As Didi says in the novel (Findependence Day), “There’s no point climbing the Tower of Wealth when you’re still mired in the basement of debt.” If you owe credit-card debt still charging an usurous 20% per annum, forget about building wealth: focus on eliminating that debt. And once done, focus on paying off your mortgage. As Theo says in the novel, “The foundation of financial independence is a paid-for house.”

They say that money doesn’t buy happiness. But when funds are tight it sure can feel as though life is a little constrained. You may constantly feel as though you’re missing out on opportunities or fun events.

Learning to live within your means is a hard lesson, but many people who achieve it never feel as though they are going without. In fact, most have found ways to live their lives to the absolute fullest. Sometimes all that is required is a change of perspective or a minor reorientation of values.

It may come as somewhat of a surprise, but having a great and fulfilling life often isn’t tied to how much money you make or the fancy things you’re able to spend it on. Some of the most important things that really make life worth living don’t cost much and many come for free.

Improve Life, Save Money

Entertainment can be one of the draining items on your budget. A couple drinks with co-workers after work one night, going to a show with a gal pal another, maybe paying for tickets to the big game the next. It seems like everything fun costs money and over the course of a week or a month that really adds up.

But not all hobbies have to cost a lot of money, or really any money at all. Rather than grabbing drinks after work, you can invite people over to your house to hang out around the fire pit and have a potluck-style barbeque. Or instead of going to a show with a friend, you strive to attend free local events like music in the park, farmers’ markets, or explore new neighborhoods. Maybe instead of paying for a ticket to the big game, you can invite your friends to a tailgate in the parking lot. Continue Reading…

As a mother, I know the importance of raising my daughter to be independent and confident. One of the most significant ways I can do this is by instilling in her the value of financial literacy. By teaching her to be financially independent, I am setting her up for a future where she can make sound decisions with money and have the freedom to achieve her dreams. I feel every mother should share this responsibility and nurture the financial skills of their children, especially when we consider the uncertainties of the current global economic climate.

Growing up and learning to manage money through lived experiences, I discovered that some of those life lessons can be painful. My immigrant parents were so focused on working hard to provide the basics for the family, financial literacy lessons weren’t really a priority for my sister and me. All we were taught was to save and keep on saving. In fact, my sister and I would sometimes skip lunch at school just to save the allowance our parents gave us. I learned the hard way that while saving is part of being financially literate, it can’t just stop there; a significant next step is to find safe, reliable methods to growing your wealth.

Not knowing better, when I was 18, one of the earliest financial mistakes I made was getting multiple credit cards, which eventually resulted in a lot of debt (because which teenage girl doesn’t like shopping?). I had to work hard to pay it off and it was a tough lesson to learn, but it was valuable because it made me realize the importance of being smart about money from a young age.

After that, I started seeking support to become more financially literate from any source I could get my hands on. The internet was my best friend and I got into the habit of listening to podcasts about investing and best financial practices. When I started working, I was lucky enough to find a trusted mentor who taught me that putting 75 per cent of my paycheque toward smart investments was smarter than spending the money on any big-ticket item immediately.

As I became better with money, I went from only knowing how to save money to growing my wealth through investing in stocks (ETFs) and real estate and having a diverse portfolio. When it comes to investments, I now know it’s important to maintain both passive and aggressive investments. Having said that, choosing between good investments and bad ones can be daunting and that’s where financial advisors come in. Engaging a trusted advisor who is experienced in investing in different asset classes can make all the difference in the world because they often have access to wealth management tools and data that make investment proposals more reliable and easier to understand.

Teaching children about saving and investing — and the mindset behind both

Although I eventually found my financial footing, others are not so lucky and many have never been able to recover once they get into debt, which can be crippling. Now that I have a family of my own, one of my top priorities is to make sure my daughter has a strong foundation in financial literacy, with all the tools she needs to make better decisions when managing money.

One of the things that we’ve started working on together is to get her to save regularly, like I did as a child. But more than teaching my daughter good saving habits, I believe what’s important is to show her the difference between the money-going-out and money-going-in concept. Very often, children are no strangers to the former because they see us making purchases daily and this makes it easy for them to learn spending (or worse, impulse spending). The latter, however, is more difficult to emulate because they rarely witness the act of saving. This is especially true now that we live in a world where most financial transactions are digital. Though this speaks to the convenience of innovation, how do we curb impulse spending in our children beyond merely saying “no” (and parents, I’m sure you’ll agree that saying “no” doesn’t always elicit the best response from children)? Continue Reading…

One of the most agreed-upon financial planning concepts is the importance of an emergency fund. Having quick access to money to pay for an unexpected expense or job loss can prevent unwanted credit card debt and can lower stress levels.

Not everyone is on board though. Some people feel that keeping money in cash instead of investing it means you’re sacrificing too much potential growth. This might be a particularly true for people who are targeting financial freedom. Since investing is an important component of reaching financial goals, it’s understandable that you don’t want to drag down your overall rate of return by holding cash.

Having access to money for unexpected expenses, though, is important for pretty much everyone. So do you need an emergency fund and if you do, how much should it be?

Do you need an emergency fund?

If you have a home equity line of credit (HELOC), you might not need funds sitting in a savings account. Whether it’s a good idea to depend on your HELOC as an emergency fund depends on two main factors: if you had to borrow from it, how long would it take you to pay if off and what is the rate of interest you’re paying?

Generally, as long as the rate of interest on the line of credit is below what you could expect to earn in the stock market, and assuming you’re able to pay down the line of credit within a reasonable time period, then using your line of credit isn’t a bad idea. The key is to make sure you are disciplined in paying down the line of credit quickly, otherwise the interest cost will outweigh what you could earn in the market.

How much do you need?

For those who don’t have a HELOC or who prefer to have a safety net in cash, determining the right amount of money to keep in an easy-to-access, low-return account is important.

There are really two kinds of emergency funds: one that will pay your expenses if you lose your job or can’t work for a period of time, and one that will pay for the large, unpredictable expenses that crop up in everyday life.

The job loss emergency fund

Job loss can mean you were laid off or that you can’t work due to illness, an accident, or a personal/family crisis. You might have heard the standard advice that says you need 3-6 months’ worth of living expense to protect against a job loss. Like all personal finance shortcuts, this isn’t necessarily helpful. How much you need in an emergency fund is highly dependent on your situation.

Here are the main factors that influence how much you should have set aside in your job loss emergency fund:

Do you have job stability? If your industry is known for sudden layoffs or if your role might be considered non-essential to an organization, you have a higher risk of losing your job and it might take you longer to find a new one. It would be wise to have a bigger cushion than someone who works in a stable industry or performs an essential role.

Do you have disability insurance? If you have an accident or get really sick, you’ll receive some kind of payment while you have to take time off work. It won’t necessarily be enough but it will help and you’ll need a smaller emergency fund. If you expect to receive no pay if you need to take time off work, you need a bigger emergency fund.

What kind of lifestyle do you want to maintain? If you are laid off, you’ll need to pare back your spending. But to what extent? What do you consider to be “essential”? Are the kids’ swimming lessons essential? What about your gym membership? Understanding what essential means to you will help you decide how much to set aside.

Do you have a partner or spouse? If you have a partner or spouse with whom you share the financial responsibilities of running a household and they are employed, would they be able to cover the essentials if you lost your job? How would your lifestyle be impacted? What is their job stability like? Do they work in the same industry as you do? If so, there might be a higher risk of both of you being laid off at the same time.

Do you have savings in a TFSA or a non-registered account? If all of your money is in RRSPs or your pension, you don’t have any good options for withdrawing money in an emergency. However, you could choose to rely on your TFSA or non-registered funds for a portion of your needs.

The large expense emergency fund

For your large expense emergency fund, the amount you want to have available depends on how many opportunities for unexpected expenses you are exposed to and what other resources you could draw on. Continue Reading…

For people with bad credit, the experience of buying a home can be quite difficult and daunting. It’s a tricky time that necessitates careful planning and preparation.

However, despite the difficulties that low credit scores may present, there are several tips and strategies you can employ to help you navigate the home-buying process. This article highlights some of these innovative strategies.

How to Buy a Home with Less than Stellar Credit

Here are some pointers to help you buy a home even if you have bad credit:

Consider Special Programs

There are numerous loan programs that do not require a high credit score or a down payment if you are a first-time homebuyer or have a low income. Some options [in the United States] to consider include USDA loans, VA loans, and the Fannie Mae HomeReady and Freddie Mac HomeOne and Home Possible loan programs.

Look for the Best Deal

Different mortgage brokers offer various rates of interest, so shop around to find the best deal. According to studies, trying to compare multiple rate quotes could save you a substantial amount of money in the long run.

Look into Down Payment Assistance

If you’re concerned about saving for a down payment, there are more than 2,500 down payment support programs available across the country for which you could be eligible. However, you need to avoid major financial changes. Taking on new debt or making a large purchase can lower your credit score, so avoid doing so while applying for a mortgage.

Things you should know about the Homebuying Process

Before you start looking for a house, you should educate yourself on the ins and outs of house purchases. Here’s a rundown of some key points to keep in mind:

Recognize why you want to Buy a House

Buying a house is a significant investment that shouldn’t be taken lightly. If you don’t know why you would like to buy a house, you may come to regret your decision later on.

Check your Credit Score

Your credit score will help you in evaluating your payment plans; lenders use it to set loan pricing and determine if you can repay your mortgage. The more favorable your credit history, the better your chances of obtaining financing at the best terms and rates. Continue Reading…

Central banks across the globe are likely to continue with their attempts to tame inflation by hiking interest rates, crushing the hope that markets will return to normality any time soon.

With the unemployment rate at a historically low level, inflation remains a top concern for the Bank of Canada (BoC) and the Federal Reserve (Fed), who are also dealing with looming risk of a recession and uncertainty regarding the impacts of the recent bank turbulence. The BoC and the Fed appear to be ahead of global peers in their attempt to slowdown inflation – raising the question around whether we have seen the peak in rates in North America.

The rapid tightening cycles by policy makers are reinforcing the appeal of owning high-

quality ultra-short bond, and money market ETFs. A series of recent rate hikes by the Bank of Canada and the Federal Reserve gave a boost to yields for these products, making the saying “cash is king” true to a certain extent, as investors who are worried about higher inflation and slowing growth prefer investing in these cash alternatives to ride out the market volatility. In today’s market, you can earn an attractive yield while taking less risk – earning while you wait for volatility to subside.

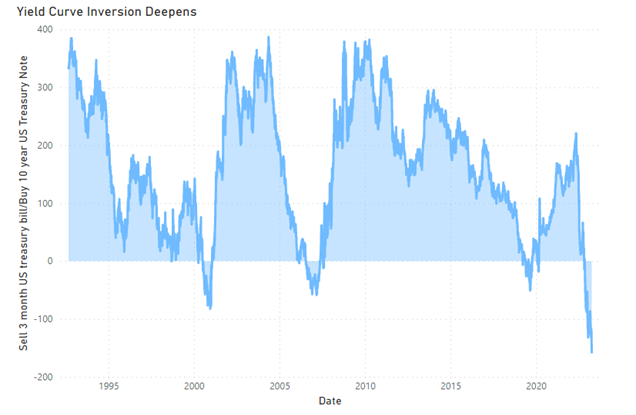

Yield curve[1], are we in love with the shape of you?

Normally, the yield curve is upward sloping, meaning longer-term bonds yield more than shorter-term bonds as investors often demand higher yields for locking their money up for a longer period. However, at present, the shape of the yield curve is inverted, which means shorter-term securities are yielding more than longer-term ones. This inversion is largely owing to the Central Bank’s quest to reduce inflation by hiking the interest rates.

Due to historically low interest rates in the last few years, investors were compelled to take more duration[2] risk by adding exposure to longer-term bonds and higher credit risk[3] by investing in lower credit quality segments such as high-yield or emerging markets bonds. However, due to the current yield curve inversion, the tables have turned now, offering a unique opportunity for fixed-income investors looking to earn higher yields.

Source: Bloomberg USYC3M10 Index (Sell 3 Month US T-bill & Buy 10 Year US Bond Yield Spread) Sep 1992 to April 2023

Why stash cash in money market & ultra-short-term bond ETFs?

The front-end of the yield curve (0-1yr) offers an attractive asymmetry and opportunity to capture yield between 4-5% + with limited duration and credit risk. This allows investors to earn the highest yields we’ve seen in more than a decade on fixed income and build a more stable high-quality fixed-income portfolio by adding exposure to ultra-short investment grade bonds and money market securities. Based on the current interest-rate volatility, hugging the front-end of the curve seems a more prudent and consistent way to preserve capital in a fixed-income allocation. BMO ETFs offers solutions such as BMO Money Market Fund ETF Series (ZMMK), BMO Ultra Short-Term Bond ETF (ZST) and BMO Ultra Short-Term US Bond ETF (ZUS), which are a great way to get exposure to the front end of the curve.

These money market & ultra short-term bond ETFs invest in high credit-quality instruments that provide a great degree of safety and capital preservation. Firstly, by investing in securities that mature in less than one year, the duration risk is minimal, which results in lower interest rate sensitivity in your portfolio. Secondly, these ETFs offer high liquidity[4] due to the nature of their underlying securities, which means they can be bought and sold easily with minimal market impact. Continue Reading…