Diversification, RRSPs, and compounding interest are important topics for investors building portfolios for retiring in Canada

Long-term stock investment strategies aren’t built to make a fast dollar. They are built to prosper over time, and most important, teach you how to pick the right stocks. Retiring in Canada can be easier if you follow our tips for building a long-term stock portfolio.

Retiring in Canada: Diversify your holdings to create a long-term retirement portfolio

One of our key rules for successful investing is to maintain a diversified stock portfolio. This means spreading your money out across most, if not all, of the five main economic sectors: Manufacturing & Industry; Resources & Commodities; Consumer; Finance; and Utilities.

Here are some additional suggestions to prepare investors for retiring in Canada:

- When it comes to a diversified stock portfolio, stocks in the Resources and Manufacturing & Industry sectors expose you to above-average share price volatility.

- Stocks in the Utilities and Canadian Finance sectors entail below-average volatility.

- Consumer stocks fall in the middle, between volatile Resources and Manufacturing companies, and the more stable Canadian Finance and Utilities companies.

Most investors should have investments in most, if not all, of these five sectors. The proper proportions for you depend on your temperament and circumstances.

Conservative or income-seeking investors may want to emphasize utilities and Canadian banks for their high and generally secure dividends.

Long-term value investing is a key part of building a balanced and diversified portfolio

The core of the long-term value investing approach is identifying well-financed companies that are established in their businesses and have a history of earnings and dividends. They are likely to survive any economic setback that comes along, and thrive anew when prosperity returns, as it inevitably does.

When you look for stocks that are undervalued, it’s best to focus on shares of quality companies that have a consistent history of sales and earnings, as well as a strong hold on a growing clientele.

Here are three of the financial ratios we use to spot them:

- Price-earnings ratios

- Price-to-sales ratios

- Price-cash flow ratios

A long-term investment strategy for retiring in Canada maximizes compound interest

Compound interest — earning interest on interest — can have an enormous ballooning effect on the value of an investment over the long-term. It can be considered the mother of all long-term investment strategies. This tip is especially important for young investors to learn. The benefits of this stock trading tip apply to both dividend-paying stocks and fixed-return, interest-paying investments such as bonds. When you earn a return on past returns, the value of your investment can multiply. Instead of rising at a steady rate, the number of dollars in your portfolio will grow at an accelerating rate.

To profit from this tip, you need to pay attention to steady drains on your capital, even seemingly small ones: like high brokerage commissions. If you’re losing (or missing out on a profit of) even 1% a year, it can have an enormous draining effect on your investments over a decade or two.

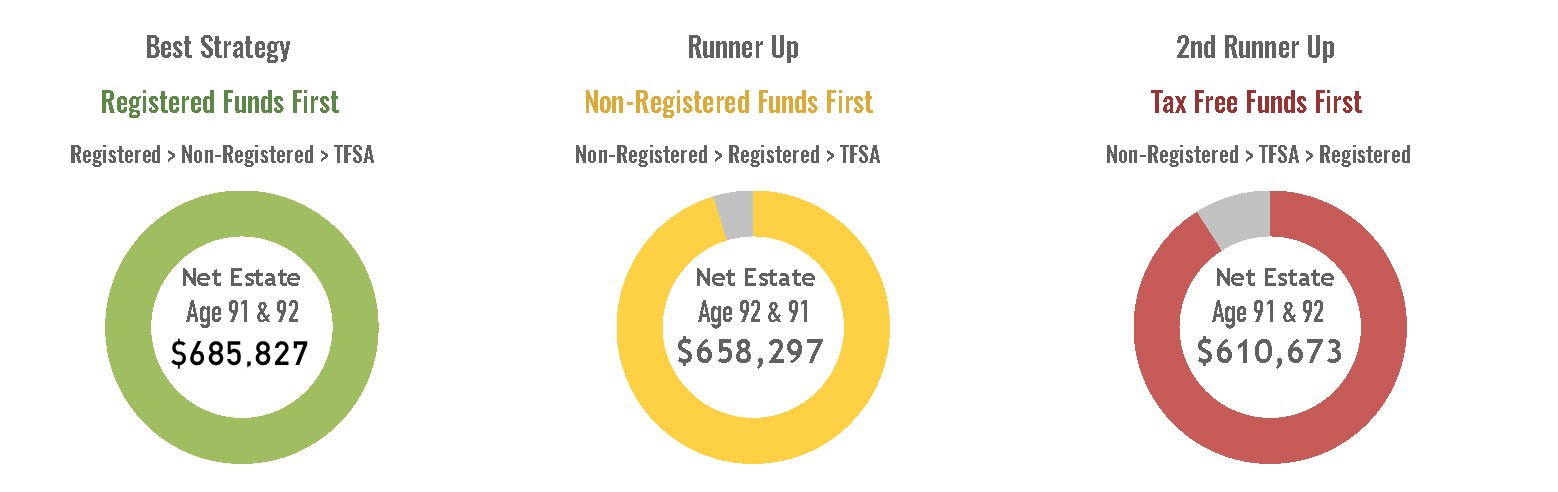

Registered Retirement Savings Plans as an option for retiring in Canada

Registered Retirement Savings Plans, or RRSPs, are a form of tax-deferred savings plan. RRSP account contributions are tax deductible, and the investments grow tax-free. When you begin withdrawing funds from your RRSP, they are taxed as ordinary income. RRSPs are the best-known and most widely used tax shelters in Canada.

Bonus tip: If you’re retiring in Canada soon, you should switch your RRSP to a registered retirement income fund (RRIF)

Why should you switch your RRSP to a registered retirement income fund (RRIF) if you’re retiring soon in Canada: as opposed to other options?

If you have one or more RRSPs, you’ll have to wind them up at the end of the year in which you turn 71. We think converting your RRSP to a RRIF (registered retirement income fund) is the best option for most investors. You have three main retirement investing options:

- You can cash in your RRSP and withdraw the funds in a lump sum. In most cases, this is a poor retirement investing option, since you’ll be taxed on the entire amount in that year as ordinary income.

- You can purchase an annuity.

- Proceed with the RRSP to RRIF conversion.

Converting your RRSP to RRIF is the best retirement investing option for most investors. That’s because RRIFs offer more flexibility and tax savings than annuities or a lump-sum withdrawal.

Like an RRSP, a RRIF can hold a range of investments. One convenient thing to note about the RRSP-to-RRIF conversion process is you don’t need to sell your RRSP holdings when you convert: you simply transfer them to your RRIF.

Retiring in Canada can be easier if long-term strategies are used. Have you employed any short-term investment strategies to prepare for retirement, and if so, how have they performed for you?

If you’ve already retired, what investment tips would you offer to those just planning their retirement finances?

Pat McKeough has been one of Canada’s most respected investment advisors for over three decades. He is the founder and senior editor of TSI Network and the founder of Successful Investor Wealth Management. He is also the author of several acclaimed investment books. This article was originally published in 2017 and is regularly updated, most recently on July 10, 2018. It is republished on the Hub with permission.