By Savannah Wardle

Special to the Financial Independence Hub

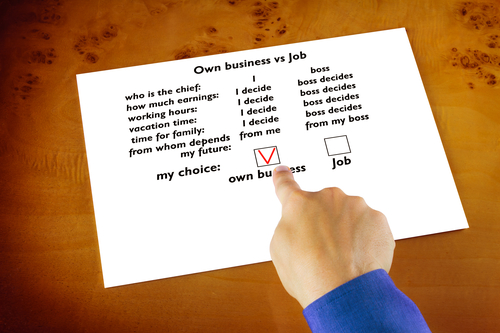

Instead of getting a job, make a job. You can take a large vacant place where a business should have been and fill it with everything you’ve ever dreamed of. If you’re on the verge of a major career change, you have the unique ability to customize that change to your needs. It might be time for you to branch out on your own and do things for yourself: you can wind up better off for having done it.

It’s easier than it used to be

The internet revolutionized the way that people run businesses. It used to be that people were confined to working for someone else because they didn’t have the resources they needed to become fully independent. Now, almost everything you can’t do yourself can easily be outsourced to software, apps, or freelancers who know how to get things done the right way. It doesn’t matter if you need to hire a Twitter expert, have a catering website built, or find specialty garage door software. The internet has it, and you can use it to build your own empire.

You’re free to explore Innovation and Creativity

Think about all the aspects of your old job that were holding you back. Did you have bold new ideas that you were dissuaded from pursuing because they didn’t adhere to the company’s “play it safe” motto? You don’t have to worry about that anymore. You’re the one calling the shots, and if you know you have the potential to shake up your industry, no one is stopping you. You can try and try and try, even if you fail, and you don’t need to worry about the powers that be restricting you from exploration.

You can live the way you want

If you used to work long hours and weekends, you probably felt like you were missing out on life. If you run your own business, you can be open from 9 to 5 on weekdays. Close up shop for dinner and the weekends and live your life. A lot of people cite work/life balance as being one of the reasons they opt for a career change, and if you’re one of those people, you can easily find the exact balance you want by becoming an entrepreneur or an independent contractor.

You get to build your dream team Continue Reading…