Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

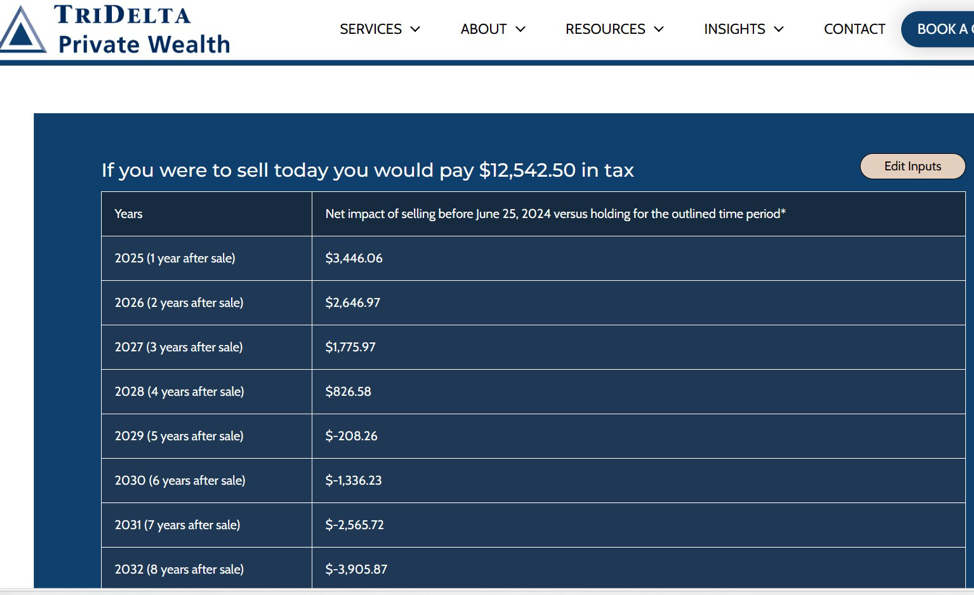

As you may know, the recent Federal Budget announcement had a few important changes that can have an impact for some, but certainly not all. The most discussed has been the increase to the capital gains tax.

The most directly impacted are those with investments in a Corporation or a Trust. Not only will they face an increase in taxes on every dollar of capital gains (not just after $250,000 as it is on personal accounts), but this is forcing some important near term decision making.

For many people in this situation, the question for investments with unrealized capital gains is whether to hold those securities longer term or sell them prior to June 25th to avoid the new higher tax rate.

To help with that choice, we have just launched a new calculator aimed at this group.

It is free for anyone to access. They don’t have to provide any details.

Interesting headline and catchy, but we know stocks for the long-run can work for long investing periods. Otherwise, nobody would take on this form of investing risk for any reward…

That said, Swedroe does raise a few interesting factoids from his reference in the article about stocks in the long-run:

“Over the 150 years from 1792 to 1941, the performance of stocks and bonds produced about the same wealth accumulation by 1942.”

AND

“Results for the entire 227 years were weakly supportive of Stocks for the Long Run: The odds that stocks outperformed bonds increased as the holding period lengthened from one to 50 years. However, the odds never got much higher than two in three and increased only slowly as the holding period stretched from five years (62%) to 50 years (68%).”

The problem I have with such information, while interesting, is our modern economy is fundamentally different than 1942, let alone 1842, or 1792. I simply don’t see the value or point in referencing any stock market data that goes back 200+ years for the modern retail investor.

But I do agree with Larry in that stocks may not always beat bonds, at least over short or modest investing periods. I have participated in a bit of a “lost decade” in my own DIY investing past.

It could happen again.

Looking back at a broad measure of the U.S. stock market, such as the S&P 500 index, over the past 20 years, you would see (or experience as an investor) very different results from the first decade (2000-2009) and the second (2010–2019).

In fact, for large-cap U.S. stocks in particular, this “lost decade” from January 2000 through December 2009 resulted in very disappointing returns: an index that had historically averaged more than 10% annualized returns before 2000, instead delivered less-than-average returns from the start of the decade to the end. Annualized returns for the S&P 500 (CAD) during the market period were -3.18%.

Of course, we only know the results of stocks in hindsight after bad market periods are over and preferably for me, a few generations back makes sense to measure some relative stock market history vs. going back to horses and buggies in the form of a few hundred years…

What do I think? Is 100% equities investing at your peril?

No.

I remain invested in mostly equities at the time of this post with conviction although I do keep cash (or more recently cash equivalents on hand) and always have to some degree. Continue Reading…

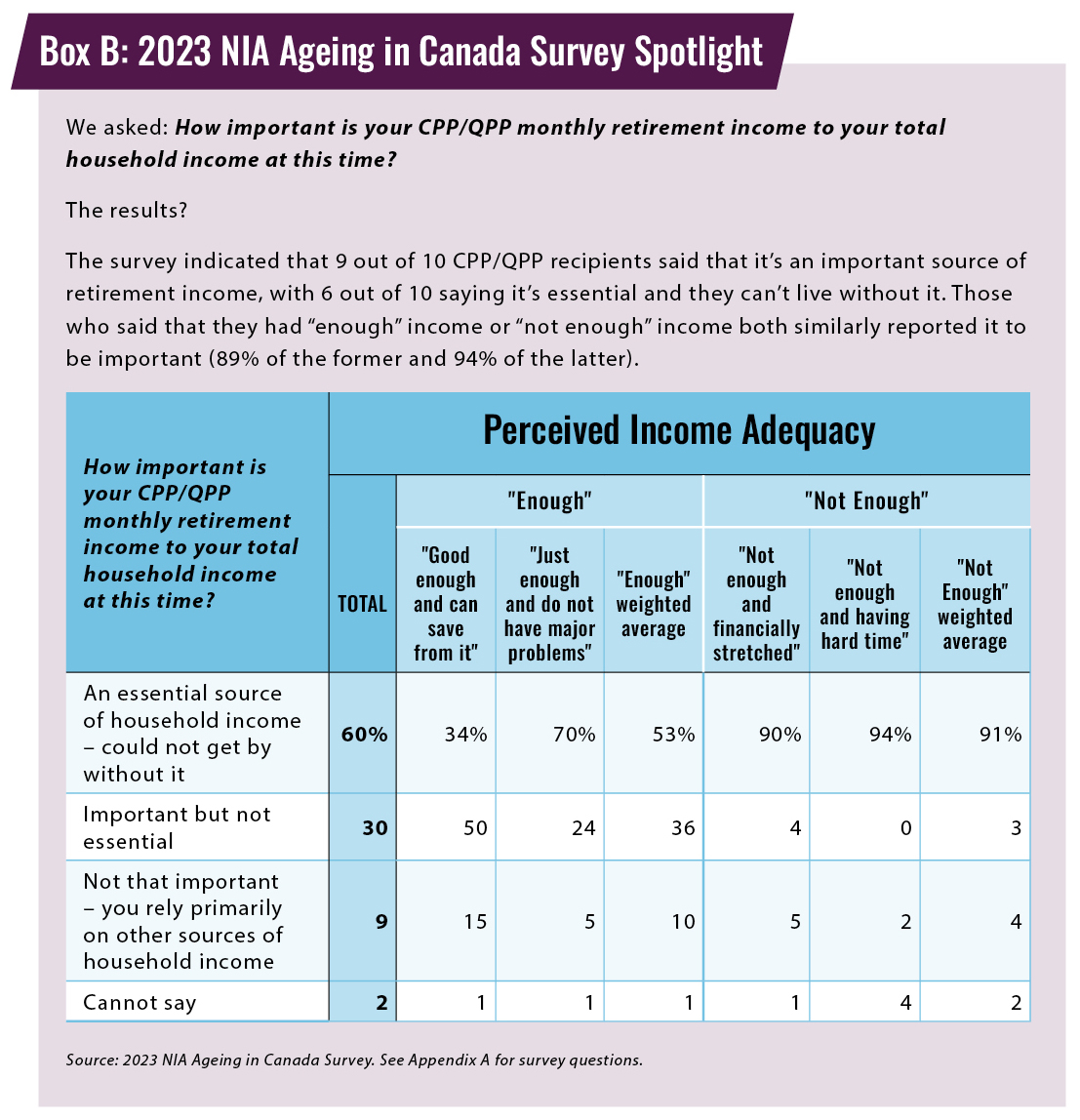

My latest MoneySense Retired Money looks in more detail at the National Institute of Ageing’s recent series of papers on CPP (and OAS). As the Hub reported on April 11th, few Canadians are aware that delaying CPP benefits to age 70 can more than double (2.2 times actually) eventual monthly benefits compared to taking it early at age 60. That blog reproduced a chart from the NIA that showed just how much money Canadians are leaving on the table by NOT deferring benefits as long as possible.

The other major chart from the NIA paper is reproduced above, showing just how important most retirees view the guaranteed inflation-indexed income that CPP and OAS provide. As the new column points out, for many retirees — especially those who worked most of their careers in the private sector and don’t enjoy a Defined Benefit employer pension — CPP and OAS are the closest thing they’ll have to a guaranteed-for-life inflation-indexed annuity.

The new MoneySense column focuses on how delayed CPP benefits not only generate higher absolute amounts of income but also carry with it the important related benefits of more longevity insurance and inflation protection.

It features input from several well-known retirement experts, including noted finance professor and author Dr. Moshe Milvevsky, retired Mercer actuary Malcolm Hamilton, author and semi-retired actuary Fred Vettese, TriDelta Senior Financial Planner Matthew Ardrey and the lead author of the NIA report, Bonnie Jean MacDonald.

Delaying CPP is “the best annuity-buying strategy you can implement.”

Milevsky sums it up well, when he says “delaying CPP is the best ‘annuity-buying strategy’ you can implement. Everything else is just Plan B.” Audrey makes a similar point: CPP is “an annuity and an indexed annuity at that … This helps protect the purchasing power of this income stream through retirement. Many people wish they had an indexed DB [defined benefit] pension and in fact we all do. It is the CPP.”

You’ll probably see much more press on this topic as the NIA is releasing a paper each month between May and December. May 8th will be general education on the Canadian retirement income system while July 17th will explain the mechanics of delaying CPP (and QPP) benefits.

Boating is an adventure at any age, but it often becomes a lifestyle for retirees. If you’ve ever considered trying to save up for a boat one day this could be a good read. With a couple of these financial tips, you’ll be well on your way to living your boating dream!

Adobe Image courtesy Logical Position/Visionsi

By Dan Coconate

Special to Financial Independence Hub

Retirement is a time for relaxation, adventure, and a well-deserved break from the toils of work. For many, it’s the perfect time for ticking off items on the bucket list and enjoying activities they couldn’t do before, such as boating. Setting sail on serene waters has a draw that’s hard to resist, especially once you’ve reached your golden years, but it can unfortunately be an expensive hobby. With these financial tips, investing in a boat for retirement is within reach.

Why Invest in a Boat?

Investing in a boat can offer several benefits depending on your interests as well as your lifestyle. In many cases, the most common reasons as to why one would invest in a boat is for recreation/leisure, family time, and adventure!

In the financial world, large purchases are seldom one-dimensional. However, they can be gateways to new experiences or investment opportunities. A boat, with its allure of freedom and tranquility, often blinds potential owners to its financial complexities. With a good understanding of your needs and what’s available, you can spend your glory days in luxury and comfort.

Don’t forget that investing in a boat depends greatly on the individual themselves and what they are comfortable in affording. As great as it is to own one, you don’t want it to feel like you’re being submerged by a financial burden especially towards your later years in life. Find something that you can truly afford and go from there.

Understanding the Cost of Ownership

As mentioned above, owning a boat depends greatly on the individual themself and what they can afford. The financial commitments of boat ownership extend far beyond the initial purchase price. From understanding the dos and don’ts of marine craft maintenance to preparing your vessel for foul weather, upkeep can turn the investment into a bottomless expense if not managed wisely.

Here are some common costs that every prospective boat owner should consider:

Purchase Price: The upfront cost varies widely based on the boat’s type and age.

Maintenance and Repairs: Regular upkeep, including engine maintenance, hull cleaning, and repairs.

Docking Fees: Charges for mooring or storing your boat at a marina or docking facility.

Insurance: Protection against accidents, theft, and natural disasters.

Fuel: Operational expense that can fluctuate with usage and fuel market prices.

Safety Equipment: Initial purchase and replacement costs for items such as life jackets, fire extinguishers, and flares.

Understanding these costs is imperative, as they can tally up faster than the wakes behind a speedboat.

Legal and Financial Considerations

There are also key legal and tax-based implications of boat ownership. When considering the various forms of state and federal taxes on a boat’s purchase, operation, and potential resale, the financial burden can become relatively heavy. Annual or biennial fees can add up and make it difficult to ascertain the full price of boat ownership beforehand. Continue Reading…

Since the beginning of the year, Canadians saw the Bank of Canada maintain the overnight rate at 5.00% as inflation eased to be less than the upper end of the Bank of Canada’s inflation-control target of 3%.

Amidst this economic backdrop, Canadians who participate in defined benefit (DB) pension plans may be interested in the financial health of their DB plans.

The Mercer Pension Health Pulse (MPHP) is a measure that tracks the median solvency ratio of the defined benefit (DB) pension plans in Mercer’s pension database. At March 29, 2024 the MPHP closed out the year at 118%, an improvement over the quarter from 116% as at December 31, 2023. The solvency ratio is one measure of the financial health of a pension plan.

Throughout Q1, most plans saw positive asset returns coupled with decreased DB liabilities, which resulted in an overall strengthening of solvency ratios. In addition, compared to the beginning of the year, there are more DB pension plans with solvency ratios above 100%.

In other words, Canadians who participate in DB plans are likely to have seen the financial health of their DB pension plans improve over Q1.

Inflation in Canada and interest rates

Canadian inflation eased to 2.9% in January, which is less than the upper end of the Bank of Canada’s inflation-control target of 3%. It is the Bank of Canada’s expectation for inflation to remain close to 3% during the first half of 2024 before gradually easing. On March 6, the Bank of Canada continued its policy of quantitative tightening by maintaining the overnight rate at 5.00%. On March 19, Canadian inflation for February 2024 came in at 2.8%, which ignited industry speculation on the timing and amount of a cut to the overnight rate.

In addition, on April 10, the Bank of Canada announced that it was maintaining the overnight rate at 5.00%. The next scheduled date for announcing the overnight rate target is June 5, 2024. Continue Reading…