Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Stock market traders use a lot of jargon. Terms like “haircut,” “candlestick,” and “circuit breaker” are commonplace in the trading community, but for the average investor, not so much.

For the most part, knowing the meanings of these terms is not critical. However, there are some terms used by traders that investors should know and understand well because they’re used on a regular basis. So, in this article, I’ll share what I consider to be some of the most important terms to know when it comes to investing: bid, ask, and spread.

Bid: The highest price a buyer will pay for a stock

A trader seeking to purchase a stock or other asset will make their intent known by placing a “bid.” The bid represents the highest price the buyer is willing to pay for the stock. Establishing a bid is not only important for the buyer, but also the seller: the range of bids from interested buyers helps sellers determine how much market interest there is in a particular stock.

Ask: The lowest price a seller will accept for a stock

On the opposite side, an “ask” refers to the lowest price a seller is willing to sell a stock for. The ask represents the supply side for a market for any given stock, while the bids represent demand.

Bid-ask spread: The difference between the ask and bid

Typically, the ask — also known as the “offer price” — will be higher than the bid. The difference between the bid and the ask is known as the “bid-ask spread,” or simply the “spread.” The smaller the spread, the easier it is to buy or sell a stock. That’s because, with smaller spread, less movement is needed to bring buyers and sellers to an agreeable price and conduct a transaction. Generally speaking, stocks and other assets that are being traded in higher volumes tend to have smaller spreads. Continue Reading…

A revolutionary new approach to preserving portfolio longevity through a modern “Tontine” structure was unveiled Wednesday by Guardian Capital LP and famed author and finance professor Moshe Milevsky.

GuardPath™ Longevity Solutions, created in partnership between Guardian and Schulich School of Business finance professor Milevsky, is designed to address what Nobel Laureate Economist William Sharpe has described as the “nastiest, hardest problem in finance” 1

Announced in Toronto on September 7, a press release declares that the “ground-breaking step” aims to “solve the misalignment between human and portfolio longevity.” See also this story in Wednesday’s Globe & Mail.

Over the years, I have often interviewed Dr. Milevsky about Retirement, Longevity, Annuities and his unique take on how the ancient “Tontine” structure can help long-lived investors in their quest not to outlive their money. Milevsky has written 17 books, including his most recent one on this exact topic: How to Build a Modern Tontine. [See cover photo below.]

Back in 2015, I wrote two MoneySense Retired Money columns on tontines and Milevsky’s hopes that they would one day be incorporated by the financial industry. Part one is here and part two here. See also my 2021 column on another pioneering Canadian initiative in longevity insurance: Purpose Investment Inc.’s Longevity Pension Fund.

Addressing the biggest risks faced by Retirees

In the release, Milevsky describes the new offering as a “made-in-Canada” solution that addresses “the biggest risks facing retirees and are among the first of their kind globally. Based on hundreds of years of research and improvement and backed by Guardian Capital’s 60-year reputation for doing what’s right for Canadian investors, I am confident these solutions will revolutionize the retirement space.”

Milevsky’s latest book is on Modern Tontines

In an email to me Milevsky said: “You and I have talked (many times) about tontines as a possible solution for retirement income decumulation versus annuities. Until now it’s all been academic theory and published books, but I finally managed to convince a (Canadian) company to get behind the idea.”

In the news release, Guardian Capital Managing Director and Head of Canadian Retail Asset Management Barry Gordon said that “for too many years, Canadian retirees have feared outliving the nest egg they have worked so hard to create.” It has answered that concern by creating three solutions that aim to alleviate retirees’ greatest financial fears: The three solutions are described at the bottom of this blog.

With the number of persons aged 85 and older having doubled since 2001, and projections suggesting this number could triple by 2046,2 Guardian Capital says it “set out to create innovative solutions that this demographic could utilize when seeking a greater sense of financial security.”

Tontines leap from Pop Culture to 21st Century reality

Tontines were one of the most popular financial products for hundreds of years for individuals willing to trade off legacy for more income, Guardian says. Once in a while the tontine shows up in popular culture, notably in the film The Wrong Box, where the plot revolves around a group of people hoping to be the last survivor in a tontine and therefore the recipient of a large payout.

“With our modern tontine, investors concerned about outliving their nest egg pool their assets and are entitled to their share of the pool as it winds up 20 years from now,” Gordon says, “Over that 20-year period, we seek to grow the invested capital as much as possible to maximize the longevity payout. Along the way, investors that redeem early or pass away leave a portion of their assets in the pool to the benefit of surviving unitholders, boosting the rate of return. All surviving unitholders in 20 years will participate in any growth in the tontine’s assets, generated from compound growth and the pooling of survivorship credits. This payout can be used to fund their later years of life as they see fit, and aims to ensure that investors don’t outlive their investment portfolio.” Continue Reading…

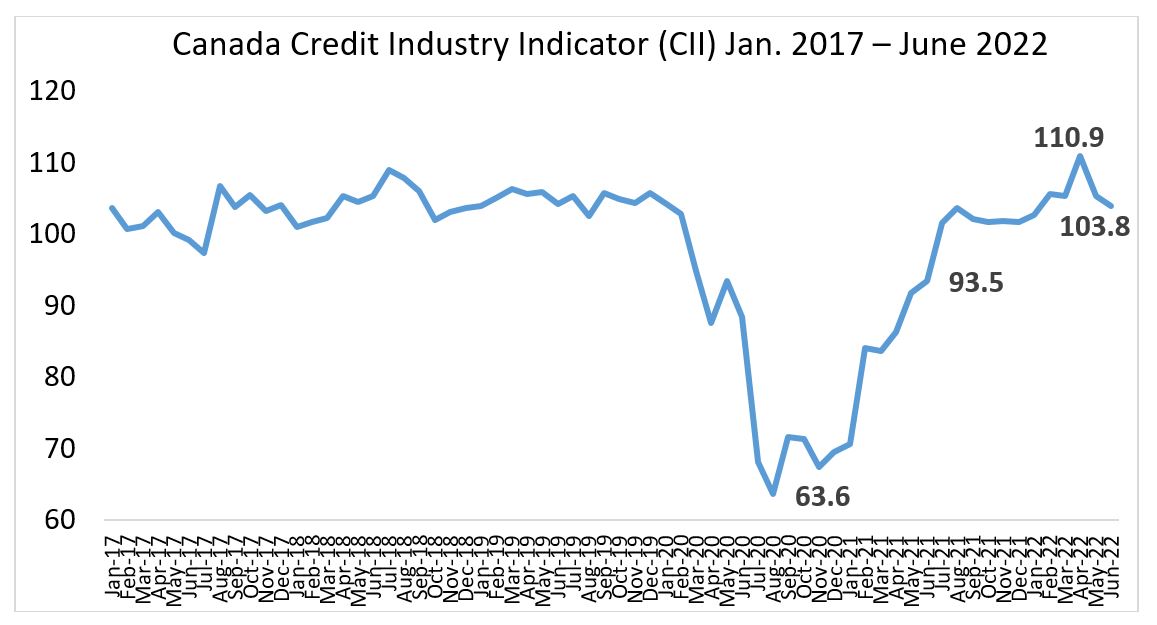

The double whammy of Inflation and rising interest rates are starting to be reflected in higher debt levels for Canadians, according to data released by TransUnion on Tuesday.

The Q2 2022 Credit Industry Insights Reportreveals that Canadians are vulnerable to payment shock as a result of high interest rates and inflation challenges: “While there have still been gains in GDP growth and low unemployment, they are being offset by higher interest rates and cost of living. This lead to higher credit balances and increased costs of mortgages and loans.”

The report shows total debt grew to an all-time high at $2.24 trillion, up 9.2% year-over-year (YoY) and up 16.4% from pre-pandemic levels observed at the end of 2019. The number of consumers with a credit balance has increased by 2.1% YoY to 27.6 million and is up 2.5% from pre-pandemic levels (Q4 2019).

Household finances were worse than planned for 41% of consumers, with 48% reporting they had cut back on discretionary spending. A startling 26% of consumers expect to be unable to repay their bills and loans.

Total debt grew to an all-time high at $2.24 trillion, up 9.2% from the same time in 2021 and up 16.4% from pre-pandemic levels at the end of 2019.

Consumer delinquency on personal loans has returned to pre-pandemic levels, up 19 base points (bps) YoY to 0.93%. Credit card delinquency is also up six bps from the prior year same quarter.

Increased balance growth was observed across all risk tiers, with super prime consumers continuing to build overall outstanding balances (+5.1% YoY).

In the release, TransUnion director of financial services research and consulting Matt Fabian says: “With the combination of higher cost of living and higher spend driving up credit balances, along with the recent surge in mortgages and auto loans, many Canadian consumers are under pressure from higher debt service obligations … We’ve seen an increase in miminum payment amounts of up to 10% in the first half of 2022, depending on the combination of products consumers hold, along with a slight deterioration in payment behaviours.”

As shown in the chart below, all major credit products saw an increase in average balance per borrower, which TransUnion says indicates the consumer need to leverage credit.

Fabian added that “During the pandemic we saw a decline in credit participation among below prime consumers, so this marks a re-engagement of this segment as potentially the effects of inflation and interest rates have driven demand, while lenders have increased their risk appetite in this space.”

The report shows that overall, consumer-level delinquencies (borrowers more than 90 days past due on any account) increased by four basis points (bps) over the prior year same quarter, but still remain below pre-pandemic levels. “Consumer delinquency on personal loans has returned to pre-pandemic levels, up 19 bps YoY, to 0.93%.” Credit card delinquency (90 days or more past due) is higher by six bps from the prior year same quarter.

TransUnion says the increase in consumer delinquencies is partially explained by accelerated lender origination activity, especially in the below-prime space: “The YoY rises in delinquencies are generally small and not a major concern, given the increased credit activity observed post pandemic. As credit activity recovers and grows further, consumer credit performance is expected to return to near pre-pandemic levels.”

This is a common headline in personal finance and although the details are nuanced, the headline can give the wrong impression: that you shouldn’t rely on the equity in your home to fund your retirement.

Certainly, it shouldn’t be the only source of retirement income: homeowners also have to save using RRSPs and TFSAs. However, homeowners in high-priced housing markets will likely have excess equity in their homes that should be considered when building a retirement plan and determining how much they need to save.

The rationale for the “don’t rely on your home for retirement” advice is twofold: first, that you will always need a place to live and the value of your home will be needed to buy or rent another residence; and second, that you need money to buy food and other things, which you can’t do if all your wealth is tied up in your home.

Both these points are valid, but they don’t apply to everyone. Like all aspects of financial planning, each individual’s personal circumstances need to be considered and in fact, many people should count on their home to help fund their retirement.

You’ll always need a place to live

To address the first point — that your current home will fund your next home — consider doing an analysis that looks at the cost of renting for the years after you sell your home. For those in high-priced housing markets like Toronto, the proceeds from selling a mortgage-free home will likely more than offset the cost of renting for 30 years in retirement, including paying for long-term care. The same analysis applies to downsizing by buying a smaller place in a less-expensive market. This means there could very well be excess funds that can be used later in life and this should be accounted for when determining how much retirement savings you need. Continue Reading…

Whether or not you consider building wealth a complicated process, the fact is that there are time-tested paths to make it happen. Increasing your net worth and building generational wealth is never unintentional; this article described six unique ways to help you do it.

Build Solutions for Unique Problems

All of the world’s wealthiest people, self-made millionaires, created solutions for global problems, and that’s why they became rich. You may argue that most industries already have wealthy giants, but you can find a niche with a growing problem and design a solution. Scale the solution for the global market, and you would have made a step in building generational wealth.

Invest in Profitable Startups

Investment has always been key to building wealth. If you invest early in a business, you position yourself for massive profits when the business grows. Carefully profile startups and invest in them. You should hire a financial advisor or learn more about investment before doing this.

Hire a Debt Management service

You may get into debt as you invest and build a business. Debt is not necessarily wrong when taking loans to build a business, but it could easily cripple your finances. Debt management helps you overcome depth without declaring bankruptcy, improves your cash flow and gives you the more significant financial freedom to invest in building wealth. You can contact Harris and Partners to learn about consumer proposals and how they could help you. A consumer proposal is an alternative to declaring personal bankruptcy and helps create an agreement with creditors.

Hire brilliant Employees

All rich people who built their wealth from scratch have one thing in common: despite their brilliance, they hire the best minds and hands to handle their business and investments. Whether or not you are brilliant, you need employees with specific traits. As Warren Buffett puts it, you need employees with integrity, intelligence, and energy to get the best results. Of course, you need to show strength and foresight, but ensure you have a solid team working for you. Continue Reading…