Alain Guillot in Cascais, Portugal, a rich neighborhood.

By Alain Guillot

Special to Financial Independence Hub

Learning how you can turn a little bit of money into a lot of money is a great way to get your finances on the right track. After all, this can help with everything from paying off debt and credit card bills to growing your savings.

With that in mind, here are some top tips that you can use to do exactly that!

Add money to your savings immediately after getting paid

Don’t wait until the end of the month (i.e., when you have spent all your money) to think about transferring cash into your savings account. Instead, transfer a pre-designated amount of money into your savings account each payday. This way, you are reducing the chances of spending money you’d originally wanted to save!

By regularly adding to your savings account, you put yourself in the best possible position to improve your finances in the long term. When setting up a savings account, make sure you choose one with a great interest rate!

Start investing

Whether you’re going to buy and sell Cyrpto currency or going down a more traditional investment pathway, investing money is a great way to turn a little cash into a lot of cash. This can also be a great way to earn passive income, as a lot of the work is out of your hands once you’ve made the initial investment.

Of course, you should make sure to do plenty of research ahead of time so that you are protecting your best interests as much as possible. Remember, while no investments are risk-free, some are more stable than others, and you should not invest money you cannot afford to lose.

Turn your hobby into a side-hustle

Turning your hobby into a side hustle can also help you to turn your finances around, and could even become a real money-maker over time. While it may not seem that way to begin with, you can monetise just about every hobby. Whether you’re a painter or a writer, you simply need to be willing to put the work in to refine your craft and get your name out there. Continue Reading…

My latest MoneySense Retired Money column looks at a curious Canadian phenomenon called The Annuity Puzzle: that while life annuities sold by insurance companies seem to have all sorts of compelling reasons to acquire them, more often that not retirees shun them.

Engen notes that experts like Finance professor Moshe Milevesky and retired actuary Fred Vettese say “converting a portion of your savings into guaranteed lifetime income is one of the smartest and most efficient ways to reduce retirement risk.” Vettese has said the math behind an annuity is “pretty compelling,” especially for those without Defined Benefit pensions.

Engen observes that a life annuity is “the cleanest version of longevity insurance … You hand over a lump sum to an insurer, and they guarantee you monthly income for life. If you live to 100, the insurer pays you. If stock markets collapse, you still get paid. If you’re 87 and never want to look at a portfolio again, the income keeps flowing.”

In other words, annuities neutralize the two big risks that haunt retirees: Longevity Risk (the chance of outliving your money) and Sequence-of-returns risk: the danger of suffering a stock-market meltdown early in Retirement and inflicting irreversible damage on a portfolio.

Despite all the seeming positives about annuities, Engen notes that “almost nobody buys one.” He cites a Vettese estimate that only about 5% of those who could buy an annuity actually do so.

A chance to lock in recent portfolio gains?

Even so, the new Retirement Club created by former Tangerine advisor Dale Roberts earlier this year — see this blog posted on this site in June — recently featured a guest speaker who extolled the virtues of annuities: Phil Barker of online annuities firm Life Annuities.com Inc. Barker said many clients tell him they’ve done really well in the markets over the last 20 years and now they’d like to lock in some of those gains. They may be looking for Fixed-Income strategies and many were delighted with GIC returns when they were a bit higher than they are now (some in the range of 5%). But they less happy with the new rates on GICs now reaching maturity. Meanwhile, annuities have just come off a 20-year high in November 2023 so the time to consider one has never been better, Barker told the Club in August. With annuities you can lock in a rate for the rest of your life so if your timing is good, it may make sense to allocate some funds to them.

See the full MoneySense column for the list of the eight life insurance companies that offer annuities in Canada, how they are covered under Assuris, when Annuities really shine, and how to fund annuities with registered or non-registered accounts.

I suspect the Club’s session on annuities was enough to get a few members off the fence. I have long been impressed by the aforementioned Fred Vettese, who often argues that those preparing to convert their RRSPs into RRIFs might opt to annuitize 20 or 30% of the amount, thereby transferring a chunk of investment risk from the do-it-yourself investor on to the shoulders of a Canadian life insurance company. Continue Reading…

If you’ve ever felt nervous about the stock market ups and downs, you’re not alone. Most investors want their money to grow steadily without the wild swings: especially if you’re thinking about retirement. Lately, worries about an AI bubble and changing interest rates have shown just how quickly things can get unpredictable.

That’s why building the right portfolio is important to help you stay calm and stay invested, even when markets get a little rocky.

Low-volatility investing, and specifically using funds such as BMO Low Volatility Canadian Equity ETF (ZLB) and BMO Low Volatility US Equity ETF (ZLU), are designed to give you a smoother experience. These strategies help you stay invested with confidence no matter what the markets are doing.

What does Low Volatility mean for your Investments?

Imagine low-volatility investing as playing it smart in baseball: not trying for risky home runs, but focusing on steady singles and doubles. This way, you keep making progress, scoring runs over time, and avoiding big losses. It’s all about reliable growth, not wild swings that could set you back.

ZLB and ZLU are designed to help your investments stay on track, even when markets get unpredictable. They pick companies that don’t jump around as much as the overall market: think of them as the steady players on the team. By steering clear of those big ups and downs, your money can grow more smoothly, and you can benefit from compounding over time.

Building a Smoother Ride with Low volatility

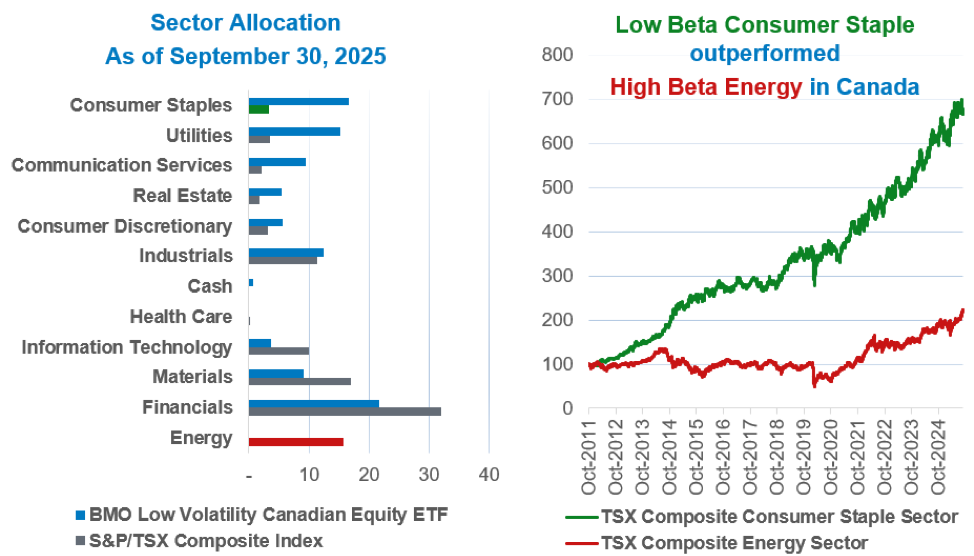

ZLB and ZLU focus on defensive sectors like utilities, consumer staples, and healthcare. These ETFs can act as financial shock absorbers, reducing risk from market swings and limiting exposure to more volatile sectors like technology. Position and sector caps further protect against over-concentration, while the selection of low-beta1 companies means the portfolio is designed to cushion losses during downturns.

The disciplined construction of ZLB and ZLU helps you stay on course regardless of market conditions. This approach isn’t about chasing the latest trends but about building steady, long-term growth through stability and diversification, letting compounding work its magic over time.

Low volatility cushioned the blow with stability

Chart 1

Note: Data as of September 30, 2025. Source: BMO AM Inc. Bloomberg Sector allocation subject to change without notice. Chart compares sector allocations of BMO Low Volatility Canadian Equity ETF and S&P/TSX Composite Index as of September 30, 2025, and shows Consumer Staples outperforming Energy in Canada from 2011 to 2024.

Common Myth: Low-Volatility ETFs reduce Return

Low volatility doesn’t mean you have to settle for lower returns. In fact, Canadian low-volatility investments have consistently outpaced the S&P/TSX Capped Composite Index since inception, offering strong returns while helping to reduce risk.

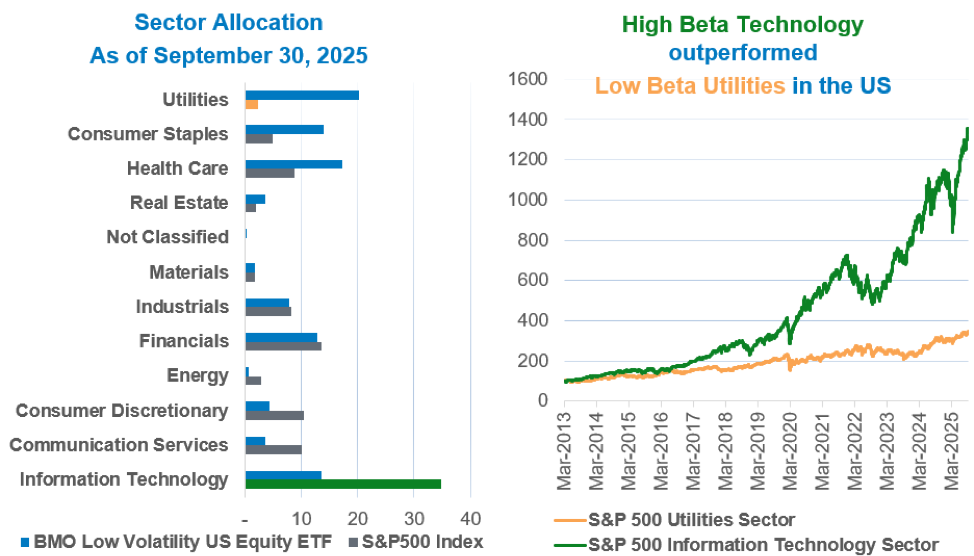

Chart 2

Note: Data as of September 30, 2025. Source: BMO AM Inc. Bloomberg Sector allocation subject to change without notice. Chart compares sector allocations of BMO Low Volatility US Equity ETF and S&P 500 Index as of September 30, 2025, and shows Technology outperforming Utilities from 2013 to 2025.

The U.S. market is highly concentrated in the Magnificent 72 and generally information. Because ZLU invests more in stable sectors like utilities and healthcare, it provides steady, long-term returns, though it might not keep up with the S&P 500 when the market is booming, as it has more recently with the growth dominated in the Tech sector. Even with this more cautious approach, ZLU still delivers strong annual returns for investors by emphasizing stability and value rather than jumping into the latest tech trends.

Balanced Growth, Less Stress: Blending ETFs for Smoother Returns

If you want steady growth for your portfolio without taking on too much risk, you may not have to choose between safety and strong returns. By combining BMO Low Volatility US Equity ETF (ZLU) with BMO NASDAQ 100 Equity Index ETF (ZNQ), you can get the best of both worlds: reliable stability and exciting growth. This mix has delivered higher returns and lower risk than simply investing in BMO S&P 500 Index ETF ( ZSP) as shown in Chart 3. Continue Reading…

Canada is about to experience an unprecedented transfer of wealth across generations that will transform household balance sheets, life plans, and the role of financial advisors. Experts estimate that roughly $1 trillion will transfer between generations over the next decade, and this shift is discussed weekly.

As someone who advises families across multiple generations, I see three key implications. First, the amount of capital shifting hands is significant, but equally important are the who and the how: younger recipients seek different things than their parents. Second, the timing and structure of transfers (gifts made during life versus testamentary bequests) are driven by family dynamics as much as tax considerations. Third, the industry itself must modernize to stay relevant: advice now goes beyond portfolio selection to include income architecture, behavioral coaching, private-market access, values alignment, and digital delivery. The landscape is changing more quickly than I have experienced in the past 25 years.

Understanding what each generation needs and why they want it is the foundation for giving meaningful advice.

Baby Boomers: stewardship, income, and legacy

Baby Boomers still hold a disproportionate share of wealth in Canada, and their priorities have shifted from accumulation to preservation, predictable income, and legacy planning. The questions they ask are practical and existential: Will I outlive my money? How do I leave a legacy without causing family conflicts? How do taxes and health-care risks affect my plan? In practice, this means structuring retirement income to address longevity risk, incorporating tax-efficient solutions, and creating estate plans that minimize friction at death.

At Trans Canada Wealth, an advisory group of Harbourfront Wealth’s independent platform, we integrate investment strategies with our in-house CPA tax specialist and estate planning expertise so clients can see the full chain of outcomes, cash flow, taxes, and transfer, rather than isolated portfolio returns. This comprehensive approach is what gives Boomers the peace of mind they value most. We walk clients through our “Atlas” system to ensure they have peace of mind that no stone has been left unturned and that they have a structure and plan that works for their unique situation.

Gen X: the bridge generation demanding clarity

Generation X is in the middle, often financially squeezed, supporting aging parents while raising children, yet they are likely to be the most active people in managing wealth transfers. Many Gen X clients will inherit significant wealth but usually don’t plan for it; instead, they seek control, transparency, and practical plans that address debt today, catch up on retirement savings, and fund education. Unlike parents of previous generations, they have a stronger desire to help their children buy their first home and ensure they start their financial journey on solid footing.

An important role for advisors is facilitation: helping families have clear conversations about intentions and timing. We frequently counsel Boomers on the merits of lifetime gifts versus estate transfers because earlier transfers can increase intergenerational utility and allow parents to witness the benefits. Equally, Gen X wants straightforward, independent advice that filters noise, ensuring one poor decision doesn’t derail a 20- or 30-year plan.

Millennials: aligning performance with purpose

Millennials prioritize differently when they invest. While performance remains important, purpose and fees are now key factors. Studies and industry reports reveal that younger investors are highly interested in sustainable and impact strategies; they seek access to alternative investments and ESG-informed allocations as part of a diversified portfolio.

For advisors, this means providing institutional-grade access and clear discussions about costs alongside values-based solutions. Millennials are well-informed but have limited time; they expect advisors to add value by curating investment opportunities, conducting thorough due diligence, and explaining trade-offs: such as how an ESG focus might affect risk/return, liquidity, and fees. When advisors excel at this, they not only retain inherited capital but also build lifelong relationships.

Gen Z: digital-first, early adopters and learners

Gen Z approaches wealth conversations with a different relationship to money. They are digital natives, comfortable transacting and learning online, and many start their investing journey earlier than previous generations. Research shows a significant rise in early retail investing and financial literacy among Gen Z, and their expectations for digital access, education, and transparency are high. Continue Reading…

Here’s what we think about real estate investing in Canada — and it may surprise you

TSInetwork.ca

We’re constantly asked about real estate investment in Canada (or investment in Florida real estate, for that matter), and we understand the appeal. Even though today’s house prices still remain high in most markets (i.e., Toronto and Vancouver) mortgage interest costs are expected to fall as inflation comes back down. And owning your own home has a number of advantages.

In terms of real estate investment, owning your house is a great tax shelter. That’s because gains on your principal residence are exempt from capital-gains taxes. Note, though, that this benefit only applies to your principal residence, and not investment in Florida real estate as a second home or income property. You must still pay tax on gains on the sale of a recreational property, such as a cottage or a ski chalet. But these properties generally appreciate at a much slower rate than, say, a home in a major urban centre. That’s a key consideration with any real estate investment.

What are the best real estate investment strategies in the current market?

Given Canada’s diverse real estate landscape in 2025, the most effective strategy is to focus on suburban multi-family properties in growing secondary markets like Hamilton, Halifax, or Kelowna, where prices remain relatively affordable while offering strong rental demand and potential for appreciation.

What are the potential risks of investing in real estate right now?

The primary risks include rising interest rates affecting mortgage payments, potential market corrections in overvalued areas, and stricter regulations on foreign buyers and short-term rentals in major Canadian markets.

Capital-gains taxes are also applicable to gains on real estate investment, such as rental properties you buy for investment purposes. Moreover, this type of real estate investing in Canada (or investment in Florida real estate) involves a number of other commitments that can make it feel more like running a small business than, say, investing in stocks. With stocks, you only have to tell your broker to buy: everything else is done for you.

By contrast, when you own rental property, you have to spend time finding and dealing with tenants, arranging for maintenance, doing the accounting and so on. You can hire others to do these tasks for you, but that can get very expensive.

Moreover, real estate investing in Canada can entail higher levels of risk than stocks. That applies to investment in Florida real estate and other U.S. sunshine destinations. Simply put, all real estate investment must contend with the fact that real estate is less liquid, more expensive to manage and to buy or sell, and highly geographically concentrated. Rising crime, unpleasant neighbours and other changes on the street or in your property’s neighbourhood can make it hard to find tenants or buyers. So can physical problems, like adverse traffic patterns, backed-up sewers and zoning changes that allow undesirable development, or limit what you can do with your real estate investment property.

Many real estate investing enthusiasts say that if you buy a property with a 20% down payment (which is the Canadian government’s proposed new minimum to qualify for government-backed mortgage insurance on a property that is not your principal residence), then a 20% rise in the property’s value means you have doubled your money.

However, that claim neglects the costs of selling (up to 5% or 6% for real-estate commissions, plus lawyer’s fees and related costs). It also overlooks any negative cash flow you may have experienced while you owned the property, because rents failed to cover expenses. When you’re less familiar with the market, such as with Canadian investment in Florida real estate, that kind of unfavourable outcome is more likely.

How can I prepare my real estate investments for potential economic downturns or unexpected events?

Maintaining substantial cash reserves (ideally 6-12 months of expenses per property), keeping conservative loan-to-value ratios, and diversifying across different property types and locations provides the strongest protection against market volatility.

What is the best long-term investment strategy for building wealth through real estate?

The most reliable strategy is buying and holding cash-flowing multi-family properties in growing metropolitan areas while systematically paying down the mortgages to build equity over time.

We continue to believe that ownership of a primary residence is all the real estate exposure most investors need. Still, we get many questions about real estate investment beyond that. If you want to add to your real estate holdings, one good way to do it is through real estate investment trusts, or REITs.

Real estate investment trusts invest in income-producing real estate, such as office buildings and hotels. Some may even focus on investment in Florida real estate or other key U.S. markets for vacationers. Generally, that’s a segment of the market that is difficult for most investors to access through direct ownership of property. Moreover, real estate investment trusts save you the cost, work and risk of owning investment property yourself.

If you’re interested in real estate investing in Canada through a REIT, we still recommend RioCan Real Estate Investment Trust (symbol REI.UN on Toronto). It, like all REITs, continues to suffer fallout from the COVID-19 pandemic. Still, RioCan continues to benefit from an increasingly solid portfolio of properties now focused on Canada’s biggest markets. It is also working to diversify its portfolio beyond malls (these malls feature large stores that are usually part of a chain). We cover RioCan in our Successful Investor newsletter. Continue Reading…