Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

Financial Independence (aka Findependence) is a dream many hope to achieve, the freedom to live the life you’ve always dreamed of, pursuing passions or simply choosing to work on your own terms. While these are all great reasons, what about achieving this earlier?

This article will explore key investment strategies and asset allocations to accelerate your path to early financial freedom, including the role of precious metals investments.

Traditional Investments & their Limits

It’s important to acknowledge that traditional investments (stocks, bonds, mutual funds, and ETFs) will always be the building blocks when it comes to financial independence.

However, when it comes to achieving Findependence earlier in life, traditional investments may have potential limitations and risks involved.

Potential Limitations and Risks:

Inflation: Inflation erodes the real value of your accumulated savings over time.

Market Volatility: Unpredictable swings and downturns can threaten your gains and potentially delay your FI (financial independence) timeline.

Economic Uncertainty: Geopolitical risks and unforeseen crises can increase risk and cause market corrections, impacting even the safest portfolio.

While traditional investments form a crucial base for any Findependence strategy, they may not be enough to achieve the resilience and growth required. Achieving financial independence early requires specific and powerful assets to drive your portfolio, providing a balance to your financial ecosystem.

Accelerating your FI Timeline: Beyond just Investing

Accelerating your Findependence timeline requires additional steps. A crucial part is increasing your savings rate, aiming for 50% to 75% of your income, creating a powerful snowball effect that reduces your time horizon. This pairs with increasing your income through career advancement, salary raises, or profitable side hustles.

Simultaneously, optimizing expenses and embracing a frugal lifestyle in areas like housing, transportation, and food can further boost investment growth over time. A key step is defining your (FI Number) typically 25 times your desired annual expenses ($50,000). This lifestyle-specific figure provides a clear target.

Diversifying for Resilience: Beyond the Basics

Beyond traditional investments and accelerating your timeline, diversification involves not just different stocks, but asset classes as well (equities, fixed income, real estate, and alternatives). Each behaves differently under various economic challenges. Diversifying across geographies and industries can protect against downturns in a market or sector.

A crucial concept to know is asset correlation: You want your assets to not run in the same direction. According to Stock Rover, this reduction in volatility can significantly impact overall returns. For example, a portfolio experiencing wild swings of +20% then -20% loses money, while reducing it to +10% then -10% swings leads to a healthier outcome. In essence, a low correlation portfolio better withstands economic turbulence.

Strategic Allocation: The Role of Precious Metals

When aiming for early Findependence, strategic alternative assets are crucial. Gold and silver stand out as a hedge against inflation and economic uncertainty due to their low correlation nature. Historical data from Investopedia reveals that while the S&P 500 dropped almost 10% (2007-2010) during the 2008 financial crisis, a 1971 gold investment significantly increased in value. Gold IRAs also offer tax advantages for those interested in physical metals. Continue Reading…

Add to your long-term returns in the resource sector by investing in mining stocks that pay dividends

At TSI Network, we keep a sharp eye out for high-quality mining stocks that pay dividends.

Dividends are typically cash payouts that serve as a way companies share the wealth they’ve accumulated through operating the company. These payouts are drawn from earnings and cash flow and paid to the shareholders of the company. Typically, these dividends are paid quarterly, although they may be paid annually or even monthly.

Dividends can now contribute up to a third of your long-term investment returns, without even considering the tax-cutting effects of the dividend tax credit. In addition, dividends are far more reliable than capital gains. A stock that pays a $1 dividend this year will probably do the same next year. It may even increase its dividend payment.

Many investors buy gold stocks as a hedge against inflation, and some gold stocks pay dividends. But there are other mining stocks that also offer an inflation hedge: and on average pay higher dividends.

Copper stocks generally have higher dividend yields than gold stocks because they have steadier demand and more stable prices. As well, they’re usually much cheaper than gold stocks in relation to their earnings and cash flow. That means they potentially have less room to fall if markets in general fall. That’s also another way of saying that they can be less risky than gold.

Long term, copper should gain from rising demand and tighter supply. Major deposits are depleting, and environmental issues are holding back new mines.

Nutrien (symbol NTR on Toronto) is one of our favourite Canadian dividend-paying mining stocks. The company is the world’s largest producer of agricultural fertilizers, including mined potash. It took its current form on January 1, 2018, when Agrium Inc. (old symbol AGU) merged with rival Potash Corp. of Saskatchewan (old symbol POT). The stock is well-suited to income-seeking investors. The company has increased its dividend by an average of 5.8% annually in the past five years. That dividend yields 3.4%.

What’s a mining stock?

Mining stocks are investments in companies that produce or explore for minerals, such as uranium, coal, molybdenum (which is used in steelmaking), copper, silver and gold.

Mining stocks can generally be broken up into two categories, majors and juniors. Majors are mining companies that have been in the mining business for many years and more often than not they operate on a global scale. Majors have proven methods for exploration and mining, and have consistent output year over year.

Junior mining stocks are mining companies that are new or have been in business for a decade or less. They are usually smaller companies and take on risky mining exploration. If a junior mining stock is successful at finding and mining, it can mean huge returns for investors.

4 ways you benefit when you invest in mining stocks that pay dividends

Growth and income. The best dividend-paying stocks offer both capital-gain growth potential and regular income from dividend payments. In fact, dividends are likely to still be paid regardless of how quickly the price of the underlying stock rises.

Dividends can grow. Stock prices rise and fall, so capital losses often follow capital gains, at least temporarily. Interest on a bond or GIC holds steady, at best. But top dividend paying stocks like to ratchet their dividends upward—hold them steady in a bad year, raise them in a good one. That also gives you a hedge against inflation. Continue Reading…

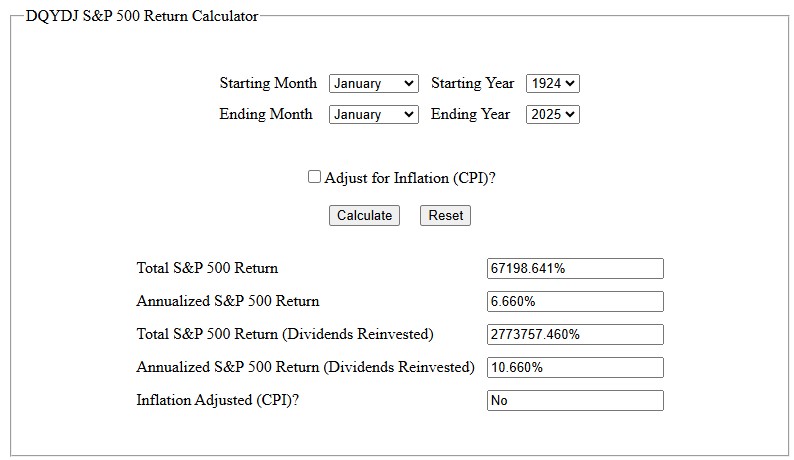

Now that 2024 is in the books, I thought I would look back financially to where we started this adventure, from January of 1991. The chart below shows the ascent of the S&P 500 Index over our 34 years of retirement.

On our retirement date of January 14, 1991, the S&P 500 index closed at 312.49. It has recently closed over 6000, making over 8% annual gains plus a couple per cent counting dividends. Hard to imagine, right? With all of the market ups and downs, global turmoil, governments coming and going, businesses expanding and failing, and still producing a better than 10% annual return.

But is this really a one-off period and not the norm?

Using a calculator, we can see that the S&P 500 returns for the last 100 years, including dividends, is 10.660%.

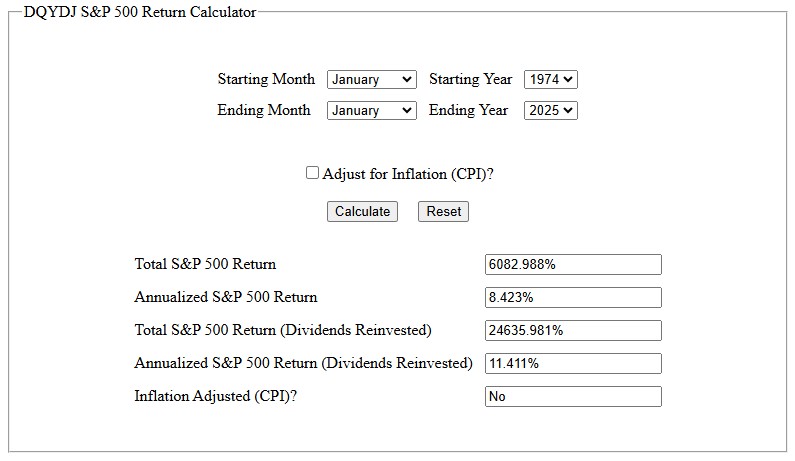

And recalculating for the last fifty years, total return is 11.411%. Clearly there is a trend here.

Does this mean that every year you invest you are going to have a 10% return? No!

But what it does tell us is that over longer time periods the return on your investment is handsomely rewarded.

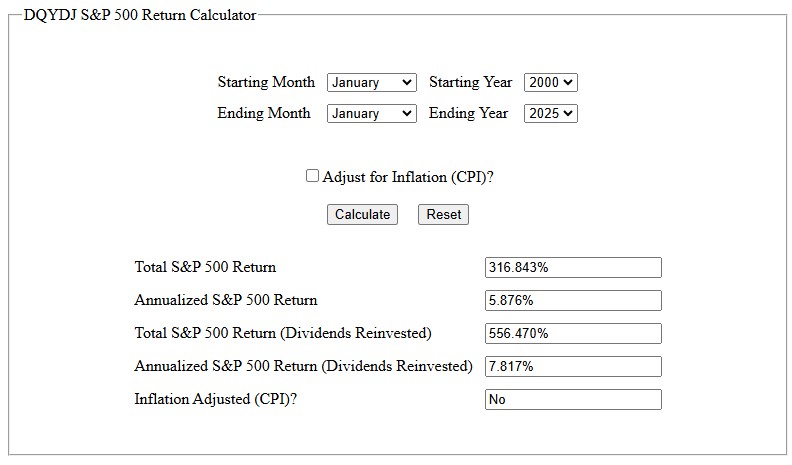

However, if we look at the returns since the year 2000 they have been sub par at an annualized rate of just 7.817%.

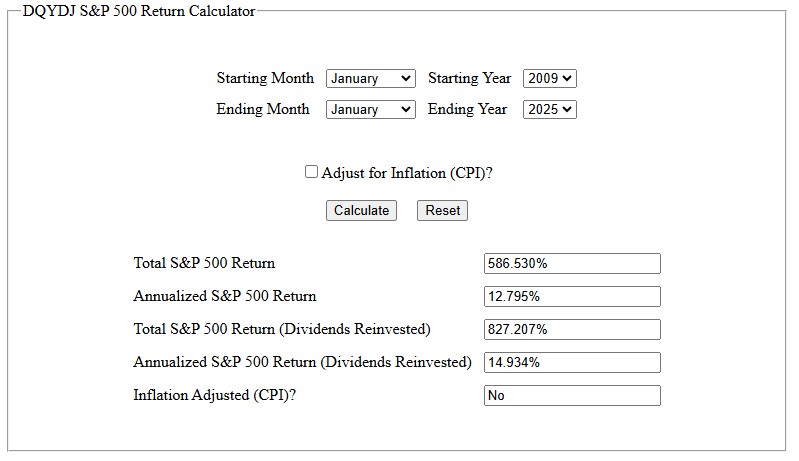

And finally, since the financial crisis in 2009, the S&P 500 Index produced a total return of 14.934% including dividends.

Getting your house in order for retirement or financial independence is not that difficult. Many investment professionals, journalists, and commentators seem to complicate the issue to the point that even we can’t understand it. Safe withdrawal rates, stocks, bonds, balanced funds, commodities, options, laddered portfolios, annuities, offshore accounts, hedge funds, life insurance … are you kidding? No wonder some people are confused and scared!

What’s a person to do?

First, you need to recognize your needs. Let’s be realistic here. How much are you spending now? Not how much do you make a year, but how much are you paying out? With today’s computer online tools and spreadsheets, this is a very easy task to compute.

Once you know your expenditures per year, take a look at where that money is going. If it’s to pay credit card bills or other consumer debt, you need to pay that off first. It’s fine to use credit cards as long as you completely pay off your balance monthly. And stay out of debt. I know this is not easy, but it’s your future, and the money you were paying in interest can now be invested.

With your debts paid off, you can commit to financial independence. Analysts say a guideline of 25 times your annual capital outlay should be enough to sustain your current lifestyle. With the data you’ve collected in your chart, you can easily calculate a target amount.

Discover practical strategies for achieving Financial Independence beyond the confines of a traditional job.

This article presents expert-backed advice on creating multiple income streams and aligning work with personal goals. Learn how to leverage your skills, build value-based income, and take concrete steps towards your vision of financial freedom.

Leverage Your Skills for Side Income

Transform Evenings into Venture Capital

Build Value-based Income Streams

Adopt a Side Hustle Mindset

Future-Proof your Professional Value

Align Work with your Core Purpose

Build a Financial Foundation first

Get Specific about your Goals

Cut Expenses to Create Options

Leverage your Skills for Side Income

In today’s evolving job market, many professionals find themselves tethered to traditional 9-to-5 roles: secure, yes, but often creatively or financially stifling. The desire for financial freedom is not just about escaping the office; it’s about reclaiming time, purpose, and the ability to design life on your own terms. We’ve worked with countless individuals who once felt exactly this way: stuck, uncertain, but ready for a change.

If you’re feeling trapped in a conventional job, the most important first step is to acknowledge that your desire for more isn’t selfish: it’s strategic. Financial freedom isn’t just about money; it’s about choices. And that journey starts by understanding your own value in the marketplace.

Step 1: Audit Your Skills and Strengths

Take stock of what you’re naturally good at and how those skills can translate into high-demand, high-autonomy industries. Digital skills like coding, copywriting, digital marketing, or consulting are especially valuable in today’s freelance and remote economy. Ask yourself: If I had to solve someone’s problem for a fee: what could I offer today?

Step 2: Start a Low-Risk Side Income Stream

This doesn’t mean quitting your job immediately. Start small: freelancing on Upwork, tutoring online, offering resume reviews, or starting a blog or YouTube channel around a niche you know well. Build proof of concept without jeopardizing your current income.

Step 3: Invest in a Career Coach or Mentor

Working with a coach can help you shortcut the confusion. We help clients identify the right path forward based on their lifestyle goals, not just job titles. Our structured guidance has helped people launch side businesses, shift into more flexible roles, or double their income by making strategic pivots.

According to a 2024 report by LinkedIn Workforce Insights, over 60% of professionals under 40 are actively seeking roles that offer greater flexibility and autonomy. Additionally, Harvard Business Review found that professionals who pursue “career portfolios” — multiple income streams from various skill-based services — report 43% higher job satisfaction and 31% faster income growth than peers in static roles.

Feeling stuck isn’t the end of your story: it’s a signal. A signal that you’re ready for change. We believe that financial freedom isn’t just for the lucky few—it’s for anyone willing to make bold, informed moves. — Miriam Groom, CEO, Mindful Career inc., Mindful Career Coaching

Transform Evenings into Venture Capital

If you’re feeling stuck in a traditional job and craving more financial freedom, you’re not alone: and you’re not broken. That restless feeling? It’s your internal compass telling you that what you’re doing no longer aligns with where you want to go. My advice? Don’t silence it: study it.

The most powerful first step I ever took was treating my evenings and weekends like venture capital. Instead of doom-scrolling or complaining about my 9-to-5, I built skills that made me valuable outside of it. I didn’t quit blindly. I audited my strengths, explored high-leverage models like consulting and digital products, and tested small bets until one clicked. It was less about passion and more about leverage: where can I help people, solve problems, and get paid well for it?

If you’re after financial freedom, don’t chase quick wins. Chase agency. Build something that compounds. Start by learning one monetizable skill: something you can offer tomorrow. Package it, test it, refine it. You don’t need to be loud online or have a business plan that wins awards. You need to take the first step: and then the next.

What I’ve learned from growing multiple businesses and coaching founders is this: freedom doesn’t arrive fully formed. It’s built in the margins before it becomes the main thing. So if you’re reading this wondering if it’s too late or too risky: it’s not. Your current job might pay the bills, but it doesn’t have to define your ceiling. — John Mac, Serial Entrepreneur, UNIT

Build Value-based Income Streams

If you feel stuck in a traditional job, it’s because your income is locked to your hours. Financial freedom begins when you earn based on value, not time. The fastest path is building a side income that proves you’re worth more than your salary. That means selling a skill — marketing, coding, design, sales strategy — directly to people who need results, not resumes.

I replaced my paycheck by packaging my experience into targeted offers. One client became two. Two became four. The process wasn’t complicated. I identified a problem, built a simple solution, and sold it. The first $1,000 didn’t change my life. It changed my mindset. From there, scaling was execution, not hope.

Most people stall because they’re waiting for the perfect idea or ideal conditions. Neither exists. Start by solving one problem for one customer. Build income that’s not tied to your boss. Cut costs, track results, and reinvest profits. Don’t romanticize the idea of freedom. Make it measurable. Give yourself a deadline to match and then exceed your job income.

You’re not trapped. You’re unproven. The solution isn’t to quit. The solution is to validate your value outside the structure you’ve been conditioned to depend on. You move forward the moment you stop waiting. — Steven Mitts, Entrepreneurial Coach, Steven Mitts

Adopt a Side Hustle Mindset

Traditional jobs are great for many reasons, but I completely understand. I was stuck in a normal or traditional 9-5 job, and the only thing I was dreaming about was freedom. This feeling is more common than you might think, so anyone who is experiencing it, you are not alone. The best advice I can offer is to change your mindset, more specifically, to adopt a side hustle mindset.

Think about what you currently have in your job: stability, which hopefully provides a decent income. This is a huge asset. Use this stability to your advantage; don’t think of it as a cage, but rather as your investment stream to financial freedom. Then, make a list of the skills you have, things that you like (passions) that could be monetized, or if you’ve noticed a problem that many people experience and you may have the solution, it could be your golden ticket.

Once you have your idea, don’t quit your day job. Dedicate a small but consistent chunk of your time each week to your new adventure (5 hours to start with will do). When it comes to the steps I’d recommend you take, there is only one: validate your idea. Do your research; you don’t want to waste countless hours on something that is already thriving. Once validated, begin your journey. Draw up a business plan, get a name (register it), open a bank account (do not use your personal one), then start. Take that first bold step. It is incredibly exciting, and it can induce a whole heap of fear, but you will never know if you don’t take it.

My encouragement is this: every great entrepreneur started with a tiny step. No one jumps into success; it is built from the ground up. — Aiden Higgins, Senior Editor and Writer, The Broke Backpacker

Future-Proof your Professional Value

Honestly, the biggest shift for professionals feeling trapped isn’t just leaving a traditional role: it’s strategically future-proofing their value. Research shows 65% of workers who feel ‘stuck’ actually suffer from skill obsolescence, yet those who dedicate just 5 hours weekly to learning in-demand capabilities like automation fluency or data-driven decision-making see a 47% faster transition to higher-paying, flexible roles.

Start by auditing daily tasks for automation potential: this reveals immediate efficiency gains and highlights valuable skills to develop. Platforms offering certified, applied learning in operational tech turn that insight into tangible leverage. That frustration? It’s actually a compass pointing toward untapped potential.

Financial freedom isn’t about escaping the grind; it’s about equipping yourself to command the work that matters. Every expert was once someone who decided their growth couldn’t wait for permission. — Anupa Rongala, CEO, Invensis Technologies

Align Work with your Core Purpose

First, define your freedom.

I’ve sat across from many successful people who feel completely trapped by their traditional jobs. My advice is always to stop focusing on the financial spreadsheet and start with a psychological one. The feeling of being “stuck” is rarely about money alone; true freedom comes from aligning your work with your “why.” Continue Reading…

How real Spending Patterns challenge Traditional Retirement Income Planning

Canva Custom Creation: Lowrie Financial

By Steve Lowrie, CFA

Special to Financial Independence Hub

Here’s a contrarian thought.

When most people imagine retirement, they picture steady cash flow from their investments to support their lifestyle.

The common assumption is that they’ll preserve their financial nest egg and live off the growth” drawing a consistent amount each year while keeping the principal largely intact.

But there are actually three broad approaches. At one end, some plan to spend their entire portfolio over their expected lifetime (as one client joked, “I want my last cheque to bounce.” At the other end is the idea of preserving capital entirely. Most people, in practice, end up somewhere in between.

But what if that assumption is only part of the story?

The reality is that real-life retirement spending isn’t flat. It fluctuates unevenly and unexpectedly over time. And those patterns can have a big impact on your retirement income strategy.

Retirement Planning has changed. Have you?

For decades, retirement planning has focused on Saving: building a nest egg, maximizing RRSPs, and making the most of tax-advantaged accounts.

But the real challenge begins after you stop working. Then, the question becomes:

How do I turn my savings into reliable, lasting income?

This is where traditional models often fall short. Most assume spending stays constant throughout retirement. But as recent research from J.P. Morgan Asset Management shows, that’s not how real retirees actually spend.

J.P. Morgan studied anonymized spending data from more than 5 million U.S. households, offering a detailed picture of how retirees actually spend in retirement. These findings closely align with what I’ve observed over 30 years of working with Canadian clients.

Three key Retirement Spending patterns:

Spending Surge: Many retirees experience a spike in spending right around the time they retire. This is often due to lifestyle changes and delayed goals coming to fruition in the early retirement years, like travel, home upgrades, or helping adult children.

Spending Curve: Over time, overall spending tends to decline. For example, households with investable assets between $250,000 and $750,000 saw an average inflation-adjusted spending decrease of about 1.65% annually through retirement.

Spending Volatility: Perhaps most important, spending is anything but steady. According to J.P. Morgan’s 2025 Guide to Retirement, 60% of retirees saw their expenses fluctuate by 20% or more in the first three years of retirement. And this volatility often continues well into later years.

These findings show that retirement income strategies need to be flexible enough to accommodate spikes, declines, and everything in between.

Why it matters

Most financial plans assume a flat, inflation-adjusted income for 25 to 30 years. That’s a very good place to start. However, based on both this research and my practical experience observing hundreds of client habits over three decades, here’s what can happen:

You over-save early, delaying retirement unnecessarily

You under-spend during healthy years, missing out on the freedom you’ve earned

You get caught off guard by spending spikes, leading to early withdrawals or tax surprises

J.P. Morgan’s data shows retirees typically need about 92% of pre-retirement income at age 65, but just 70% by age 85. That is a significant shift and a reminder of why you want healthy exposure to equities, which is the only asset class that has historically given the best chance of outpacing inflation over the long run.

A better way to Plan for Retirement Income

Here are a few ways to build a more adaptable, evidence-based retirement plan: Continue Reading…