Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Late in October, bestselling author and pyschologist Mihaly Csikszentmihalyi passed away in California at age 87. You can read the obituary in the Washington Post here.

Czikszentmihalyi — pronounced “chick-SENT-me-high” — was a university professor who built a mini empire around the nebulous concept of Flow. See this Wikipedia entry for more on his life and work.

As noted in the earlier reviews, I’m intrigued by the concept of Flow as it applies to Encore Careers and life after corporate employment. As many blogs in the Hub’s Victory Lap section have pointed out, aging baby boomers still have a potentially long and creative period ahead of them that lies between the traditional career and what used to be called Retirement.

So it seems to me that if late-bloomer Boomerpreneurs are going to make a success of this new stage of life, they’d better tap into the concept of Flow. It’s all tied in with passion and mastery, which is why I went to the well one last time with Czikszentmihalyi.

Portfolio Manager, Director of Credit Research, Franklin Bissett Investment Management

(Sponsor Content)

The phrase “hunt for yield” is by now a well-worn cliché among fixed income investors. Persistently low yields have led many investors to take on additional risk, and some have considered abandoning fixed income altogether.

We think this is a mistake. Even amid fluctuating yields, inflation jitters and pandemic-driven economic upheaval, fixed income can help maintain stability and preserve capital: if you know where to look.

Why Short-term now

For increasing numbers of investors, the short end of the yield curve is the place to be in the current environment. Short-term rates reflect central bank policy actions. Since the pandemic first took hold early in 2020, central banks have taken extraordinary measures to keep liquidity pumping into the marketplace, all without raising rates. Both the Bank of Canada and the U.S. Federal Reserve have so far left their overnight lending rates unchanged and have indicated their intent to continue along this path well into next year, and possibly longer. This predictability has stabilized, or anchored, short-term rates. In contrast, longer maturities have been prone to volatility as the stop-and-go nature of the pandemic has influenced economic reopening, inflation expectations and financial markets.

Franklin Bissett Short Duration Bond Fund is active in short-term maturities, with an average duration of 2-3 years. About 30% of the portfolio is held in federal and provincial bonds; most of the remaining 70% is invested in investment-grade corporate bonds.

Beyond stability, investments need to make money for investors. In this fund, duration and corporate credit are important sources for generating returns. Historically, the fund has provided investors with better returns than the FTSE Canada Short Term Bond Index1 or money market funds, and with comparatively little volatility.

In It for the Duration

Duration is a measure of a bond’s sensitivity to interest rate movements. Imagine the yield curve as a diving board, with the front end of the curve, where short-term rates reside, anchored to the platform. Like a diver’s body weight, pandemic-driven economic forces have placed increasing pressure further out along the curve. The greatest movement ― expressed as volatility ― has been at the long end, especially in 30-year government bonds. Currently, the fund has no exposure to these bonds.

Cushioned by Corporates

Corporate debt provides a cushion against interest rate volatility, and a portfolio that includes carefully selected corporate securities as well as government debt can therefore be a bit more protective. In addition, the spread between corporate and government bonds can provide excess returns.

We believe it is not unreasonable to anticipate stronger Canadian economic and corporate fundamentals in 2021 and 2022, as well as continued demand for bonds from yield-hungry international investors. These conditions support a continuation of the current trend of a slow grind tighter in spreads, with higher-risk (BBB-rated) credits outperforming safer (A and AA-rated) credits.

Credit Quality is Fundamental

In keeping with Franklin Bissett’s active management style, in-house fundamental credit analysis is a key element of our investment process for the fund. Unless we are amply compensated for both credit and liquidity risk (particularly in the growing BBB space), at this stage of the economic cycle we prefer higher-quality credit. We look for strong balance sheets, good management teams, excellent liquidity, clear business strategy and larger, more liquid issues. Continue Reading…

A couple of recent surveys from J.P. Morgan Asset Management and RBC shed a fair bit of light into recent Retirement trends in North America in the wake of the ongoing Covid-19 pandemic. Summarized in the October 2021 issue of Gordon Wiebe’s The Capital Partner newsletter, here are the highlights:

First up was J.P. Morgan on August 19 in a study focused on de-risking for investors approaching retirement and about to draw down on Retirement accounts.

The study was quite comprehensive, drawing on a data base of 23 million 401(k) and IRA accounts and 31,000 Americans. 401(k)s and IRAs are similar to Canada’s RRSPs and RRIFs.

De-risking is quite common, with 75% of retirees reducing equity exposure after “rolling over” their assets from a 401(k) to an IRA. These retirees also relied in the mandatory minimum withdrawal amounts.

Of those studied, 30% received either pension or annuity income, and the median value of Retirement accounts was US$110,000. The median investable assets were roughly US$300,000 to US$350,000, with the difference coming from holdings in non-registered accounts.

Not surprisingly, the most common retirement age was between 65 and 70 and the most common age for commencing the receipt of Social Security benefits was 66. (Coincidentally, the same age Yours Truly started receiving CPP in Canada.)

The report warns that retirees who wait until the rollover date to “de-risk” or rebalance portfolios needlessly expose themselves to market volatility and potential losses: they should consider rebalancing well before the obligatory withdrawal at age 71.

The newsletter observes that 61-year-olds represent the peak year of baby boomers in Canada and cautions that if they all retire and de-risk en masse, “Canadian equity markets will likely undergo increased downward pressure and volatility. Retirees should consider re-balancing or ‘annualizing’ while markets are fully valued and prior to an increase in capital gains or interest rates.”

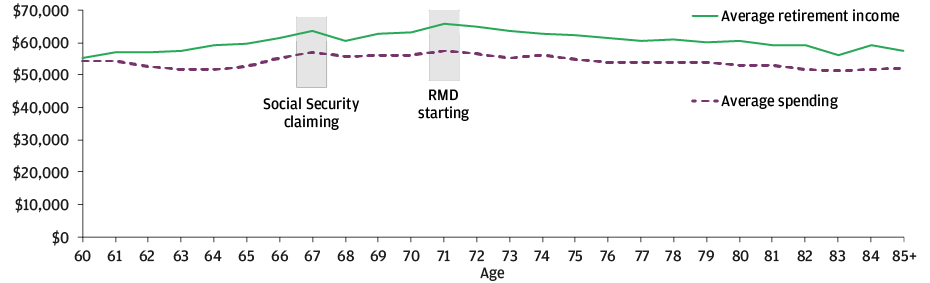

The report includes several interesting graphs, which you can find by clicking to the link above. The graph below is one example, which shows average spending (dotted pink line) versus average retirement income (solid green line.) RMD stands for Required Minimum Distributions for IRAs, which is the equivalent of Canada’s minimum annual RRIF withdrawals after age 71.

EXHIBIT 4: AVERAGE RETIREMENT INCOME AND SPENDING BY AGES Source: “In Data There Is Truth: Understanding How Households Actually Support Spending in Retirement,” Employee Benefit Research Institute & J.P. Morgan Asset Management.

RBC poll on pandemic impacts on Retirement and timing

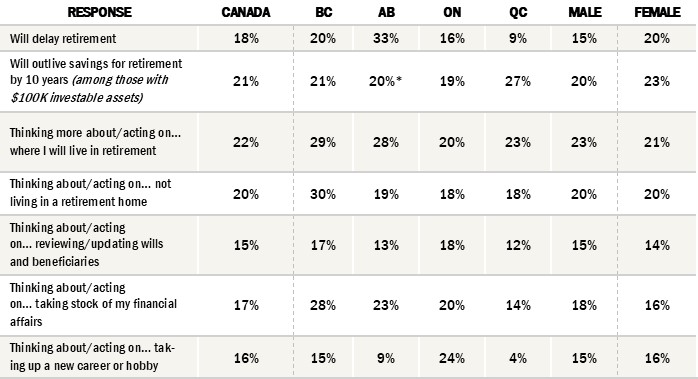

Meanwhile in late August, RBC released a poll titled Retirement: Myths & Realities. The survey sampled Canadians 50 or over and found that the Covid-19 pandemic has caused some Canadians to “hit the pause button on their retirement date.” 18% say they expect to retire later than expected, especially Albertans, where 33% expect to delay it.

They are also more worried about outliving their money, with 21% of those with at least C$100,000 in investible assets expecting to outlive their savings by 10 years. That’s the most in a decade: the percentage was just 16% in 2010.

Sadly, 50% do not yet have a financial plan and only 20% have created a final plan with an advisor or financial planner.

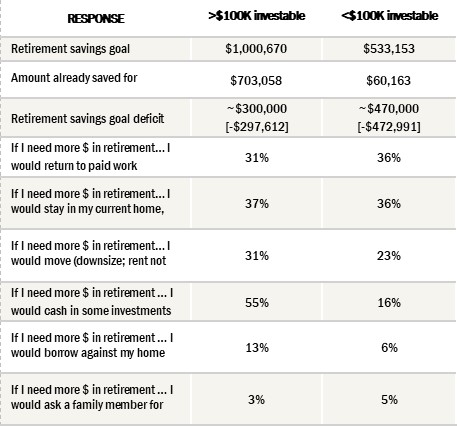

Those near retirement are also resetting their retirement goals. Those with at least $100,000 in investable assets now estimate they will need to save $1 million on average, or $50,000 more than in 2019. 75% are falling short of their goal by almost $300,000 on average.

Those with less than $100,000 have lowered their retirement savings goal to $533,153 from $574,354 in 2019, and the savings gap is a hefty $472,994.

To bridge the shortfall, 37% of those with more than $100K plan stay in their current home and live more frugally, compared to 36% of those with under $100K. 31% and 36% respectively plan to return to paid work, 31% and 23% plan to downsize or move, and 3 and 5% respectively intend to ask a family member for financial assistance.

What is one way you are capitalizing on low-interest rates?

To help you take advantage of low interest rates, we asked seven finance experts and business leaders this question for their best insights. From refinancing existing debts to looking into preferred securities, there are several suggestions that may help you benefit from the low interest rates in the current market.

Here are seven tips for capitalizing on low-interest rates:

Work with a Finance Broker

Get into Commercial Real Estate

Refinance Existing Debts

Consider FHA Loans

Maximize your Return on Investment

Set up a Line of Credit

Look into Preferred Securities

Work with a Finance Broker

As a commercial finance broker, we work with our clients to make sure they can take advantage of low interest rates based on a thorough financial analysis of their company. By analyzing your credit and financial health, we act as an advisor to clients for the best financing options available. We also build leases and loans that are competitively priced and intelligently structured for an optimal plan that works for the client and incorporates the best rates possible. — Carey Wilbur, Charter Capital

Get into Commercial Real Estate

If you’ve been wondering whether or not to buy commercial real estate, I think it is time to take advantage of the “perfect storm” of low borrowing rates. You’ll save a lot of money on interest payments long term. Now is the perfect moment to acquire real estate for assets as an income-generating resource. So whether you need a warehouse, brick-and-mortar store outlet, or even commercial property to place on the rental market, this might be one of the best times to get in the market. Renting your commercial property will provide you with consistent income, and you might also benefit from tax advantages on depreciation and capital gains, to name a few. — Allan J. Switalski, AVANA Capital

Refinance Existing Debts

I suggest you consider refinancing your small business loan, mortgage, or student debt, which entails paying off your existing loan by taking out a new one. The new loan will have a reduced interest rate. Ideally, opt for a fixed-rate loan to lock in the lower rate. To qualify, you’ll need strong credit, but if you do, you’ll save a lot of money on interest fees. — Sundip Patel, LendThrive

Consider FHA Loans

FHA Loans are a great low-interest lending option that is offered by the Federal Housing Administration. These loans are intended to increase homeownership access to those who may not have the ideal credit score required by other financing options. This can be a great option for prospective real estate investors. — Than Merrill,FortuneBuilders

Maximize your Return on Investment

When interest rates are low, borrowing is much more convenient. Continue Reading…

By Don Ludlow, Vice President, Small Business, Strategy & Partnerships and Business Financial Services, RBC

(Sponsor content)

While the COVID-19 pandemic brought significant challenges and uncertainty to small businesses across Canada, it also became a catalyst for many new business practices.

In many ways, it also accelerated the need for small business owners to adapt to other trends and consumer expectations that were steadily on the rise over the last several years.

To help us better understand these trends, RBC recently conducted research to gauge the types of experiences and expectations Canadians have when interacting with small businesses in the coming year as we continue to navigate the ongoing pandemic and journey toward economic recovery.

The survey revealed three important trends that will continue to impact small businesses in the year ahead:

First, we’ll see a growing demand for digital payment and engagement options, whether customers are connecting with small businesses in person or online.

While eCommerce and digital solutions were already on the rise pre-pandemic, they became pandemic necessities as businesses adapted to health and safety measures.

Now, more Canadians are expecting this to be the new way of doing business, with two-thirds (64%) of Canadians saying that partnering with digital platforms to make products and services more accessible will be important post-pandemic, especially among millennials (72%).

Meanwhile, four in five Canadians polled say that they would like to continue to shop online at small businesses, even after the economy is fully reopened, and 72% say that increased social media presence helped them become more aware of what small and local businesses had to offer.

Small businesses that focus on prioritizing employee wellness and overall customer health & safety will be greatly valued by Canadians.

The majority of Canadian respondents in our poll said providing more wellness and mental health benefits and resources to employees will be important going forward (87%).

They also expect heightened hygiene standards to continue post-pandemic (99%) and would like businesses to continue offering flexible curbside pickup and delivery services (78%).

As a result, offering employee benefits, resources and safety protocols that meet these expectations will be critical differentiators for small businesses looking to attract and retain talent and customers.

We’ll continue to see a rise in socially and locally conscious consumers – especially among millennials and Gen Z.

Supporting small, local, and diversity-focused businesses is here to stay post-pandemic. According to our research, the majority of Canadians (77%) polled plan to spend more at small, local retail stores, restaurants and businesses to support their recovery than they did before the pandemic.

Many respondents also said they are actively seeking out and supporting 2SLGBTQ+* (52%) and BIPOC **(61%)-owned businesses, products and services. These numbers are greater among Millennials and Gen Z, indicating the next generation of consumers will increasingly purchase through a diversity-focused lens.

Being aware of these trends, and adapting business strategies and operational practices to address evolving consumer expectations will be important to the success of small business owners in the next year.

In light of these insights, we have three tips for entrepreneurs to consider as part of their 2022 playbook for success.Continue Reading…