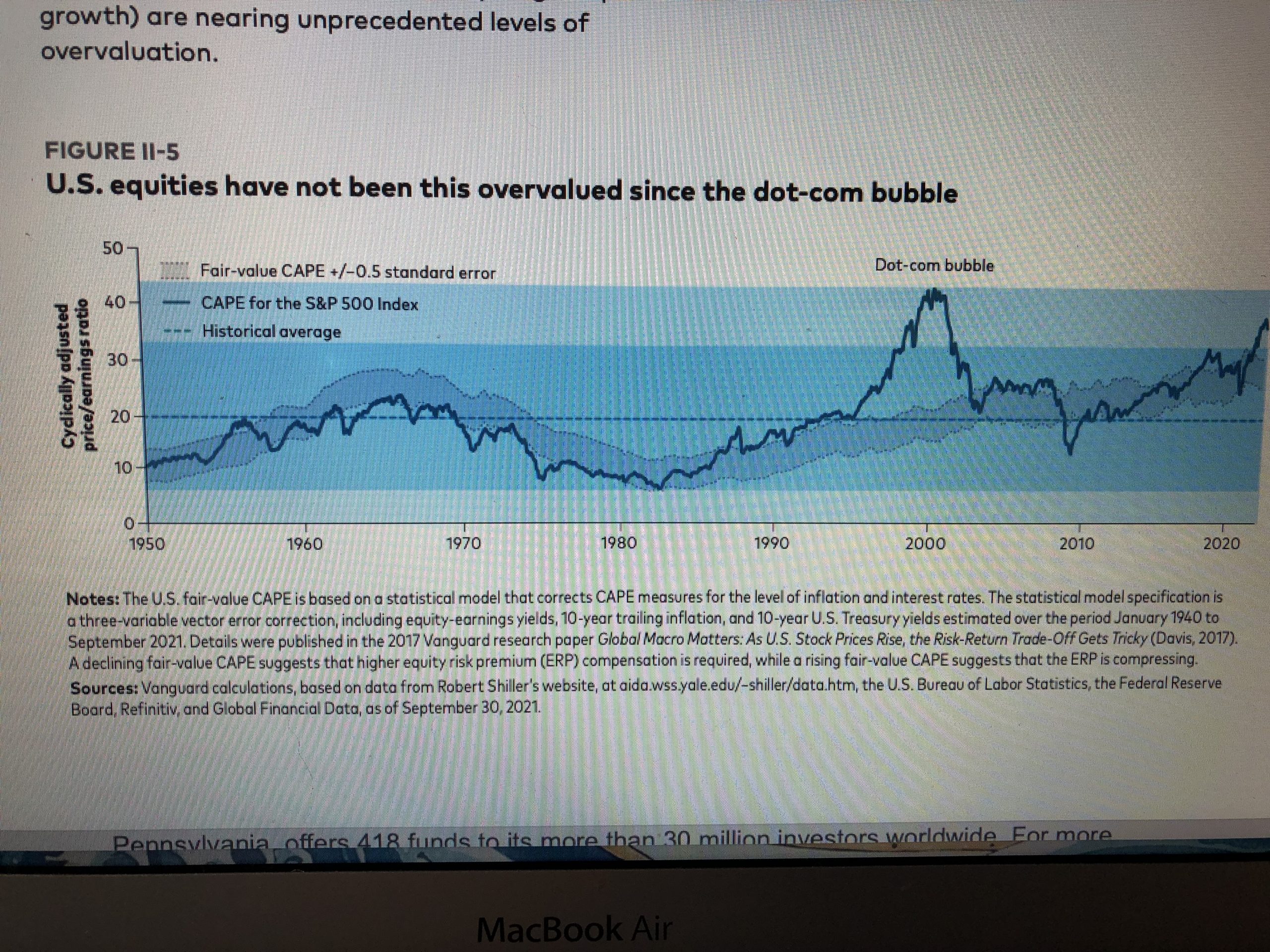

US equities have not been this overvalued since the dot-com bubble, Davis said, adding that a secular decline in rates has been three decades in the marking.

For Bond markets, best values is in TIPS and short-term treasuries. Most stretched are long-term treasuries, mortgage backed securities and international credit. In between are intermediate treasures and high-yield bonds.

Policy accommodations

In Monday’s press release, Vanguard said challenges are likely to be most evident with the unwind of monetary policy, a critical factor in 2022 as central bankers assess a rapidly evolving economic landscape. Inflationary pressures have sharpened the focus on monetary policymakers as these pressures may drive changes in central bank communications and actions. Vanguard projects that central banks will largely try to avoid sharp and unexpected shifts in the timing of policy changes, particularly of policy rate increases, but that conditions will force them to act in 2022 and quite possibly by more than markets are anticipating.

Economic outlook

With the global economic recovery expected to continue in 2022, Vanguard economists foresee the low-hanging fruit of rebounding activity to give way to slower growth, regardless of supply- chain dynamics. In both the U.S. and the Euro area, Vanguard expects economic growth to normalize to 4%. In the U.K., Vanguard expects growth of about 5.5%, and in China, expectations are that growth will fall to about 5%.

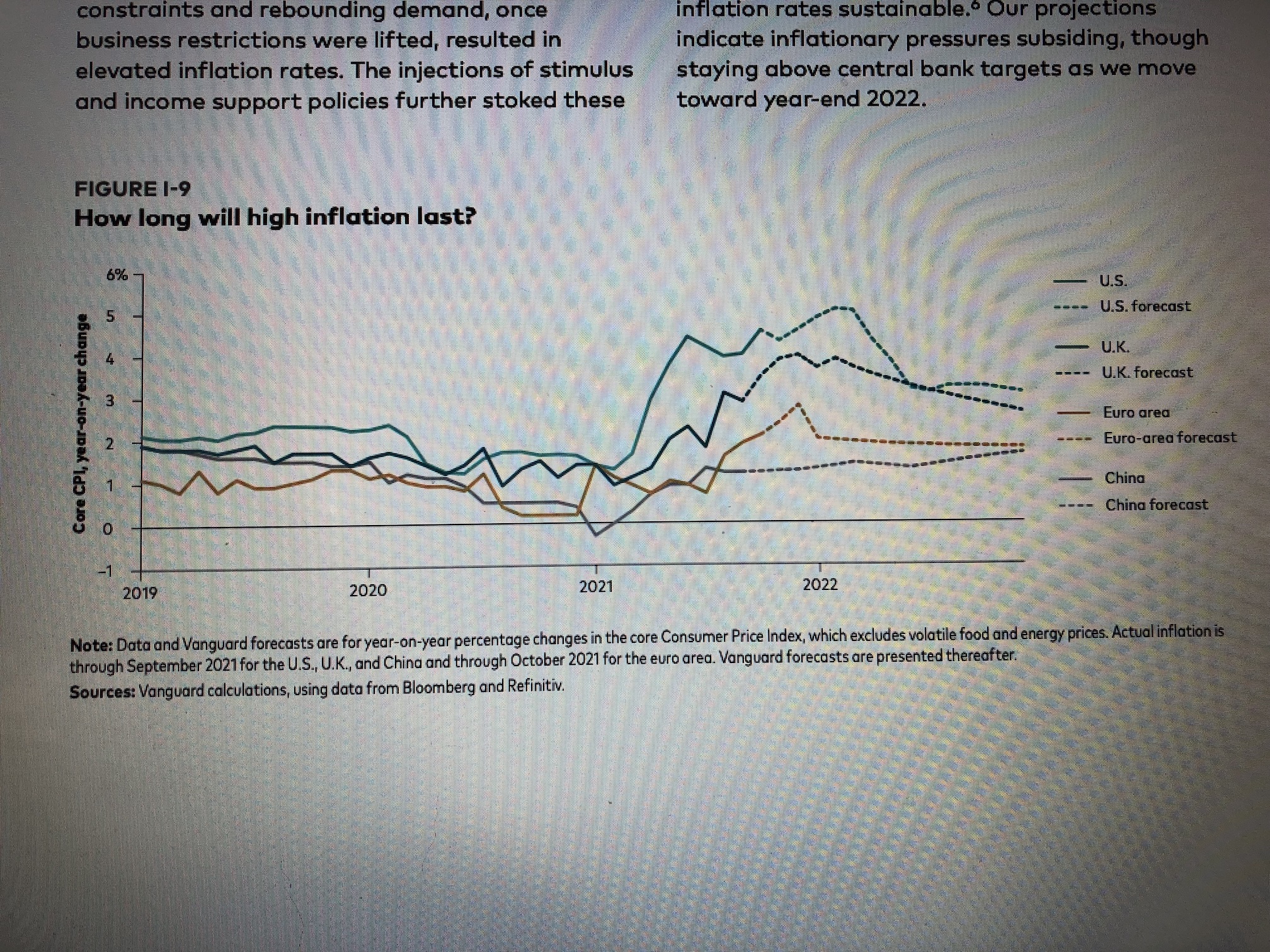

Inflation

Vanguard expects labor markets will continue to tighten, with several major economies quickly approaching full employment. Vanguard estimates the cyclical effects of supply constraints will persist well into early 2022 and then normalize as the structural deflationary forces of technology and unemployment take hold again. These factors contribute to expectations that inflation will trend higher for some time before slowing in the second half of 2022.

Don’t fear a “lost decade” for US stocks but a lower-return one

Vanguard’s long-term outlook for global asset returns for 2022 and beyond remains guarded, particularly for equities where valuations are high and low real interest rates continue to act as a strong gravitational pull on future returns. Investors should not fear a “lost decade” for U.S. stocks, but rather, a lower-return one, it says. For fixed income, low interest rates mean investors should expect lower returns. However, because rates have risen modestly since 2020, Vanguard’s outlook is commensurately higher.

International equities will outperform US in coming decades

Given the differences in valuations between the U.S. and non-U.S. developed markets, Vanguard projects international equities will outperform U.S. equities in the coming decades and value stocks will outperform growth in the U.S.

It says investors are best served in a broadly-diversified portfolio, including international equities.

“While the economic recovery is expected to continue through 2022, easy gains in growth from rebounding activity are behind us, and policy will replace health as the leading consideration for investors,” Davis said, “Despite a potential low-return environment, we are still expecting a positive premium for bearing equity risk. Investors should continue to focus on what they can control, and if they have the patience to weather potential periods of underperformance, we believe accepting some active risk offers the opportunity to offset low future returns.”

Inflation: Transitory with a Twist

At the advance webinar, Vanguard America’s Senior Economist Roger Aliaga-Diaz projects inflation to be “Transitory with a Twist.” He foresees only a modest decline in inflation in 2022. Central banks, including the Fed, will have to normalize sooner than later. “We may see next week [i.e. this week: Dec. 13 to Dec 17] accelerating tapering but not likely to hike rates.” He expects “one or two” hikes in the second half of 2022. Inflation will be around 5% early in 2022 but this should be in the low 3s by the end of 2022. Continue Reading…