Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

My latest MoneySense Retired Money column looks in-depth at a new “Decumulation” offering from Sun Life, unveiled late in September. You can find the full column by clicking on the highlighted headline: What is Sun Life’s new decumulation product?

As you can see from image below taken from MyRetirement Income’s website, the emphasis is on providing regular income to last to whatever age a retiree specifies. That income is not, however, guranteed as a life annuity would be.

The Globe & Mail’s Rob Carrick first wrote about this shortly after the Sun announcement. My column adds the opinions of such varied Canadian retirement experts as author and finance professor Moshe Milevsky, retired actuary Malcolm Hamilton, Caring for Clients’ Rona Birenbaum and Trident Financial’s Matthew Audrey, as well as Sun Life Senior Vice President, Group Retirement Services, Eric Monteiro.

Some of the more cynical takes are that this is a way for Sun Life to continue to profit from client financial assets gathered during the long accumulation phase, rather than seeing them migrate to other solutions, such as annuities provided by either one of its own life insurance arms or that of rivals.

Aiming for Simplicity and Flexibility

As Sun’s Eric Monteiro told me in a telephone interview, the company’s preliminary research found that rival products that were first on the market (see full MoneySense column) were often perceived as complicated, and as a result uptake of some of these pioneering Decumulation products have been underwhelming. It sought to create a solution that was relatively simple and flexible.

In essence, it is not dissimilar to some Asset Allocation ETFs, such as Vanguard’s VRIF, which is 50% equities and 50% fixed income. But Sun’s product may and probably will have different proportions of the major asset classes. In fact, it lists 16 external global money managers who deploy up to 15 different asset classes, which include Emerging Market Debt, Liquid Real Assets, Direct Infrastructure, Liquid Alternatives and Direct Real Estate. Managers include BlackRock Asset Management, Lazard Asset Management, Phillips, Hager & North, RBC Global Asset Management and its own Sun Life Capital Management. Continue Reading…

To Hedge FX Risk, or Not to Hedge: Currency markets are notoriously difficult to call but can meaningfully impact portfolio returns. ETF Strategist Bipan Rai provides a detailed framework for investing outside the Canadian market.

Image Getty Images courtesy BMO ETFs

By Bipan Rai, BMO Global Asset Management

(Sponsor Blog)

Admittedly, using a spin on a famous Shakespeare quote to start a note on currency hedging1 is verging on trite. Nevertheless, if Hamlet were running a portfolio of overseas assets, his primary concern would have to be the “slings and arrows” of currency markets — which are notoriously difficult to call but can meaningfully impact portfolio returns.

For Canadian investors, looking abroad provides several benefits. The most important is diversification, whether it’s through access to other regions that are less correlated with Canadian markets or to other products that aren’t available domestically.

However, investing abroad also means taking on foreign exchange risk given that international assets are priced in currencies other than the Canadian dollar (CAD).

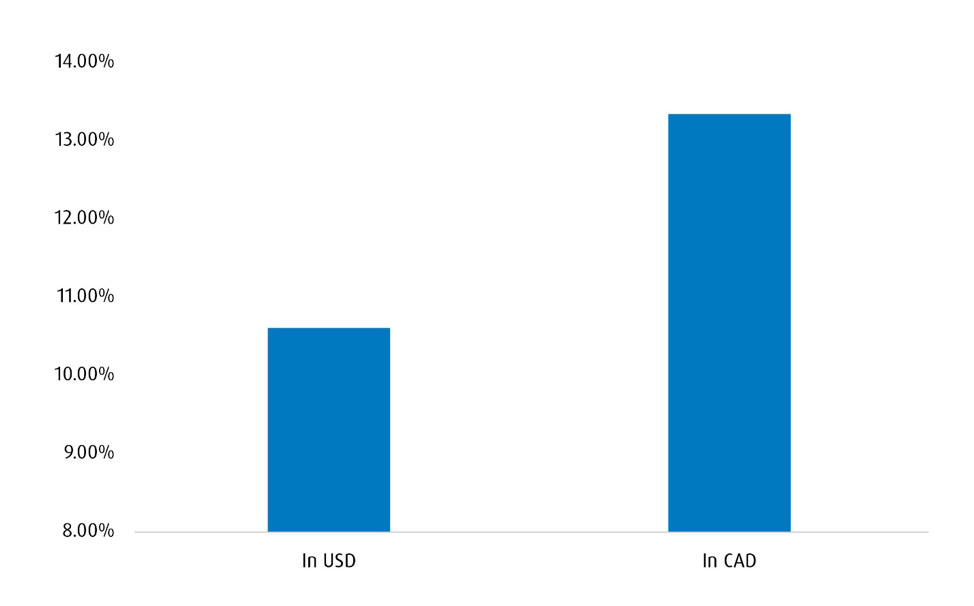

For illustrative purposes, consider Chart 1, which shows the total return for the S&P 500 in U.S. dollars (USD) and in CAD terms for Q1 of this year. In USD terms, the index was up 10.6% over that time frame, but since that period also corresponded to weakness in the CAD relative to the USD (or USD/CAD moved higher) the index outperformed in CAD terms (up 13.3%). That means that Canadian investors would have fared much better leaving their USD exposure unhedged ex ante.

Chart 1 – S&P 500 Total Return for Q1 2024

Source: BMO Global Asset Management

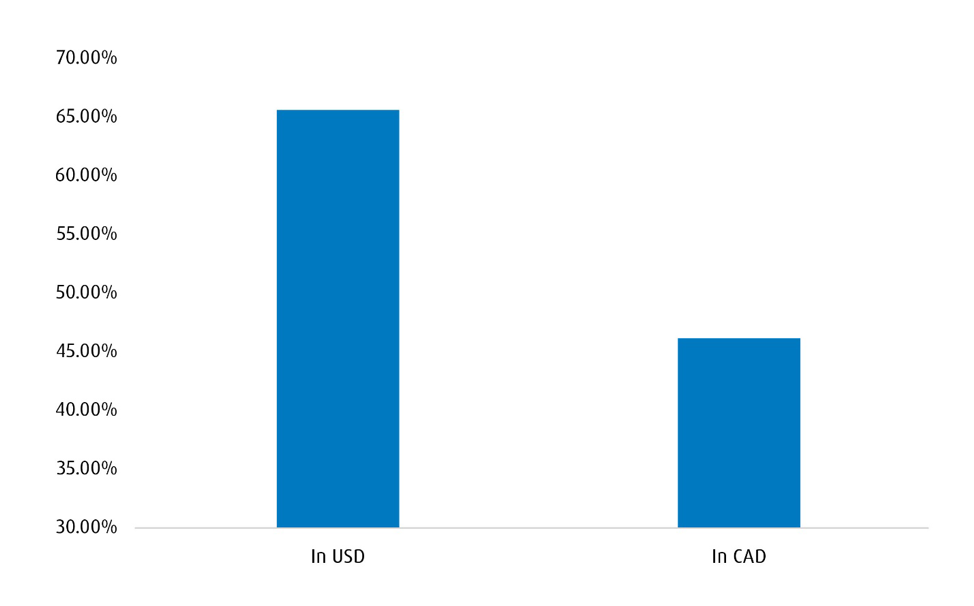

Now let’s look at an alternative period in which the CAD strengthened against the USD. Chart 2 shows a comparison of the total return for the S&P 500 from April 2020 to April 2021 (in which USD/CAD was lower by over 11%). During that period, the total return index outperformed in USD terms by close to 20%. In this scenario, an investor who had hedged their FX risk would have been in the optimal position.

Chart 2 – S&P 500 Total Return Between April 2020 – April 2021

Source: BMO Global Asset Management

As these examples show, currency risk is a key consideration for any investor who wants to look beyond Canada for diversification. That risk can cut both ways, which amplifies the importance of hedging decisions. In our minds, the decision to hedge foreign exchange (FX )risk (including the degree to which foreign exposure is hedged) comes down to the following:

An investor’s view of the underlying currency pair

Whether the currency pair is positively or negatively correlated2 with the underlying asset

In this note, we’ll make a brief comment on the first point but focus largely on the second one. as we feel that should be given more weight for hedging decisions.

FX Markets are Tough to Call

Taking a view on the underlying currency pair is easy to do — but difficult to capitalize on.

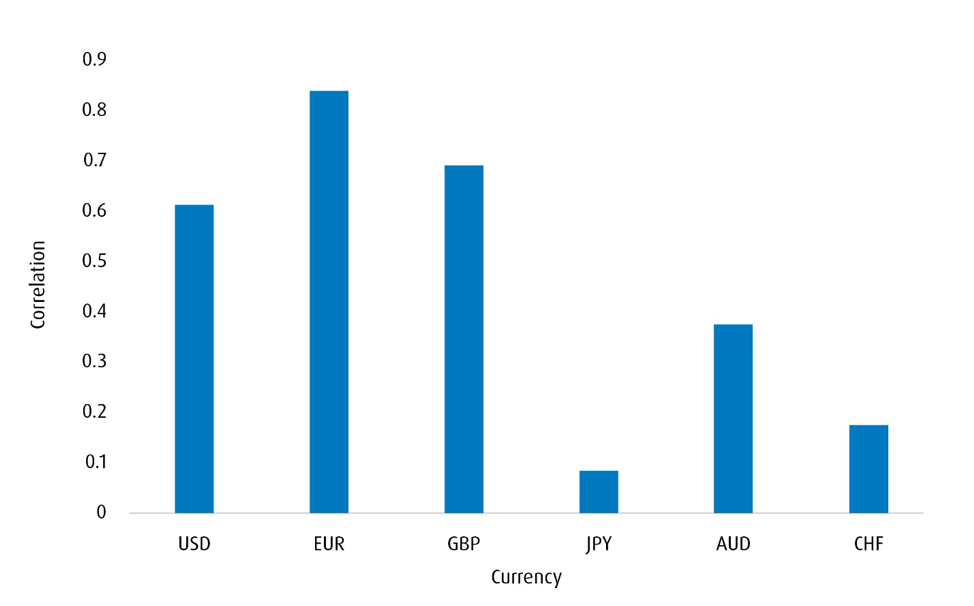

Indeed, foreign exchange markets are notoriously fickle. One reason why is the relationship between predictive factors and currency pairs is rarely stationary. For instance, a lot of market participants tend to use front-end (2-year) yield spreads as a proxy for central bank divergence in the spot FX market. Chart 3 shows the current correlation between those spreads and the different CAD crosses, and as expected, the relationship isn’t consistent from a cross-sectional perspective.

Chart 3 – Correlation Between Two-Year Spreads and the CAD Crosses

* * Correlation window is 2 years. The CAD is used as a base currency for this analysis. The spread is tabulated by subtracting the foreign 2-year yield from the CAD 2-year yield. Source: Bloomberg, BMO Global Asset Management.

We can also see this by looking closer at the relationship between a factor and a currency pair over time. Chart 4 shows the rolling 100-day correlation between USD/CAD and the price of oil (proxied by the prompt WTI contract3) going back ten years. Note how frequently the strength of the correlation (as well as the sign) changes over time. Continue Reading…

The following is an edited transcript of an interview conducted by financial advisor Darren Coleman of the Two Way Traffic podcast with tax lawyer Anna Malazhavaya of Advotax Law.

It appeared on September 6th under the title ‘What you need to know about recent tax changes in Canada.’ Advotax is a team of lawyers and tax professionals that serves individuals, businesses and real property owners with tax planning and tax-dispute resolutions involving the Canada Revenue Agency. The discussion explored everything from the capital gains inclusion rate to expanded powers of the CRA to clients asking about moving to the US.

“It’s emotional but for some the increase in the capital gains inclusion rate was the last straw as they choose to leave Canada,” said Anna who added that over four million Canadians hold more than one property which means the government’s claim that this affects only 0.13% of the population isn’t true. “People are calling me every week. The wealthiest, the most talented entrepreneurs, are leaving Canada. It’s very sad to see.”

Anna and Darren talked about this phenomenon and how the June 25th deadline made it more expensive to leave the country with what can be a hefty departure tax. They also got into RRSPs, RIFs, and bare trusts which involve putting your property in someone else’s name. Anna said while the bare trust may have been designed to catch those who are less than scrupulous, it also captures honest people and gave examples.

I want your perspective and what your clients are thinking about the capital gains change we saw recently, and the deadline for people making changes. Now we’re in the new environment where the inclusion rate, or the amount of money you have to pay tax on, has gone up. And the government told us this was only going to affect 0.13% of taxpayers. Do you think their math was right?

Anna Malazhavaya

I have doubts. I’m not an economist and don’t have access to all the government stats, but I can share some stats. Capital gain may apply on the sale of your property that is not your principal residence. This includes your cottage, and your investment in rental properties.

4 million Canadians hold more than one property

Darren Coleman

More than four million Canadians hold more than one property. So four million Canadians, potentially, may be subject to that new increase capital gain rate. So that’s not 0.13%. That’s more.

Anna Malazhavaya

It’s way more. Of course, if I argued for the other side, I would say, Well, you don’t know how much money these people made on the property, and the first $250,000 of capital gain is still subject to the old rate, and that’s true. But at the same time, something tells me if these people held the property for more than 10 years that gain will be substantial. Look at how the real estate market performed in the last 20 years.

Darren Coleman

A lot of these people will be subject to the new rules. And not only that, think about people who only have one property, and let’s say, live on a farm property, and they have their house. When they sell their property, not the entire sale price will be sheltered by the principal residence exemption, but only the portion that’s required for the maintenance of their farm property. Everything in excess will be subject to capital gain and can potentially be subject to these new higher rates. Do you know how the government arrived at their number? A reasonable solution would have been to look at past taxpayer data and say, if we look at the last five or 10 years, how many taxpayers had a capital gain over $250,000? Let’s average it out over a bunch of years. But that’s not what they did. They looked at one year, 2022, and said only 0.13% of taxpayers had a capital gain of over $250,000. But that was also a negative year for stock markets globally, and a bit of a negative year for real estate equity markets everywhere. Tell me a little more about how your clients are experiencing this change.

Anna Malazhavaya

Until 2022 I probably had five people consulting me about leaving Canada. Normally, it was the other way around. We had all those talented people who wanted to bring their money, settle their life in Canada, educate their children here, build their future, build businesses, hire people. Pay taxes at 54% mind you. But this year alone, I have over a dozen new clients who plan to leave Canada and for my practice it’s a big change. People calling me practically every week, saying, I’m done. You know what? This capital gain game change. It did not affect me today. It probably won’t affect me tomorrow, but it’s the straw that broke the camel’s back.

More Canadians want to leave the country

Darren Coleman

The people who used to hire people, who used to come up with brilliant solutions, making everyone’s life better, they’re leaving Canada. Very sad to see and you’re not alone in experiencing that. I had a conversation this morning with a cross-border tax accountant and he said he’s had a surge of people looking to leave Canada, and he blames it on the tax policies which are making it less attractive for them to be here. Is it easy to just pack up and go to places like Florida?

Anna Malazhavaya

Leaving Canada became a lot more expensive. If you want to leave Canada, you are treated by Canadian law as if you sold all of your assets, even though you’re not selling anything. You keep all your assets. But the government says, Okay, fine, you want to leave Canada, but we want all the tax on the gain that you accrued to date. Some call it a departure tax, although this isn’t an official name, but it can hit you hard if you decide to leave Canada. So you have to declare all the gain you had from all your assets. Continue Reading…

I have been saving since I arrived in Canada 25 years ago. During my first year I saved as little as $10 month, but in general I saved about $25 during the first 10 years, then I increased the amount I was saving to about $500 per month and during the past 5 years I was saving as much as $1,000 per month.

Finally this year, I stopped contributing to my retirement accounts. Instead, I started taking out whatever I get as a dividend distribution from my non-registered account.

I have to tell you. It feels good!

I have accumulated over $500,000. According to the 4% rule, I can withdraw the equivalent of $20,000 per year, which is more or less my cost of living.

At this moment I am only withdrawing from 1% to 2% of my capital per year. I am withdrawing the dividend distributions from my non-registered accounts.

I see some cash siting on my broker’s account and I just transfer it to my checking account and I invite myself for dinner.

At the beginning of the year, I transfer the maximum allowed from my non-registered account to my TFSA. I have a feeling that the maximum allowed for 2024 will be $7,000. I will be ready.

Transferring capital from non-registered account to TFSA will allow to earn more and pay less taxes.

I am in the fortunate position where I don’t even need my retirement money right now. My part time job, which I love, provides me enough to live.

I think that I will use my retirement money to pay for some luxuries that I haven’t paid for myself before, like… instead of taking one vacation per year, I will take two vacations per year, one to my home country, and another to any other random country. Continue Reading…

Cut The Crap Investing recently looked at the go-to chart on creating retirement income. The post looked at sustainable spend rates. The 4% “rule” suggests that you can start at a 4.2% spend rate, and then increase spending each year to adjust for inflation. That protects your spending power and lifestyle in retirement.

That said, the 4% rule is based on a very conservative 50/50 stock to bond allocation using U.S. assets. We might be able to boost the spend rate in retirement by adding more growth and more non-correlated assets.

In the above post and charts we see the challenges of a 5% or 6% spend rate with a traditional balanced portfolio.

Here’s a very good post that shows how we can potentially boost our spend rate. And the go-to table on boosting your retirement start date with gold, REITs, small cap value, and international stocks in the mix. The equity allocation is moved up to 70% as well.

From that post …

So instead of limiting your retirement portfolio to the S&P 500 and government bonds, think about diversifying with small-cap value and gold! If you don’t mind a little more complexity, go a step further with REITs, utilities, and international stocks. This level of diversification has done very well in the past. It includes at least one asset that does well in each type of economic situation.

That post offers a nod to the all-weather portfolio and utilities as a defensive asset. Readers will know I am a favour of both additions, especially the defensive sectors for retirement that includes consumer staples, healthcare and utilities (including pipelines and telco). I’m hopeful that the approach will allow us to boost our spend rate to the 5-6% range.

Canadian banks in 2024

At the beginning of the month we looked at investing in Canadian banks. I noted that it is difficult to pick the winners and there is a surprising variance in returns among the individual banks. Here’s the total returns in 2024. Continue Reading…