“Retirement at sixty-five is ridiculous. When I was sixty-five I still had pimples.” — George Burns (1896–1996) Comedian, actor, singer and writer

“Retirement at sixty-five is ridiculous. When I was sixty-five I still had pimples.” — George Burns (1896–1996) Comedian, actor, singer and writer

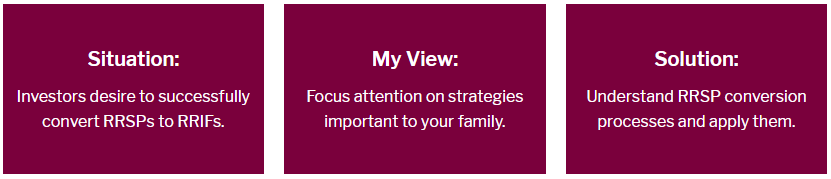

There are three retirement accounts everyone ought to understand. They are the RRSP, the TFSA and the RRIF (Registered Retirement Income Fund). I submit that the early part of each year is preferred to review the RRSP and TFSA. That leaves the RRIF to be dealt with well before year-end.

Start paying special attention to planning the RRIF, even if you don’t yet need one.

Be very mindful of the RRIF. Recognise its purpose and how it complements the other two accounts. Review it periodically to ensure it stays on track.

The RRIF is firmly entrenched as a prominent retirement planning vehicle, serving as an essential foundation of retirement nest eggs. For example, starting a RRIF at 71 implies long planning, often to age 90 or more: especially if there is a younger spouse or common-law partner.

Three conversion choices for RRSPs

RRIFs typically result from the aftermath of mandatory RRSP conversions. Three conversion choices include cashing the RRSP, purchasing a variety of annuities and using the RRIF account. The RRIF is most popular because it provides considerable flexibility. Avoid cashing RRSPs.