As Didi says in the novel (Findependence Day), “There’s no point climbing the Tower of Wealth when you’re still mired in the basement of debt.” If you owe credit-card debt still charging an usurous 20% per annum, forget about building wealth: focus on eliminating that debt. And once done, focus on paying off your mortgage. As Theo says in the novel, “The foundation of financial independence is a paid-for house.”

Generation Z (Gen Z) is feeling the brunt of economic uncertainty in Canada as they enter the workforce and take on a whole host of financial ‘firsts’ – such as paying rent, saving for a vacation and purchasing groceries. More than any other generation, Gen Z is more likely to feel stressed (42 per cent), anxious (37 per cent), and overwhelmed (31 per cent), according to new research from Interac Corp.

Inflation is one of many factors serving as a hurdle for Gen Z and Canadians alike in their ability to stay on top of their money. In fact, 78 per cent of Gen Z respondents agree inflation and everyday essentials (75 per cent) are two external causes throwing a wrench in their ability to manage their finances.

Leaning on Interac Debit and Interac e-Transfer

Canadians will likely continue to contend with inflationary pressures for many months to come and it’s critical they’re equipped with tools that can help them stay in control.

Building healthy money habits such as creating a budget and using your own money are two ways to help navigate personal finances amid the current economic landscape. We’re hearing that Gen Z is doing just that – leaning on debit to take charge of their finances. Gen Z told us they are more likely (70 per cent) to frequently use debit, compared to 55 per cent of non-Gen Z Canadians polled in the Interac survey.

From the survey findings, we discovered that nearly half of Gen Z say they prefer to spend with debit so they’re only spending the money they have. Gen Z also told Interac that they feel more in control of their spending when using debit (46 per cent) and half of this generation of debit users (50 per cent) also say it’s easier to track their spending when using debit versus credit.

While there are many external factors that make it difficult to manage your finances, there are tools to help you stay in control of your day-to-day spending. For example, making Interac Debit the default payment in your mobile wallet or merchant app can help you spend the money you have in your account. Using debit for essential purchases can also help you stay on track and build good financial habits.

Canadians can also take charge of their financial well-being by using Interac e-Transfer to pay instantly or to split costs with others, making shared experiences more affordable and easier to track. This is a trend we began to see last year, as Interac e-Transfer hit one billion transactions. We’re seeing that Gen Z continues to rely on this tool, with nearly eight in ten (78 per cent) saying Interac e-Transfer is the simplest way for them to split costs so they can still get the most out of life and spend the money they have.

Essential spending continues

In times of uncertainty, debit remains an important and empowering tool, helping all generations across Canada stay in charge of their finances. While we’ve seen Canadians react to inflation and shift their spending accordingly, essential spending has continued. Canadians continue to spend the money they actually have in their accounts, as evidenced by year-over-year growth in Interac Debit (5 per cent) and Interac e-Transfer (11 per cent) volumes.

Additionally, year-over-year, Interac transaction data shows an increase in the number of transactions with InteracDebit at grocery stores and supermarkets as average basket sizes have decreased. Continue Reading…

BDO Affordability Index Spring 2023 (CNW Group/BDO Canada LLC)

By Jennifer McCracken, BDO

Special to Financial Independence Hub

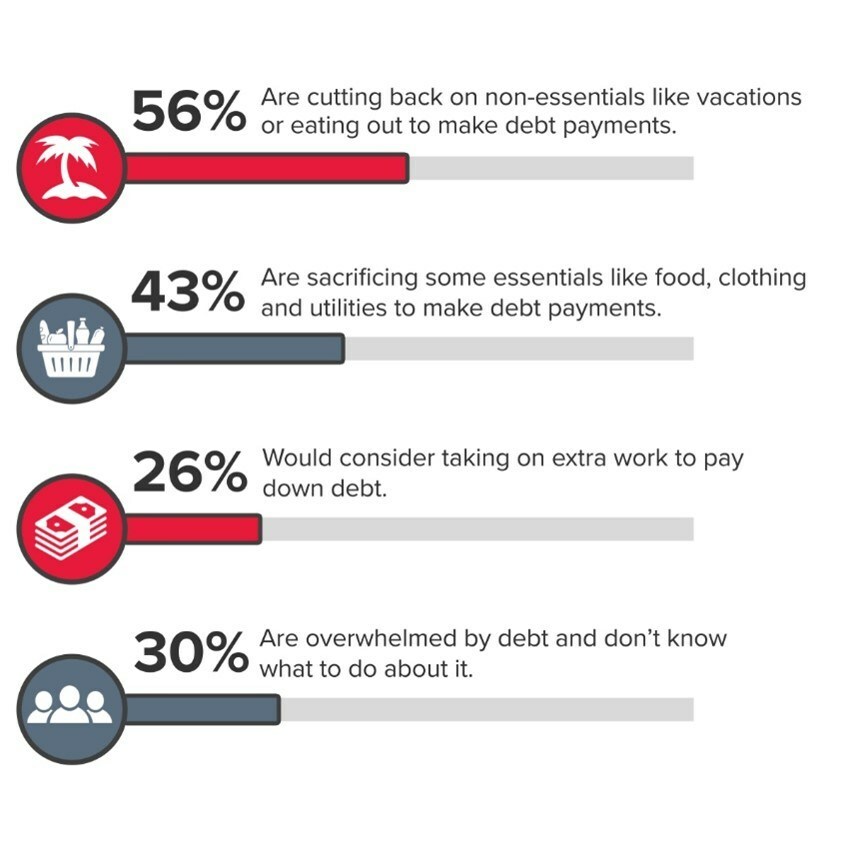

The cost of living has spiked significantly in the past year and Canadians across the country are feeling the pinch. Younger Canadians between the ages of 18 and 34 are particularly affected, having not had the chance to build up as much savings as older generations.

BDO’s newest Affordability Index shows that 45% of young Canadians say their debt load is overwhelming and they’re unsure how to tackle the problem. That’s higher than those between the ages of 35 to 54, where 39% say they’re in that situation and significantly larger than the 13% of Canadians between the ages of 55+ who feel the same.

Credit-card debt appears to be the main reason younger Millennials and Gen Z are falling behind, with 37% of 18-34 year olds saying this form of debt causes them the most stress. Mortgage debt and student debt were the next closest reasons, with 22% for the former and 21% the latter.

What are Canadians doing to cope with inflation and rising debt?

It’s not surprising then that 49% of younger Canadians say they’re reducing their living expenses to cope with inflation and the high cost of living, while 32% say they’re lowering how much they contribute to savings as well.

While younger Canadians may be struggling more than their older counterparts, they’re also more open minded when it comes to finding solutions.

The Affordability Index indicates that younger generations are much more willing to look for new streams of revenue compared to older ones. Some 24% say they are adding part-time work to keep up with inflation, compared to just 13% of 35-54-year-olds and only 5% of those 55 or older.

Young Millennials and Gen Z would also find side hustles and gig work to increase their income. Of those doing this, 35% said it was to help them pay for essentials and 27% say it’s to help them pay down debt.

It’s not just part-time and gig work that younger Canadians are using to fight inflation, they’re also looking for higher paying jobs. A total of 13% say they’ve recently found a new full-time job in response to the affordability crisis. That’s compared to just 7% of those aged between 35-54 and only 1% of those 55 and older.

However, while younger generations are keen to seek out new ways to increase their income, they’re very unfamiliar with many of the most common debt relief options available.

A lot of people just don’t know what their debt relief options are …

Only 19% of them said they were familiar with the idea of bankruptcy, 11% said they know what a debt management plan is and 9% with a debt consolidation loan. Continue Reading…

This is a battle between lower-fee Canadian Robo Advisor portfolios vs high-fee Canadian mutual funds. As you are likely aware, Canadians pay some of the highest investment fees in the world. Larry Bates, the author of Beat The Bank, calls those fees wealth destroyers. Lowering fees is one of the most predictable ways to increase your investment returns. More money stays in the right pocket; your pocket. By way of the Questwealth Portfolios (from Questrade) let’s have a look at the superiority of Robo Advisors over Canadian mutual funds.

There are three simple ways that Canadians can leave behind their advisor and high fee mutual funds. If you want investment advice and managed global ETF portfolios, you can look to one of the Canadian Robo Advisors.

Here is a post on what is a Robo Advisor? As you’re about to discover, this is a far superior approach to a typical high-fee mutual fund. Also consider that most high-fee mutual funds in Canada are offered by salespersons and not ‘real’ advisors.

Questwealth is one of the Canadian Robo Advisors. And don’t be fooled by that Robo word. While you can choose to do everything online from start to finish, real humans are available for investment advice and guidance. And at a shop such as Justwealth you’ll have a dedicated advisor, with financial planning available.

You can have it all in a low-fee environment.

Not investing with Mom and Dad’s guy

Questwealth offers the Questwealth Portfolios. They are the lowest fee Robo offering in Canada. And they are famous for their advertising. Many younger Canadians are not following their Mom and Dad, running into the bank, Investor’s Group or AGF (or other mutual fund sales shop) to fill the pockets of advisors and mutual fund creators. Nope, they are learning how to self-direct and how to take control of their own wealth building destiny.

In one commercial the younger brother turns to his embarrassed older bro and offers …

You’re not still investing with Mom and Dad’s guy, are you?

It’s nice to see many Canadians become their own advisor. Keep that 2% or more in your own pocket. You’ll need bigger pockets, by the way.

Questwealth Portfolios vs Canadian mutual funds

Questrade suggests (based on the simple fee math) that over time Canadians could retire 30% wealthier. That said, it’s a much greater benefit than that 30% suggestion. Based on the return differential to date, you’d be looking at returns that are 50% better (or more) over a 30-year period. Retiring with 50% more is obviously life changing.

And of course, a 5-year performance is a shorter period, but it aligns with the known underperformance of high-fee actively-managed Canadian mutual funds.

Also, past performance does not guarantee future returns.

You’ll find a calculator on their site.

Here’s the Questwealth Portfolios vs typical or average mutual funds in Canada, to the end of February 2023. The mutual fund returns are based on Questrade calculations, looking at the available data for the mutual fund space. That list and returns for the individual mutual funds was also provided to me.

It appears to be a no-brainer: ditch your high-fee Canadian mutual funds. If you decide that a Robo option such as the Questwealth Portfolios is right for you, you’ll find it is an easy process to make the move. They can help you with the transfer process.

But please pay attention to any tax consequences should you have any taxable accounts. You might consider Justwealth if you need to transfer considerable taxable amounts. They can accept your taxable account mutual funds and will drawdown the assets over time in a tax-efficient manner.

Budgeting is hardly exciting, but it’s key to getting finances under control. However, making a budget and sticking to one isn’t always easy. That’s why we could all use some help now and then.

Consider using budgeting and financial planning apps to maintain disciplinary action. Here are the best budgeting apps on the market.

YNAB earns a spot on this list because of its proactive budgeting approach. It offers the ability to sync bank accounts, import data, and manually enter transactions.

Once users sign up, they can create a budget and assign each transaction to a purpose. For instance, they might like to use the app for car payments or mortgages.

The app’s goal is to get users one month ahead. That way, they spend money they earned over a month ago. Essentially, the app gives customers a complete budget overhaul. It also provides users with top security to protect their information and gives them additional resources for staying on track.

This app costs US$98.99 per year or $14.99 per month and offers a 34-day free trial. [All figures below are in US$]

Goodbudget has a free version with ads. Or, users can pay for an ad-free version that costs $7 per month or $60 annually.

Goodbudget is a useful budgeting app that allows users to create and stick to budgets – and keep track of their debt to pay it down faster.

In addition, it helps with money management. That way, users know where their funds are and how they perform.

Users also have easy access to their accounts, as they can use them on the web and on multiple phones. In turn, people can easily share their accounts with others and stay financially connected. This is valuable for some, as it prevents miscommunication and mishaps.

The app also syncs each transaction to the cloud. And some reports show the finances in greater detail – as well as pie charts and other updates to track spending.

Mint is another great budgeting app, as it has high ratings in the App Store and Google Play. It’s also free and syncs with various bank accounts, including checking and savings, loans, credit cards, and more.

Mint works by tracking users’ expenses and placing them within budgeting categories. You might have categories of your own ready to go in a spreadsheet. Mint lets users more fully personalize their categories and set limits to maintain their budgets. Once users approach those limits, Mint will notify them within the app. Continue Reading…

To help you create a budget and stick to it for achieving your financial goals, we’ve gathered advice from 18 professionals, including CEOs, founders, and VPs. From leveraging public accountability to reviewing and adjusting your budget regularly, these experts share their top steps to take for effective budgeting and saving.

Leverage Public Accountability

Negotiate Lower Fees

Celebrate Budgeting Successes

Automate Your Savings

Identify Cost-Cutting Opportunities

Track Expenses and Income

Eliminate Unnecessary Expenses

Create a Realistic Budget

Prioritize Necessary Expenses

Monitor Financial Metrics

Automate Savings Consistently

Use the 50/30/20 Rule

Utilize a Monthly Bill Calendar

Limit Online Shopping Access

Establish a Purpose and Set Goals

Use Cash Stuffing With Discipline

Create Organized Sub-Budgets

Review and Adjust the Budget Regularly

Leverage Public Accountability

In my personal journey toward financial wellness, one of the most effective strategies I’ve employed is leveraging public accountability to create a budget and stick to it. I started by sharing my financial goals with my circle of trusted friends and family, which made the goals feel more real and tangible.

Whenever I felt tempted to stray from my budget, the thought of explaining my overspending to them motivated me to resist. In fact, one time I was really close to buying an expensive gadget on a whim, but the idea of having to admit this unnecessary expense to my accountability partners made me rethink, and I decided against it.

Using public accountability in this way can be a powerful tool to reinforce your commitment to your financial goals, and I encourage you to try it. — Antreas Koutis, Administrative Manager, Financer

Negotiate Lower Fees

One example of a strategy not commonly undertaken when creating a budget is to negotiate lower fees on existing bills such as cable, internet, or cell phone plans.

As the market becomes increasingly competitive, companies are more likely than ever before to reduce customer bills if they know they may otherwise lose that customer’s business.

This can lead to significant savings without having to decrease spending on existing items. With the resulting saved money, you can then allocate it towards your financial goals, more easily allowing for what was once considered unattainable! — Carly Hill, Operations Manager, Virtual Holiday Party

Celebrate Budgeting Successes

Creating a budget and sticking to it, in my opinion, is difficult work. Celebrate your accomplishments along the way. In the long run, I believe that this will make it easier for you to stay on your budget and will help keep you motivated.

Treat yourself to a small reward if you reach a savings goal or pay off a debt, for example. Just make sure the prize is within your financial constraints! — Bruce Mohr, Vice-President, Fair Credit

Automate your Savings

A lot of people tell you to pay yourself first. I think a better approach is to save for yourself first. Set up automatic transfers to your various retirement and savings accounts. That way, the money isn’t just sitting in your checking account and tempting you.

This works even better when you have high-yield savings accounts and retirement funds that aren’t linked to your main bank account. Spending habits are hard to break, but it can be easier to form new ones if you automate your savings. — Temmo Kinoshita, Co-founder, Lindenwood Marketing

Identify Cost-Cutting Opportunities

Of course, the goal of budgeting is to save money, but one step you need to take in order to be successful and reach your financial goals is to look for ways to save. You can do this by reviewing your budget and pinpointing areas where you can cut costs to save money.

For example, if you find that you spend a lot of money on going out to eat, you can cut down spending here and instead cook your meals, which ultimately will be the cheaper alternative.

You may also cancel subscriptions you don’t use or negotiate your bills with your service providers to see if you can get a discount. Overall, there are multiple ways to cut down your spending and save money—you just need to figure out which areas you can negotiate or compromise! — Bill Lyons, CEO, Griffin Funding

Track Expenses and Income

You can find areas where you might be overspending or where you can reduce expenditures by keeping track of your expenses and income. Additionally, you may utilize this data to make wise decisions on future purchases and investments, ensuring that you are deploying your resources as effectively and efficiently as you can.

You may keep yourself motivated and on track to accomplish your goals by routinely evaluating your financial accounts and your progress toward them. Additionally, it can assist you in seeing future difficulties or obstacles, enabling you to modify your plan and change the route as necessary. — Michael Lees, Chief Marketing Officer, EZLease

Eliminate Unnecessary Expenses

A major problem people have when sticking to a budget is the little purchases they make along the way. Many of us are guilty of ordering takeout after a long day of work, picking up a daily Starbucks order, or wasting groceries.

While these small purchases may seem innocent enough, they quickly add up and get you off track toward reaching your financial goals. Before making a purchase, ask yourself, do I need this? Or if you need extra motivation, consider how many hours of work it takes you to purchase these daily items.

By cutting out or at least reducing some of these mundane purchases, you’ll notice your bank account feeling a little healthier and lower stress knowing you have enough money to put towards your financial goals and still pay your bills. — Brandon Brown, CEO, GRIN

Create a Realistic Budget

Often, I see people attempting to budget just for the sake of budgeting without considering its implications on their overall lifestyle. If you want to religiously follow your budget, make it realistic. Realistic financial goals will provide you with a head start in creating an achievable and sustainable budget.

Create a budget that takes into account not only your financial goals but also your lifestyle behavior and the situation you are in right now. If you regularly eat out, set aside money for that based on how much you anticipate spending and how much you are willing to spend.

Moreover, don’t make your spending plan too strict. What’s the purpose of working if you can’t occasionally treat yourself to a sumptuous meal or a new pair of boots? After all, you deserve to feel human.

If you don’t make room for the things you want, you’ll eventually give in and ruin your spending plan. Just make sure to plan ahead and remember that the ultimate goal is financial security and independence. — Jonathan Merry, Founder, Moneyzine

Prioritize Necessary Expenses

Pay all your bills before buying anything discretionary. When you’re trying to save money, it’s essential to cover all necessary expenses before you try setting money aside. This way, you have a better idea of how much money you have left for casual spending and savings.

Paying any obligations first allows you to avoid surprise expenses after you’ve already started spending, which in turn helps you avoid having to pull money out of your savings. The best way to stick to your budget is to pay what you need to first. — Max Ade, CEO, Pickleheads

Monitor Financial Metrics

Entrepreneurs should track financial metrics to monitor their success. A metric for entrepreneurs to measure is customer lifetime value, which is the total amount of revenue that one customer generates during their entire interactions with the business.

Monitoring this metric helps entrepreneurs understand how much revenue can be expected from a single customer and what marketing strategies are most effective at keeping them engaged.

Additionally, tracking customer lifetime value allows entrepreneurs to maximize their returns on investment as they can target customers who spend more money and reward existing customers who have already demonstrated loyalty and commitment. — Julia Kelly, Managing Partner, Rigits

Automate Savings Consistently

Automating savings is a surefire way to help you stick to saving money and reaching your financial goals. Too many situations can thwart your best intentions to regularly add to your savings yourself: mainly forgetfulness since an additional task is the last thing anyone needs.

If you don’t automate, you may rationalize not regularly adding to your savings account because of an extra purchase you think you need or deserve. That could snowball into a pattern of doing it less than you initially wanted or not at all.

“Out of sight, out of mind” is an advantage of automating your savings: If you don’t see that money sitting in your checking account, you won’t spend it.

Disabuse yourself of the notion that you need a large amount of money for an automatic savings plan. Start with $5, $10, or $20 at a time. You can increase that by looking for ways to decrease your expenses, such as comparison shopping for your car and home insurance or requesting lower interest rates on credit cards. — Michelle Robbins, Licensed Insurance Agent, Clearsurance.com

Use the 50/30/20 Rule

To create a budget and stick to it, prioritize your expenses and allocate your income with the 50/30/20 rule. This rule suggests that 50% of your income should go towards necessities like rent, utilities, and groceries, 30% should go towards discretionary spending such as dining out and entertainment, and 20% should go towards saving and paying off debt. Continue Reading…