We’re happy to present another Decumulation blog from the forward-thinking Doug Dahmer, which you can find below.

We’re happy to present another Decumulation blog from the forward-thinking Doug Dahmer, which you can find below.

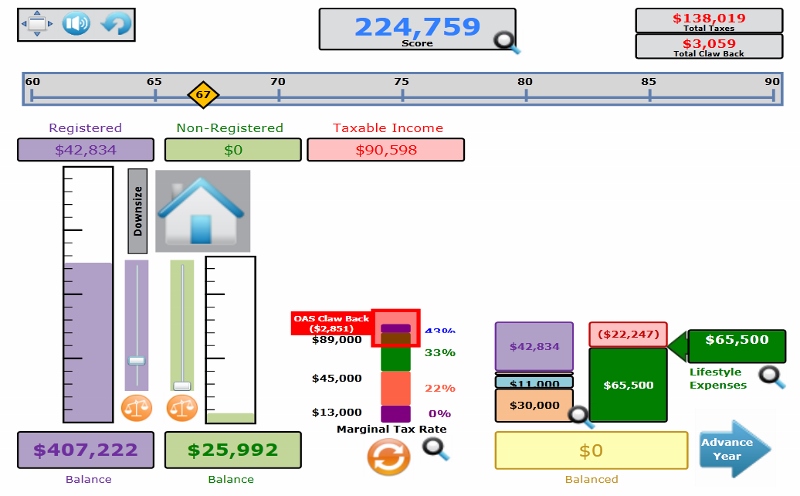

This instalment focuses on a very interesting web-based game that demonstrates how important tax planning is, particularly during your Decumulation years.

No doubt you’ll be shocked but not surprised to discover that the single biggest expense in Retirement will be income tax. Fortunately, there is more opportunity to take advantage of proper tax planning once you have begun to draw down on your nest egg. After you read Doug’s blog below, click on the links provided to view a 3-minute video on how to play the Retirement Tax Game. Then you’ll want to play the game yourself to see how well prepared you are for this daunting task. Note that you may be asked to download Microsoft Silverlight in order to play the game. — Jonathan Chevreau

By Doug Dahmer,

Emeritus Retirement Income Specialists

Special to the Financial Independence Hub

Many of our clients and friends still believe there’s inherent fairness in government programs.

When I point out disparities in medical services, government contracts, municipal board decisions, welfare payments and the greatest of them all — taxation — I, sadly, waken them to the painful reality that lots of government programs just aren’t fair.

Too often in our first world, enlightened, democratic society it is still “What you know,” “Who you know” and “When you know.”

While I can’t help with many of the program disparities I can help in one and it’s the most important to you anyway: Taxation.

The greatest expense in retirement Continue Reading…