Recently, I was helping a young person with his first ever RRSP contribution, and this made me think it’s a good time to explain a confusing part of the RRSP rules: contributions in January and February. Reader Chris Reed understands this topic well, and he suggested that an explanation would be useful for the upcoming RRSP season.

Contributions and deductions are separate steps

We tend to think of RRSP contributions and deductions as parts of the same set of steps, but they don’t have to be. For example, if you have RRSP room, you can make a contribution now and take the corresponding tax deduction off your income in some future year.

An important note from Brin in the comment section below: “you have to *report* the contribution when filing your taxes even if you’ve decided not to use the deduction until later. It’s not like charitable donations, where if you’re saving a donation credit for next year you don’t say anything about it this year.”

Most of the time, people take the deductions off their incomes in the same year they made their contributions, but they don’t have to. Waiting to take the deduction can make sense in certain circumstances. For example, suppose you get a $20,000 inheritance in a year when your income is low. You might choose to make an RRSP contribution now, and take the tax deduction in a future year when your marginal tax rate is higher, so that you’ll get a bigger tax refund.

RRSP contribution room is based on the calendar year

Each year you are granted new RRSP contribution room based on your previous year’s tax filing. This amount is equal to 18% of your prior year’s wages (up to a maximum and subject to reductions if you made pension contributions). You can contribute this amount to your RRSP anytime starting January 1. Continue Reading…

Are you a patient investor? Or are you looking at your portfolio multiple times a day, having the itch to sell everything? Despite having done DIY investing for over a decade and making my shares of investment mistakes in the past, I am still learning about investing on a daily basis.

One key lesson I’ve learned is short-termism will hurt your investment. As investors, we need to have patience and a long term view.

What is short-termism?

Per Wikipedia, short-termism is giving priority to immediate profit, quickly executed projects and short-term results, over long term results and far-seeing action.

On the surface, it seems that short-termism is associated with investment strategies like day trading, momentum trading, short selling, and options trading. However, I believe many investors that invest in individual dividend stocks and passive index ETFs often fall into the short-termism trap as well.

How so?

On one hand, it’s about short-term profit taking. On the other hand, it’s about paying too much attention to the short-term share price movement and feeling the need to tweak your investment portfolio. Some common portfolio management questions I’ve seen on Facebook and Twitter are:

“Should I take profits when the stock goes up and re-invest the money later? Give me a reason why I shouldn’t sell and should just hold?”

“I purchased Royal Bank at $110. It’s frustrating seeing the share price going up to $150 and then dropping back down to $125. Should I sell when the stock is at a 52-week high and buy back when the stock price dips?”

“I have a small paper loss on Brookfield Asset Management, I don’t think the company is doing well, should I sell and invest the money elsewhere?”

“I bought some Apple shares recently. Apple had a terrible quarter and I’m down. I’m convinced that Apple is going to crash and burn. Should I sell and run now?”

And the questions go on and on…

Why do we fall into the short-termism trap?

There are many reasons why we fall into the short-termism trap. Some of the common reasons I believe are:

The need to be correct – we as investors want to see our investments increase in value once we make the purchase. When this happens, it means we’re right and made the correct investment decision. If the share price goes down, that must mean we are wrong and are terrible at investing. The need to be correct becomes a burning desire. Nobody wants to be told that they are wrong and be the laughingstock.

The need to be validated – we all have the need to be validated by others but for some reason, this need is even stronger when it comes to investing. We want others to validate that we made the right investment decision so we can feel good inside. The desire to be validated can be like drugs, once someone validates you, you begin to want even more. The need to be validated is a very slippery slope…

Looking for gains right away – It’s exciting to see investment gains. It is even more exuberating to see significant gains in a few days. It’s like going to the casino and winning 1000 times on your bet or winning the lottery. Why wait for five years to see multi-bagger gains when you can get the same type of gains in a week? Long-term investing is for losers!

Ego – for some reason we all believe we are better investors than who we truly are. Believe me, I fall into this trap from time to time. Deep inside, we believe that we can predict how companies will do in the future accurately by looking at past performance and public information.

How to escape the short-termism trap?

So how do we escape the short-termism trap? I think the best method is to understand your short-term, medium-term, and long-term goals. Are you investing for the short-term or are you investing for the long-term? Knowing this will dictate what kind of investments you should buy. Continue Reading…

It goes without saying that 2022 was a less than stellar year for equity investors. The MSCI All Country World Index of stocks fell 18.4%. There was virtually nowhere to hide, with equities in nearly every country and region suffering significant losses. Canadian stocks were somewhat of a standout, with the TSX Composite Index falling only 5.8% for the year.

Looking below the surface, there was an interesting development underlying these broader market movements, with value stocks far outpacing their growth counterparts. Globally, value stocks suffered a loss of 7.5% as compared to a decline of 28.6% in growth stocks. This substantial outperformance was pervasive across countries and regions, including the U.S., Europe, Asia, and emerging markets. In the U.S., 2022’s outperformance of value stocks was the highest since the collapse of the tech bubble in 2000.

These historically outsized numbers have left investors wondering whether value’s outperformance has any legs left and/or whether they should now be tilting their portfolios in favor of a relative rebound in growth stocks. As the following missive demonstrates, value stocks are far more likely than not to continue outperforming.

Context is everything: Value is the “Dog” that finally has its Day

From a contextual perspective, 2022 followed an unprecedented period of value stock underperformance.

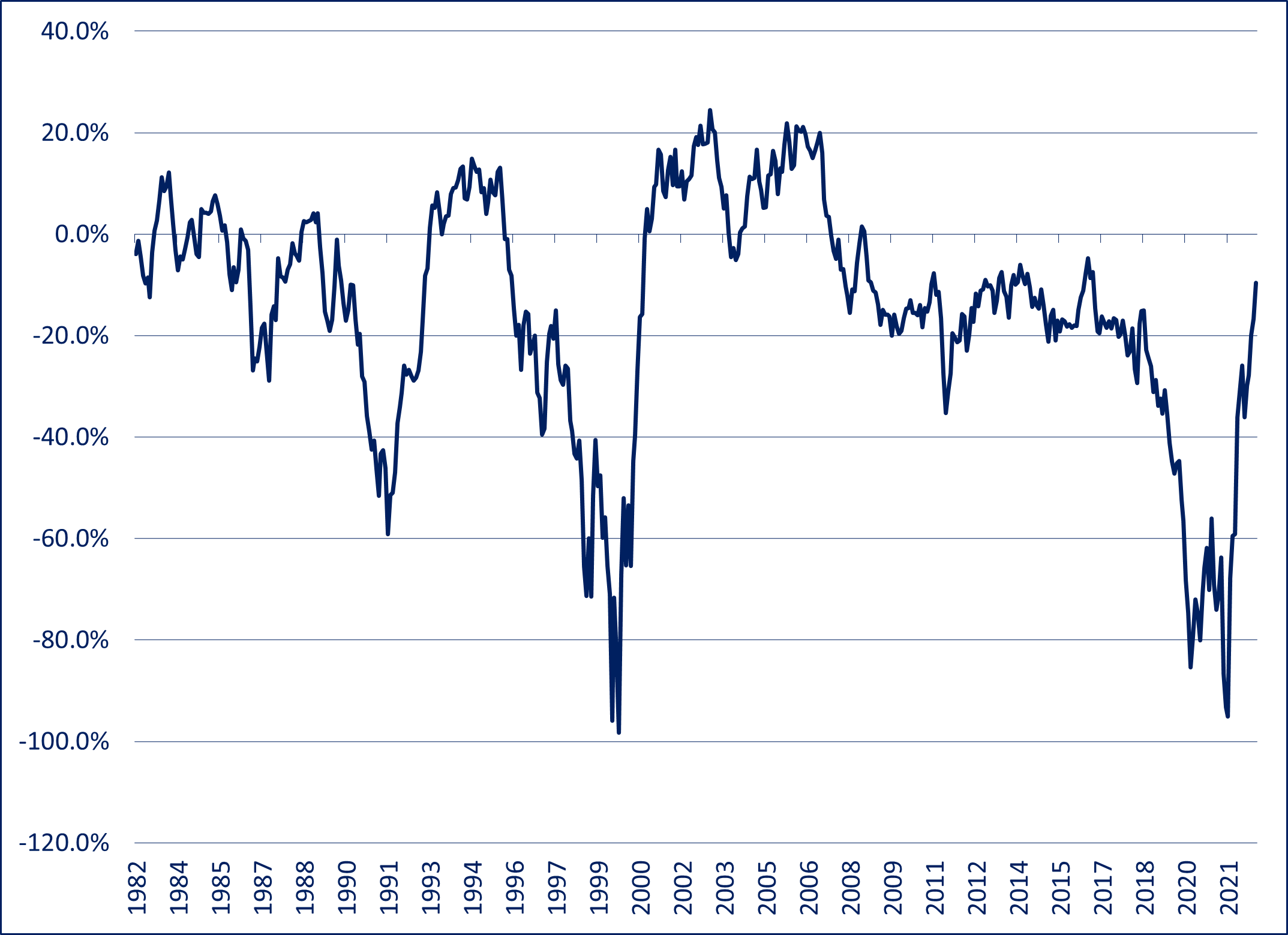

U.S Value vs. U.S. Growth Stocks – Rolling 3 Year Returns: 1982-2022

Although there have been (and will be) times when value stocks underperform their growth counterparts, the sheer scale of value’s underperformance in the several years preceding 2022 is almost without precedent in modern history. The extent of value vs. growth underperformance is matched only by that which occurred during growth stocks’ heyday in the internet bubble of the late 1990s.

Shades of Tech Bubble Insanity

The relative performance of growth vs. value stocks cannot be deemed either rational or irrational without analyzing their relative valuations. To the extent that the phenomenal winning streak of growth vs. value stocks in the runup to 2022 can be justified by commensurately superior earnings growth, it can be construed as rational. On the other hand, if the “rubber” of growth’s outperformance never met the “road” of superior profits, then at the very least you need to consider the possibility that crazy (i.e. greed, hope, etc.) had indeed entered the building.

The extreme valuations reached by many growth companies during the height of the pandemic bring to mind a warning that was issued by a market commentator during the tech bubble of the late 1990s, who stated that the prices of many stocks were “not only discounting the future, but also the hereafter.”

U.S. Value Stocks: Valuation Discount to U.S. Growth Stocks: (1995-2022)

Based on forward PE ratios, at the end of 2021 U.S. value stocks stood at a 56.3% discount to U.S. growth stocks. From a historical perspective, this discount is over double the average discount of 27.9% since 1995 and is matched only by the 56.6% discount near the height of the tech bubble in early 2000. This valuation anomaly was not just a U.S. phenomenon, with global value stocks hitting a 57.5% discount to global growth stocks, more than twice their average discount of 27.6% since 2002 and even larger than that which prevailed in early 2000 at the peak of the tech mania. Continue Reading…

Front page of Wednesday’s Financial Post print edition.

Plenty of press this week over a BMO survey that found Canadians now believe they’ll need $1.7 million to retire, compared to just $1.4 million two years ago (C$). The main reason for the higher nest-egg target is of course inflation.

As you’d expect, the headline of the story alone attracted plenty of media attention. I heard about it on the car radio listening to 102.1 FM [The Edge]: there, a female broadcaster who was clearly of Millennial vintage deemed the $1.7 million ludicrously out of reach, personalizing it with her own candid confession that she herself hasn’t even begun to save for Retirement. Nor did she seem greatly fussed about it.

Here’s the Financial Poststory which ran in Wednesday’s paper: a pick-up of a Canadian Press feed; a portion is shown to the left. The writer, Amanda Stephenson, quoted BMO Financial Group’s head of wealth distribution and advisory services Caroline Dabu to the effect the $1.7 million number says more about the country’s economic mood than about real-life retirement necessities.

BMO’s own client experience finds that “many overestimate the number that they need to retire,” she told CP, “It really does have to be taken at an individual level, because circumstances are very different … But $1.7 million, I would say, is high.”

Here’s my own take and back-of-the-envelope calculations. Keep in mind most of the figures below are just guesstimates: those who have financial advisors or access to retirement calculators can get more precise numbers and estimates by using those resources. I may update this blog with input from any advisors or retirement experts reading this who care to fill in the blanks by emailing me.

A million isn’t what is used to be

Image via Tenor.com

Back in the old days, a million dollars was considered a lot of money, even if that amount today likely won’t get you a starter home in Toronto or Vancouver. This was highlighted in one of those Austin Powers movies, in which Mike Myers (Dr. Evil) rubs his hands in glee but dates himself by threatening to destroy everything unless he’s given a “MILLL-ion dollars,” as if it were an inconceivably humungous amount.

The quick-and-dirty calculation of how much $1 million would generate in Retirement depends of course on your estimated rate of return. When interest rates were near zero, this resulted in a depressing conclusion: 1% of $1 million is $10,000 a year, or less than $1,000 a month pre-tax. When my generation started working in the late 70s, a typical entry-level job paid around $12,000 a year so you could figure that $1 million plus the usual government pensions would get you over the top in retirement.

Inflation has put paid to that outcome but consider two rays of hope, as I explained in a recent MoneySense Retired Money column. To fight inflation, Ottawa and most central banks around the world have hiked interest rates to more reasonable levels. Right now you can get a GIC paying somewhere between 4% and 5%. Conservatively, 4% of $1 million works out to $40,000 a year. 4% of $1.7 million is $68,000 a year. That certainly seems to be a liveable amount. More so if you have a paid-for home: as I say in my financial novel Findependence Day, “the foundation of Financial Independence is a paid-for home.”

Couples have it easier

If you’re one half of a couple, presumably two nest eggs of $850,000 would generate the same amount: for simplicity we’ll assume a 4% return, whether in the form of interest income or high-yielding dividend stocks paid out by Canadian banks, telecom companies or utilities. I’d guess most average Canadians would use their RRSPs to come up with this money.

This calculation doesn’t even take into consideration CPP and OAS, the two guaranteed (and inflation-indexed) government-provided pensions. CPP can be taken as early as age 60 and OAS at 65, although both pay much more the longer you wait, ideally until age 70. Again, couples have it easier, as two sets of CPP/OAS should add another $20,000 to $40,000 a year to the $68,000, depending how early or late one begins receiving benefits.

This also assumes no employer-pension, generally a good assumption given that private-sector Defined Benefit pensions are becoming rarer than hen’s teeth. I sometimes say to young people in jest that they should try and land a job in either the federal or provincial governments the moment they graduate from college, then hang on for 40 years. Most if not all governments (and many union members) offer lucrative DB pensions that are guaranteed for life with taxpayers as the ultimate backstop, and indexed to inflation. Figure one of these would be worth around $1 million, and certainly $1.7 million if you’re half of a couple who are in such circumstances.

Private-sector workers need to start RRSPs ASAP

But what if you’re bouncing from job to job in the private sector, which I presume will be the fate of our young broadcaster at the Edge? Then we’re back to what our flippant commentator alluded to: if she doesn’t start to take saving for Retirement seriously, then it’s unlikely she’ll ever come up with $1.7 million. In that case, her salvation may have to come either from inheritance, marrying money or winning a lottery.

For those who prefer to have more control over their financial future, recall the old saw that the journey of a thousand miles begins with a single step. In Canada, that step is to maximize your RRSP contributions every year, ideally from the moment you begin your first salaried job. Divide $1.7 million by 40 and you get $42,400 a year that needs to be contributed. OK, I admit I’m shocked by that myself but bear with me. The truth is that no one even is allowed to contribute that much money every year into an RRSP. Normally, the limit is 18% of earned income and the 2023 maximum RRSP contribution limit is $30,780 (and $31,560 for the 2024 taxation year.) Continue Reading…

For U.S. stocks, my wife and I hold 17 Dividend Achievers, plus 3 stock picks. In Canada, I hold the Canadian Wide Moat 7, while my wife holds a Canadian High Dividend ETF – Vanguard’s VDY. There is also a modest position in the TSX 60 – XIU. The U.S. and Canadian stocks both outperform their respective stock market index benchmarks. Working together, the U.S. and Canadian stocks form an all-weather portfolio base.

In this post I’ll offer up charts on our U.S. stock portfolio and the Canadian stock portfolio. And I’ll put them together so that we can see how they work together. The total portfolio was designed to be retirement-ready. The fact that it beats the market benchmarks is a welcome surprise. At the core of the portfolio is wonderful Canadian dividend payers – the U.S. dividend achievers and 3 picks fill in some portfolio holes. We will also take a look at how these stocks can be arranged to provide an all-weather stock portfolio base.

When I write ‘our portfolio,” I am referring to the retirement portfolios for my wife and me. As for ‘backgrounders’ on the portfolios please have a read of our U.S. stock portfolio and the Canadian Wide Moat 7 performance update.

The stock portfolios

In early 2015 I skimmed 15 of the largest-cap dividend achievers. What does skim mean? After extensive research into the portfolio “idea” I simply bought 15 of the largest-cap dividend achievers. For more info on the index, have a look at the U.S. Dividend Appreciation Index ETF (VIG) from Vanguard. That is a U.S. dollar ETF. Canadian investors can also look to Vanguard Canada for Canadian dollar offerings (VGG.TO).

You’ll find the dividend acheivers and Canadian high dividend stocks in the ETF portfolio for retirees post. Both indices are superior for retirement funding, compared to core stock indices.

Dividend growth plus quality

At the core of the index is a meaningful dividend growth history (10 years or more) working in concert with financial health screens. It leads to a high quality skew. Given those parameters the dividend achievers index will certainly hold many dividend aristocrats (NOBL).

The 15 companies that I purchased in early 2015 are 3M (MMM), PepsiCo (PEP), CVS Health Corporation (CVS), Walmart (WMT), Johnson & Johnson (JNJ), Qualcomm (QCOM), United Technologies, Lowe’s (LOW), Walgreens Boots Alliance (WBA), Medtronic (MDT), Nike (NKE), Abbott Labs (ABT), Colgate-Palmolive (CL), Texas Instruments (TXN) and Microsoft (MSFT).

United Technologies merged with Raytheon (RTX) and then spun off Carrier Global Corporation (CARR) and Otis Worldwide (OTIS). We continue to hold all three and they have been wonderful additions to the portfolio. Given that those stocks are not available for the full period, they are not a part of this evaluation. That said, the United Technologies spin-offs added to the outperformance.

Previous to 2015 we had three picks by way of Apple (AAPL), BlackRock (BLK) and Berkshire Hathaway (BRK.B). Those stocks are overweighted in the portfolio. As you might expect, Apple has contributed greatly to the portfolio outperformance. Though the achievers also outperform the market with less volatility.

In total it is a portfolio of 20 U.S. stocks.

The Canadians

I hold a concentrated portfolio of Canadian stocks. What I give up in greater diversification, I gain in the business strength and potential for the companies that I own to not fail. They have wide moats or exist in an oligopoly situation. For the majority of the Canadian component of my RRSP account I own 7 companies in the banking, telco and pipeline space. I like to call it the Canadian wide moat portfolio. They also provide very generous and growing dividends. These days, they’d combine to offer a starting yield in the 6% range.

Here are the stocks:

Canadian banking

Royal Bank of Canada (RY), Toronto-Dominion Bank (TD) and Scotiabank (BNS).

Telco space

Bell Canada (BCE) and Telus (T).

Pipelines

Canada’s two big pipelines are Enbridge (ENB) and TC Energy (TRP).

*Total performance would be improved by holding the greater wide moat portfolio that includes grocers and railway stocks. That is a consideration for those in retirment and in the accumulation stage.

The Canadian mix outperforms the market, the TSX Composite. You’ll also find that outperformance in the Beat The TSX Portfolio. That BTSX strategy (like the Wide Moat 7) finds big dividends, strong profitability and value.

Once again, my wife holds an ETF – the Vanguard High Dividend (VDY) and a modest position in XIU. I did not want to expose her portfolio to concentration risk.

The charts

Here’s the returns of the U.S. and Canadian portfolios, plus a 50/50 U.S/CAD mix as the total portfolio. The period is January of 2015 to end of September 2022. Please keep in mind the returns are not adjusted for currency fluctuations. A Canadian investor has received a boost thanks to the strong U.S. dollar. U.S. investors owning Canadian stocks would experience a negative currency experience. Continue Reading…