By Ambrose O’Callaghan, Harvest ETFs

(Sponsor Blog)

The United States stock markets have delivered positive returns through much of 2024, continuing the positive momentum that was established in the previous year.

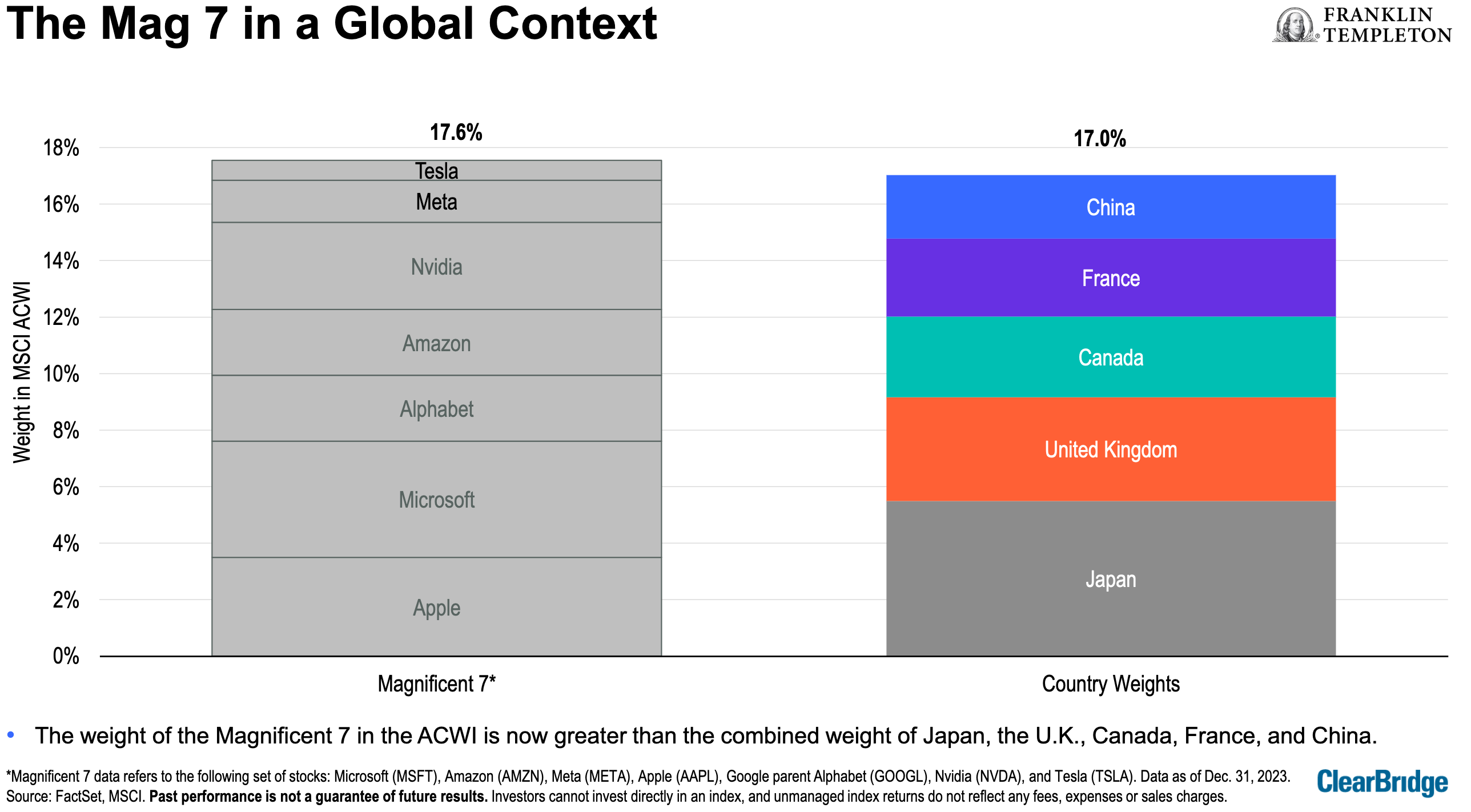

However, that performance has increasingly been powered by a smaller segment of large-cap companies. Indeed, readers have undoubtedly heard about the outsized performance of the “Magnificent 7” in the tech space over the past year. If we strip out the “big six” of Amazon, Meta, Nvidia, Microsoft, Apple, and Alphabet from the S&P 500, we have experienced three calendar quarters of negative earnings growth across the rest of the market.

Investors took profits in the month of April. Demand resumed in the month of May, but with a broader range of equities. Nvidia continued to show its dominance, but there were other sectors and stocks that were able to catch up with the leaders to close out the first half of 2024.

The summer season is historically slow in the markets. Harvest’s portfolio management team expects volatility to persist for both bonds and equities. Moreover, the team emphasizes that this summer is a key moment to stay active, attentive, and invested. A prudent strategy in this environment involves looking under the surface for opportunities while generating cash flow from call options to support total returns.

June Healthcare check up

The healthcare sector pulled back slightly in the month of May 2024. Negative moves in the healthcare sector over the course of May 2024 were driven by stock specific events. Macroeconomic data sets impacted the healthcare sector in line with others. Within healthcare, the managed care subsectors experienced volatility earlier in 2024 and changes to reimbursement structures impacted valuations in the near term. The Tools & Diagnostics sub-sector has also proven volatile due largely to a slower-than-expected recovery in China.

Regardless, there are still very promising opportunities in the GLP-1 drug category space for diabetes and obesity. The uptake of these drugs in the U.S. has been significant at a still-early stage in their lifespan. A recent study from Manulife Canada found that drug claims for anti-obesity medications in Canada rose more than 42% from 2022 to 2023.

Harvest Healthcare Leaders Income ETF (HHL:TSX) offers exposure to the innovative leaders in this vital sector. This equally weighted portfolio of 20 large-cap global Healthcare companies aims to select stocks for their potential to provide attractive monthly income as well as long-term growth. HHL is the largest active healthcare ETF in Canada and boasts a high monthly cash distribution of $0.0583.

Harvest Healthcare Leaders Enhanced Income ETF (HHLE:TSX) is built to provide higher income every month by applying modest leverage to HHL. It last paid out a monthly cash distribution of $0.0913 per unit. That represents a current yield of 10.44% as at June 14, 2024.

Where does the technology sector stand right now?

Investors poured back into technology stocks in May 2024 after taking profits in the month of April. However, they were more discriminating than in previous months and showed a preference for hardware stocks, specifically semiconductors.

Nvidia maintained its leadership position. It has soared past a $3 trillion market capitalization in the first half of June 2024. However, other AI-related tech stocks encountered turbulence which may give some investors pause around the broader bullish case for AI. Continue Reading…