Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Gold prices have gained more than 14% since late last year, renewing market interest for the precious metal.

Recent gains have been driven by an expectation that the U.S. Federal Reserve (Fed) is getting closer to reducing its trendsetting overnight rate, which led to a weaker U.S. dollar index to close 2023.

In recent months, inflation concerns have ramped back up with recent U.S. CPI data coming in slightly ahead of expectations. While consumer prices continue to trend in the right direction, higher shipping costs are becoming a concern with cargo ships having to avoid the Suez Canal. Shipping costs have surged 150% as a result, potentially add 0.5% percentage points to core inflation1: and re-igniting worries that CPI could accelerate again.

These developments have created a favourable environment for gold, given bullion tends to be used as a multi-purpose hedge for portfolios.

BMO Global Asset Management has launched a gold ETF that is backed by physical bullion. This ETF stores physical 400-oz. bars, secured in a local vault operated by BMO. Investing in the new BMO Gold Bullion ETF is efficient for investors as it is listed on the Toronto Stock Exchange (TSX) and trades like any stock or ETF. Additionally, since the underlying bullion holdings are professionally vaulted, investors do not have to worry about safe-keeping on their own. The BMO Gold Bullion ETFs are available at a cost-efficient management fee of 0.20%.

Amid reaccelerating inflation concerns and interest rate uncertainty, gold could be used as a defensive hedge.

Macro as well as weaker-U.S. dollar risks have risen in recent years, and could remain elevated going forward.

Gold offers effective diversification from stocks and bonds, which have experienced a notable rise in correlation3.

Why Gold could continue to Glitter

Gold is often used to hedge three main risks: macro-economic/geopolitical and inflation risks, as well as against a weaker U.S. dollar and fiat currencies4. All of these risks have risen in recent years and it is quite possible and perhaps probable that they will remain elevated going forward, spurring further demand. Continue Reading…

2024 brings exciting opportunities for homebuyers in the real estate market. The market is poised for growth with the ongoing demand for housing and favorable economic conditions. However, buyers must navigate this landscape with informed decision-making.

With interest rates expected to be cut by the Fed, the real estate market could experience a boom, and there are various options available for homebuyers. That said, it’s essential for potential buyers to prepare their finances ahead of time and explore affordable mortgage options. In addition, buyers should prioritize must-have features and location preferences to narrow their search.

Below, you’ll discover 7 crucial tips for homebuyers in 2024. Homebuyers can confidently navigate the market by following these tips and achieve successful results in 2024.

Importance of Informed Decision-Making

In the competitive real estate market of 2024, informed decision-making is crucial for homebuyers. Buyers can make well-informed choices that align with their goals and preferences by conducting thorough research and staying updated on market trends.

Being informed allows buyers to understand the current market conditions, such as housing inventory and pricing trends, enabling them to make competitive offers and negotiate effectively.

Moreover, buyers can ensure they are investing in a desirable location by gathering information about the neighborhood, schools, amenities, and future development plans.

Informed decision-making also involves assessing the property’s condition, conducting inspections, and considering potential renovations or repairs. By making informed decisions, homebuyers can minimize risks, maximize their investment, and achieve long-term satisfaction with their purchase.

Financial Readiness and Budgeting

Financial readiness and budgeting are essential for homebuyers to navigate the 2024 real estate market. It is crucial to carefully assess personal finances and establish a realistic budget to ensure a successful buying process.

Typically, banks have more stringent requirements than other lenders when trying to secure a mortgage to buy a home. That said, homebuyers should strive to save for a down payment and maintain a strong credit score to increase their chances of securing a favorable mortgage rate.

Buyers can enhance their financial position and have a stronger negotiating stance by managing debts and ensuring sufficient savings.

Additionally, it is important to consider other costs associated with homeownership, such as property taxes, insurance, and maintenance.

By creating a comprehensive budget and sticking to it, homebuyers can confidently navigate the market and make informed decisions that align with their financial capabilities and long-term goals.

When buying a home in 2024, it is important to identify the must-have features and prioritize the location based on personal preferences and needs. Homebuyers should consider factors such as the number of bedrooms and bathrooms, the size of the yard, and the availability of amenities like parking and storage space.

It’s also important to assess the proximity to schools, healthcare facilities, and transportation options. Making a list of non-negotiable features will help streamline the home search process and ensure that the chosen property aligns with the buyer’s lifestyle and long-term goals.

By prioritizing the features and the location, homebuyers can find a property that meets their needs and enhances their overall living experience.

Due Diligence: Inspections and Property Conditions

During the home buying process, one critical step is conducting due diligence, specifically inspections and assessing property conditions. It is crucial to thoroughly examine the property to identify any potential issues or concerns before making a final decision. Hiring a certified home inspector can provide a comprehensive report on the property’s structural integrity, electrical systems, plumbing, and other essential components.

Inspecting the property’s exterior, including the roof, foundation, and drainage systems, is also recommended. Evaluating property conditions helps buyers understand the potential costs and repairs they may incur.

Homebuyers can make informed decisions by conducting due diligence and negotiate any necessary repairs or modifications with the seller.

Crafting competitive offers and managing Negotiations

Once you have found your ideal home, it’s time to craft a competitive offer and effectively manage negotiations. Start by determining the property’s fair market value based on recent sales and comparable properties in the area. This will help you make a strong, yet reasonable, offer.

Consider including contingencies in your offer, such as a home inspection or appraisal contingency, to protect yourself from potential issues. Remember, negotiations are a give-and-take process. Be prepared to negotiate on price, repairs, or other terms with the seller. Continue Reading…

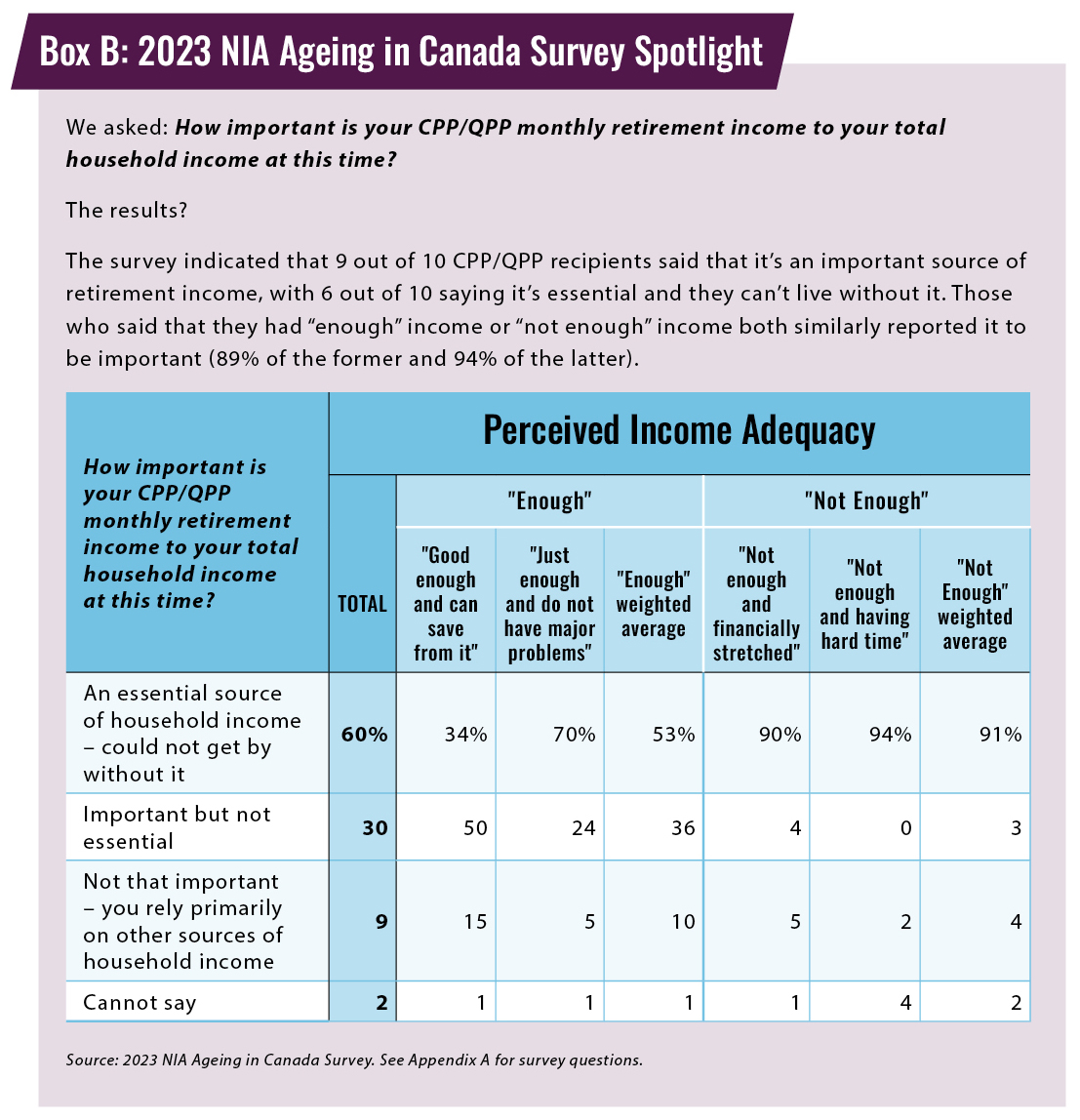

My latest MoneySense Retired Money looks in more detail at the National Institute of Ageing’s recent series of papers on CPP (and OAS). As the Hub reported on April 11th, few Canadians are aware that delaying CPP benefits to age 70 can more than double (2.2 times actually) eventual monthly benefits compared to taking it early at age 60. That blog reproduced a chart from the NIA that showed just how much money Canadians are leaving on the table by NOT deferring benefits as long as possible.

The other major chart from the NIA paper is reproduced above, showing just how important most retirees view the guaranteed inflation-indexed income that CPP and OAS provide. As the new column points out, for many retirees — especially those who worked most of their careers in the private sector and don’t enjoy a Defined Benefit employer pension — CPP and OAS are the closest thing they’ll have to a guaranteed-for-life inflation-indexed annuity.

The new MoneySense column focuses on how delayed CPP benefits not only generate higher absolute amounts of income but also carry with it the important related benefits of more longevity insurance and inflation protection.

It features input from several well-known retirement experts, including noted finance professor and author Dr. Moshe Milvevsky, retired Mercer actuary Malcolm Hamilton, author and semi-retired actuary Fred Vettese, TriDelta Senior Financial Planner Matthew Ardrey and the lead author of the NIA report, Bonnie Jean MacDonald.

Delaying CPP is “the best annuity-buying strategy you can implement.”

Milevsky sums it up well, when he says “delaying CPP is the best ‘annuity-buying strategy’ you can implement. Everything else is just Plan B.” Audrey makes a similar point: CPP is “an annuity and an indexed annuity at that … This helps protect the purchasing power of this income stream through retirement. Many people wish they had an indexed DB [defined benefit] pension and in fact we all do. It is the CPP.”

You’ll probably see much more press on this topic as the NIA is releasing a paper each month between May and December. May 8th will be general education on the Canadian retirement income system while July 17th will explain the mechanics of delaying CPP (and QPP) benefits.

Understanding the impact of financial education on wealth-building, we’ve gathered insights from Directors, Founders, and CEOs, among others, to share their experiences and lessons. From fostering open family financial talks to the importance of reinvesting profits for startup growth, explore the eleven valuable strategies these experts attribute to achieving financial independence.

Foster Open Family Financial Talks

Invest in Low-Cost Index Funds

Leverage Compound Interest Early

Learn from Real Estate Investment

Implement Simple Numbers Cash Flow Management

Educate to Protect Wealth

Invest Early, Understand Market Trends

Budget with The Total Money Makeover

Navigate with Financial Education

Avoid Emotional Investing

Reinvest Profits for Startup Growth

Foster open Family Financial Talks

I strongly advise families to prioritize open and honest communication about family finances. It is pretty common in most families to not discuss money. I am a firm believer that regular discussions about finances, budgeting, and investments will strengthen your relationship and prioritize a secure financial future.

Financial literacy is crucial, regardless of asset levels. As a CFP®, my role extends beyond managing investments or creating financial plans; I also serve as an educator for families. By providing personalized guidance and educational resources, I help families bridge the gap in financial knowledge and deepen their understanding of their financial situation. This empowers both the parents and children to contribute meaningfully and reduces the likelihood of misunderstandings or financial disagreements. This collaborative approach with your certified financial planner can provide personalized guidance and help couples navigate these important decisions together.

The more you save and the earlier you save, the better. Your future self will thank you!

You also need an emergency fund. You need to expect the unexpected. Have six months of expenses earmarked in a high-yield savings account.

The secret to building wealth is living below your means. You need to be clear on the income coming in and the expenses going out. Pay yourself first. The results of compound interest are powerful. As your income increases, lifestyle inflation creeps in. Avoid the urge to spend more as you make more. Save more. Invest the difference. Your future self will thank you. — Melissa Pavone, Director of Investments CFP, CDFA, Oppenheimer & Co. Inc.

Invest in low-cost Index Funds

Despite working in Financial Services for over 20 years, I’ve only truly educated myself about Financial Independence within the last few years.

Fortunately, I had been doing most things right all along; saving a decent proportion of my salary each month, using tax-efficient savings vehicles, maximizing my employer’s pension contributions, etc. Where I messed up, to some extent, was in what I was investing my hard-earned savings in.

Being a sucker for actively managed funds, individual stocks, etc., has hampered the growth of my portfolio over the years. I am now invested exclusively in low-cost index-tracking funds, and I wish I had decided to do this years ago.

My eyes were finally opened to the low-cost passive index tracker approach when a friend recommended I read a book called The Little Book of Common Sense Investing by John Bogle (the founder of Vanguard). It’s a great book that totally changed my outlook on investing. — Jonathan Wright, Founder, Aiming For FIRE

Leverage Compound Interest early

I have built wealth and achieved financial independence primarily through financial education. It has provided me with the necessary tools for making informed investment decisions, managing risks effectively, and optimizing tax strategies. Financial education has been an important platform for understanding the dynamics of the market and developing a disciplined approach to saving, investing, and spending.

The most valuable lesson I ever learned was about compound interest. Compound interest can turn modest savings into substantial wealth over time. The key is to start early, save consistently, and reinvest earnings. Even small amounts saved regularly can grow exponentially due to the compounding effect, highlighting the importance of patience and discipline in wealth building.

Another critical lesson is the importance of living below your means and investing the surplus wisely. It’s not just about how much you earn, but how much you save and invest that counts towards building long-term wealth. When you prioritize savings and investments, you create a buffer for unexpected expenses and have the potential to achieve financial independence sooner. — Sherman Standberry, CPA and Managing Partner, My CPA Coach

Learn from Real Estate Investment

When I was growing up, my grandfather gave me an excellent financial education through his example. He was a real estate investor, and thanks to his investments, he was able to retire early while helping my brother and me pay for college. I decided to follow his example and started buying real estate after college.

Now, my portfolio is worth seven figures. The big lesson I learned from my grandfather is that to be truly financially free, you have to find a way to earn money without having to work all the time. And with real estate, that’s possible. — Ryan Chaw, Founder and Real Estate Investor, Newbie Real Estate Investing

Implement Simple Numbers Cash Flow Management

We run a fast-growing small-business law firm and are devoted fans and implementers of Simple Numbers by Greg Crabtree. I frequently give copies of the book to our clients, and they invariably thank me later.

Greg’s advice about how to view your cash flow and responsibly manage it has been foundational to our and our clients’ success. — Matthew Davis, CEO, Davis Business Law

Educate to Protect Wealth

In co-founding Silver Fox Secure, I’ve directly observed the impact that financial education has on protecting and building wealth, especially among vulnerable populations. A key lesson that stands at the core of our mission is the critical role of preemptive measures in safeguarding one’s financial health. Through our work, we’ve implemented comprehensive identity-theft protection and credit-monitoring solutions that not only serve as a defense mechanism but also educate our clients on the importance of regular financial oversight.

One pivotal example from our experience was helping a group of seniors who were targeted in a sophisticated phishing scam. By providing them with personalized education on recognizing such threats and monitoring their financial activities through our services, we turned a potentially devastating situation into a valuable learning opportunity. This incident underscored the importance of proactive financial education, showing that knowledge is as vital as the technical solutions we offer in preventing financial exploitation.

Furthermore, our efforts have highlighted the necessity of tailored financial strategies to address specific risks associated with different demographics, such as active military personnel and individuals with mental or physical disadvantages. By focusing on the unique vulnerabilities of these groups, we’ve developed targeted educational materials and monitoring strategies. This approach has not only protected our clients’ financial assets but has also empowered them with the knowledge to make informed decisions about their financial security in the future. Through these experiences, I’ve learned that combining cutting-edge technological solutions with personalized education fosters a robust environment of financial independence and security. == Jenna Trigg, Co-Founder, Silver Fox Secure

Invest Early, Understand Market Trends

Financial education has been at the core of my journey in founding BlueSky Wealth Advisors and helping others achieve financial independence. A crucial lesson I’ve learned, and often share, is the importance of early investment and the power of understanding the market’s long-term trends. For instance, an initial $1 investment in the stock market in 1926 could have grown to over $13,000 today, despite numerous economic downturns along the way. This emphasizes not just the value of patience and perseverance in investing, but also the vital role of financial knowledge in distinguishing between short-term noise and long-term growth opportunities.

In the realm of education investment, I’ve observed the significant impact financial education has on making informed decisions regarding one’s or one’s child’s educational future. The story of my client’s son, Sammy, who pursued a $200,000 education in a competitive field only to start with a $30,000 salary, underlines the importance of weighing the value of a degree against its cost and potential debt burden. It’s not just about getting any education but making educated financial decisions regarding that education. This example highlights the necessity to have a financial plan that incorporates smart strategies towards education funding to avoid jeopardizing one’s financial independence. Continue Reading…

Boating is an adventure at any age, but it often becomes a lifestyle for retirees. If you’ve ever considered trying to save up for a boat one day this could be a good read. With a couple of these financial tips, you’ll be well on your way to living your boating dream!

Adobe Image courtesy Logical Position/Visionsi

By Dan Coconate

Special to Financial Independence Hub

Retirement is a time for relaxation, adventure, and a well-deserved break from the toils of work. For many, it’s the perfect time for ticking off items on the bucket list and enjoying activities they couldn’t do before, such as boating. Setting sail on serene waters has a draw that’s hard to resist, especially once you’ve reached your golden years, but it can unfortunately be an expensive hobby. With these financial tips, investing in a boat for retirement is within reach.

Why Invest in a Boat?

Investing in a boat can offer several benefits depending on your interests as well as your lifestyle. In many cases, the most common reasons as to why one would invest in a boat is for recreation/leisure, family time, and adventure!

In the financial world, large purchases are seldom one-dimensional. However, they can be gateways to new experiences or investment opportunities. A boat, with its allure of freedom and tranquility, often blinds potential owners to its financial complexities. With a good understanding of your needs and what’s available, you can spend your glory days in luxury and comfort.

Don’t forget that investing in a boat depends greatly on the individual themselves and what they are comfortable in affording. As great as it is to own one, you don’t want it to feel like you’re being submerged by a financial burden especially towards your later years in life. Find something that you can truly afford and go from there.

Understanding the Cost of Ownership

As mentioned above, owning a boat depends greatly on the individual themself and what they can afford. The financial commitments of boat ownership extend far beyond the initial purchase price. From understanding the dos and don’ts of marine craft maintenance to preparing your vessel for foul weather, upkeep can turn the investment into a bottomless expense if not managed wisely.

Here are some common costs that every prospective boat owner should consider:

Purchase Price: The upfront cost varies widely based on the boat’s type and age.

Maintenance and Repairs: Regular upkeep, including engine maintenance, hull cleaning, and repairs.

Docking Fees: Charges for mooring or storing your boat at a marina or docking facility.

Insurance: Protection against accidents, theft, and natural disasters.

Fuel: Operational expense that can fluctuate with usage and fuel market prices.

Safety Equipment: Initial purchase and replacement costs for items such as life jackets, fire extinguishers, and flares.

Understanding these costs is imperative, as they can tally up faster than the wakes behind a speedboat.

Legal and Financial Considerations

There are also key legal and tax-based implications of boat ownership. When considering the various forms of state and federal taxes on a boat’s purchase, operation, and potential resale, the financial burden can become relatively heavy. Annual or biennial fees can add up and make it difficult to ascertain the full price of boat ownership beforehand. Continue Reading…