We review books that deal with everything from financial independence topics to politics, and anything in between. We may sometimes stray into films and music if there is a “Findependence” angle.

Last week we witnessed another entry into the Canadian Asset Allocation One Ticket Portfolio Solutions.

Welcome BMO.

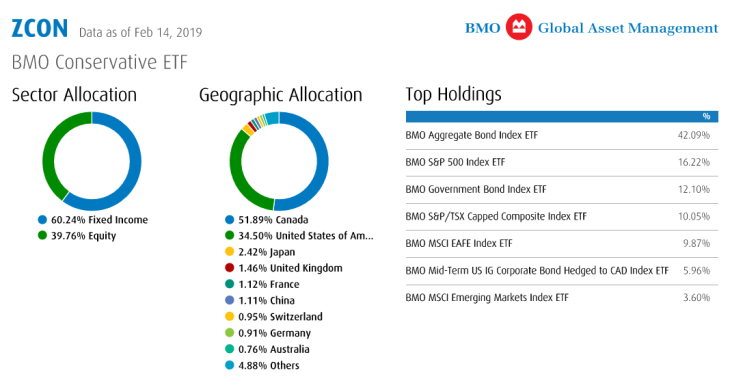

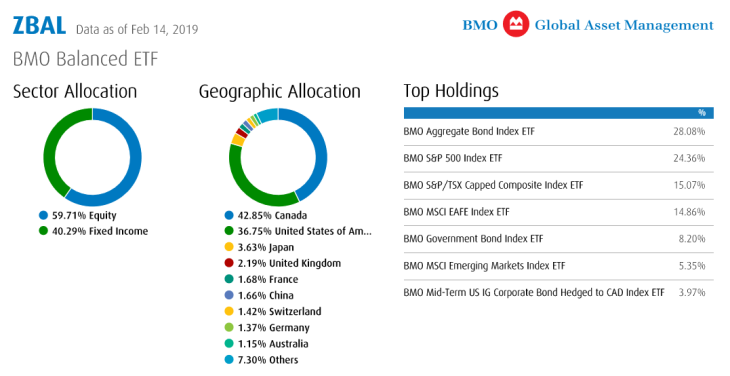

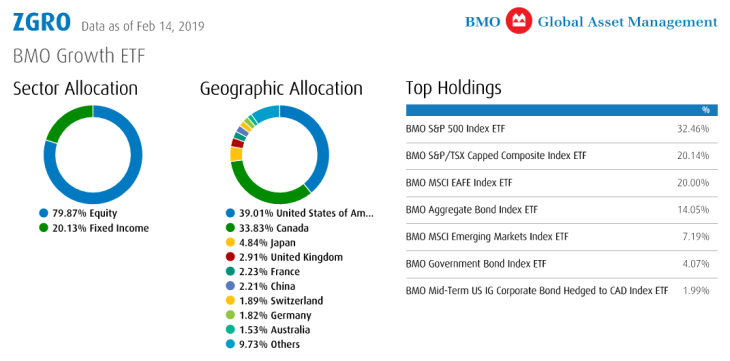

On Friday February 15th BMO launched three asset allocation portfolios by way of the Conservative ZCON, the Balanced ZBAL and the Growth ZGRO.

Here is the overview from the Fact Sheets:

Wonderfully simple or plain vanilla?

Take your pick. These are certainly plain vanilla, they’re not even Lemon Raspberry White Chocolate. But they’re still wonderful.

I am certainly surprised that BMO Global Asset Management kept the portfolios so clean and simple. As you may remember from my review of the BMO SmartFolio. the Robo Portfolios are actively managed. That is to say there is active asset allocation with respect to the core and smart beta ETFs. From my BMO SmartFolio review …

The portfolios will be rebalanced every 2 to 6 months. And back to that human touch, the management team with also make adjustments to that asset mix based on market conditions. They may be more active in periods of market turmoil compared to the current market conditions where we are mostly cruising to the upside for Canadian, US and International stocks. Continue Reading…

My latest MoneySense Retired Money column looks at a financial planning software platform called Viviplan. You can find the full article by clicking on the highlighted text: What I learned by putting Viviplan to the test.

Viviplan is the third retirement planning package I’ve tested this year, perhaps — as the MoneySense article reveals — the topic is getting all too real for me now that my wife, Ruth, has told her employer she plans to retire when she turns 65 next summer. I’m a year older and have been somewhere between self-employed and semi-retired for most of my 60s.

All these packages deserve consideration and work in more or less similar fashion. To do the job justice, you need to have handy — or at least summary information — such documents as your latest tax returns, brokerage statements, Service Canada CPP and/or OAS projections, as well as having a good grasp of your regular and occasional monthly expenses.

Having most recently performed this exercise with Viviplan — and as one of the users we interviewed for MoneySense relates — it can be a bit scary to see in black and white just how expensive daily living can be. The package won’t let you forget any tiny expense, from pet food to boarding your pet when you’re on vacation (or arranging to hire a neighbour’s teenager, which is what we do if we go away and must leave our cat behind.)

Viviplan calls itself a Robo Planner

Viviplan — which has been dubbed “Canada’s Robo Planner” — is the brainchild of financial planner Rona Birenbaum. Birenbaum also runs a separate fee-for-service financial planning firm called Caring for Clients. I have consulted her for various pieces in the past, particularly about annuities.

Indeed, when I was putting Viviplan through its paces, one of the big questions I had was whether there was a need for us to partly annuitize, seeing as Ruth has no employer-provided Defined Benefit pension at all (just a hefty RRSP), and I have only two modest DB pensions that are not inflation-indexed.

Viviplan’s Morgan Ulmer

Our main question was whether to make up for this lack of employer pensions by at least partially annuitizing, or what Moshe Milevsky and Alexandra McQueen call in the title of their book Pensionize Your Nest Egg. Another author, Fred Vettese in Retirement Income for Life, was in a similar situation when he reached 65 (the same month as I did) and had suggested annuitizing 30% of his nest egg at 65 and doing another 30% at age 75 (assuming CPP at 70). Our question for Viviplan was whether this would make sense for us too, or just for Ruth.

We went back and forth with Calgary-based certified financial planner and product manager Morgan Ulmer (pictured to the right). As she relates in the MoneySense piece, “it’s certainly not necessary,” since at today’s interest rates, Viviplan told her that for us a pure GIC portfolio could get us to where we want to go, with the virtue of more financial flexibility and higher final estate value. Like the other programs, Viviplan recommends delaying CPP till 70 and OAS too if possible.

Annuitize? No wrong decisions and no rush

Partial annuitization for Ruth along the lines of what Vettese suggests would result in a slightly lower estate for our daughter. “With annuities, you are making a choice between legacy and flexibility versus security and longevity protection,” Ulmer said in the plan’s written recommendations, “There are no wrong decisions here, and there is also no rush.” Continue Reading…

The Globe & Mail newspaper has just published a column by me describing our family’s experience with three Canadian retirement planning programs available to consumers. You can find the full article by clicking on the highlighted headline here: Three online programs to help plan out your finances in Retirement.

These programs vary in price from $85 to more than $800 but just a single insight from any one of them will likely recap the modest fees. I found all three (or four actually) quite useful, seeing as I have already turned 65 and my wife Ruth will follow suit next summer, at which point she too will abandon full-time employment for the kind of semi-retirement or financial independence that this website focuses on.

Some of the planning packages are designed for financial advisors to work with their clients but all can be obtained by individual consumers. They are all strong on the financial side and the first step with any of them is to enter data into your personal computer (PC or Mac, or any device via the cloud). You’ll need your brokerage statements, pension benefits statements if any, tax returns and a good grip on your monthly expenses, which means credit-card and bank statements, and maybe charitable contributions and any other regular expenses not gathered by the foregoing.

Just as important, you need to have at least a rough picture of what your future golden years will be spent doing once you’re no longer tethered to full-time employment.

Decumulation can be more challenging that Wealth Accumulation

All these programs are good at projecting your future retirement income and taxes, factoring in the many moving parts of CPP payments, OAS clawbacks and the other minutae that make the “Decumulation” phase of retirement planning perhaps even more challenging than what the long Wealth accumulation process was. As Retirement Navigator creator Doug Dahmer (a regular contributor to the Hub) often says, tax is perhaps the single biggest expense in Retirement.

There’s an art to deciding which income sources to drawn down upon first (registered, TFSAs, non-registered), or to deciding whether to defer corporate or government pensions till 70, while drawing on savings in the meantime.

But it’s not just about money: these programs help you identify how you’ll navigate the three major phases of retirement: the early “go-go” years where you may indulge in expensive travel and other hobbies; the “slow-go” years where you pull in your oars a bit and stick closer to home; and finally the “no-go” years where one or both members of a couple start to confront their mortality and deal with rising healthcare costs and perhaps a shift into a retirement or assisted living facility.

Here’s the capsule summary of the strengths and weaknesses of each. The highlighted text in Red will take you to the respective websites: Continue Reading…

Talk about strange timing! Last weekend, right before this week’s sharp market sell-off, the Motley Fool Money podcast featured an interview with Howard Marks, the influential money manager at Oaktree Capital. Marks has just released his second book, Mastering the Market Cycle, which I promptly bought and downloaded on Kindle and read over the (Canadian) Thanksgiving weekend.

Maybe a little, it turns out, although at the time of that podcast Marks’ mood was one of “cautious optimism.” Since then the market seems to have shifted a bit more from optimism to caution. As it happens, Wednesday’s 800-plus plunge in the Dow occurred just two days after I personally started to rebalance our portfolios, partly inspired by my weekend reading, so the new book was quite relevant.

Book publishing being what it is, and with much of it largely written in 2017, Marks doesn’t come right out and declare that the market is near a top; authors tend to be aware that books need to stand up for a few years. However, a quick look at his web-based market commentaries underline his cautious approach. As Hill pointed out in his conversation with Tim Hanson, Marks’ memos may not be quite as well known as Warren Buffett’s, but he nevertheless has a strong following.

At age 72, Marks has seen more than his share of market cycles and claims to have been able to profit from most of the biggies: from the 1999 Tech Wreck to the 2007 Global Financial Crisis. In fact, he’s been around long enough to remember the famous Nifty 50, which were perhaps analogous to today’s mania for FANG stocks. Continue Reading…

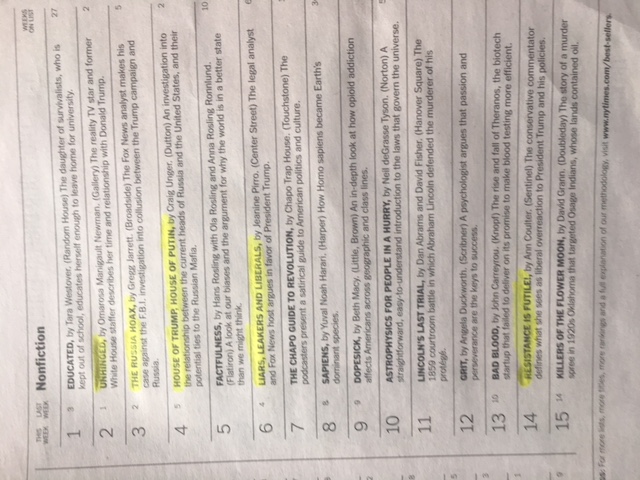

As the yellow highlights show, books about Donald Trump now dominate the New York Times’ non-fiction bestseller lists

As my latest MoneySense Retired Money column recaps in depth, roughly half of the top ten New York Times bestselling non-fiction books are about the Donald Trump presidency. You can access the full column by clicking on the highlighted headline here: How Trump’s policies are affecting my investment choices.

Soon after the 2016 election that brought Trump to power, my financial advisor and I would exchange emails about the latest books: initially biographies and warnings and then in the last year the current glut of books about the actual presidency and the administration.

I’m normally a fan of biographies and love him or hate him, it’s hard to ignore the life of Donald Trump, considering that everything he says or tweets can impact us all. Yes, he may or may not be a threat to the looming Retirement of the baby boom generation of which he is on the leading edge, but his hair-trigger temper and proximity to the nuclear codes gives us something more to fear than merely our financial survival.

Some of the books I mention do give some insights into the implications of this presidency for the global economy and stock markets. Others are mere political diatribes from the left or the right, while still others are more salacious tell-alls. Stormy Daniels, I’m looking at you! (The book is titled Full Disclosure.)

As the column mentions, there are a number of books written by rabid left-wingers who are convinced Trump is a serial liar and a treasonous sellout to Russia president Vladimir Putin, but there are also several written by conservatives and republicans who are more sanguine about it all. In the latter camp I’d include Conrad Black, Ann Coulter and David Frum, plus a few titles from FOX news personalities who are obviously sympathetic with “The President,” as they like to refer to him.