No doubt about it: at some point we’re neither semi-retired, findependent or fully retired. We’re out there in a retirement community or retirement home, and maybe for a few years near the end of this incarnation, some time to reflect on it all in a nursing home. Our Longevity & Aging category features our own unique blog posts, as well as blog feeds from Mark Venning’s ChangeRangers.com and other experts.

Duke University conducted a two-year study of 218 healthy adults of normal weight to determine if a modest, sustained calorie reduction would show appreciable benefits. The plan was to reduce calories consumed by 25 per cent, but participants were unable to achieve that much.

(Author’s note: I sure couldn’t do it! A 25% reduction in my 2,000 daily calories would leave me staggering around at only 1,500 per day.)

Participants were able, however, to cut calories by an average of about 12 per cent. This smaller change allowed them to stick to the plan without any adverse effect on mood (wherein lies a useful message in itself). The results? Lowered blood pressure; decreased insulin resistance; as well as a drop in several predictors of cardiovascular disease.

But the most appreciable result concerned C-reactive protein, a substance produced by the liver and a marker of inflammation in the body. The participants’ C-reactive levels plunged by almost half: a remarkable 47%!

It’s a no brainer that poor dietary habits would exacerbate internal inflammation. But very often this is an invisible menace (see my article ‘The Truth About Inflammation’, October 2015). Most of us remain blissfully unaware of any chronic inflammation cascading throughout our bodies. Yet this exposes us to chronic health risks as a result of knocking the body out of whack. In my case, I had the aforesaid silent inflammation and observable inflammation, which I felt in my poor old joints. And I am pretty convinced that chronic inflammation was one factor in my developing cancer.

An elevated C-reactive protein level can be a valid identifier of inflammation in the body. So, if just a 12% calorie restriction can reduce this marker by almost 50%, this is as good information as that available to an insider trader.

In the blindness of youth, so many of us can compromise our health in a mad dash for wealth. But from the other end of the lifespan, a good many seniors would gladly sacrifice some wealth for even a smidgen of better health. Those who don’t make time for their health early on in life more often have to make time for illness later.

5 ways to improve your physical health

So, if you are young, young at heart, worried that you are no longer young, here is some insider information. Five smart, little investments you can make, the aggregate interest of which, over time, will have compound into positive health returns. Continue Reading…

Once they move from the wealth accumulation phase to “decumulation” retirees and near-retirees start to focus on how to boost Retirement Income.

The latest instalment of myMoneySense Retired Money column looks at five “enhancements” to do this, all contained in Fred Vettese’s about-to-be-published book, Retirement Income for Life, subtitled Getting More Without Saving More. You can find the full column by clicking on this highlighted headline: A Guide to Having Retirement Income for Life.

You’ll be seeing various reviews of this book as it becomes available online late in February and likely in bookstores by early March. I predict it will be a bestseller since it taps the huge market of baby boomers turning 65 (1,100 every day!): including author Fred Vettese and even Yours Truly in a few months time.

That’s because a lot of people need help in generating a pension-like income from savings, typically RRSPs, group RRSPs and Defined Contribution plans, TFSAs, non-registered investments and the like. In other words, anybody who doesn’t enjoy a guaranteed-for-life Defined Benefit pension plan, of the type that are still common in the public sector but becoming rare in the private sector.

The core of the book are the five “enhancements” Vettese has identified that help to ensure that those seeking to pensionize their nest eggs (to paraphrase the title of Moshe Milevsky’s book that covers some of this ground) don’t outlive their money. Vettese says many of these concepts are current in the academic literature but have been slow to migrate to the mainstream, in part because few of these “enhancements” will be welcomed by the typical commission-compensated financial advisor. That in itself will make this book controversial.

Each of these “enhancements” get a whole chapter but in a nutshell they are:

1.) Enhancement 1: Reducing Fees

By moving from high-fee mutual funds or similar vehicles to low-cost ETFs (exchange-traded funds), Vettese explains how investment fees can be cut from 1.5 to 3% to as little as 0.5% a year, all of which goes directly to boosting retirement income flows. One of his takeaways is that “Tangible evidence of added value from active management is hard to find.”

2.) Enhancement 2: Deferring CPP Pension

We’ve covered the topic of deferring CPP to age 70 frequently in various articles, some of which can be found here on the Hub’s search engine. Even so, very few Canadians opt to wait till age 70 to collect the Canada Pension Plan. Because CPP is a valuable inflation-indexed guaranteed for life instrument — in effect, an annuity that you can never outlive — Vettese argues for deferral, although he (like me) is fine with taking Old Age Security as soon as it’s available at age 65. He argues that for someone who contributed to CPP until age 65, they can boost their CPP income by almost 50% by waiting till 70 to collect. “You are essentially transferring some of your investment risk and longevity risk back to the government, and you are doing so at zero cost.” Continue Reading…

Whether it’s junk food, drugs, alcohol, cigarettes or simply laziness there are many things that can lead to an unhealthy life. Not being health conscious can have dire consequences and you can easily walk yourself into an early grave if you don’t take care of your body. But it doesn’t have to be that way. With these tips to live by, you can stay healthy well into your retirement years.

1.) Keep fit

No matter what your age, you should be exercising regularly and doing your best to stay fit. While you don’t need to become a marathon runner or boxing expert, try to exercise for at least 30 minutes every day to maintain a healthy body and mind. Don’t believe that you have to tone it down when you reach a certain age either: your body will keep up with what you offer it. If you don’t start running until the age of 50 then you might have some problems but someone who regularly runs well into their fifties will be able to keep it up. Exercise helps to strengthen your heart, keep your body working and mobile and release endorphins to ease stress and improve mood.

2.) Eat healthily

There’s nothing wrong with a treat now and then but you need to stick to well-balanced meals and healthy snacks for the most part if you want to live for a long time. Eating the wrong diet, can result in obesity, diabetes, digestive problems, heart problems and high cholesterol. And that’s only the start. Eat well: remember that when you put good stuff in, you will get bad stuff out.

3.) Laugh often

One of the best ways to extend your life is to enjoy it. Failing to spend time with friends and family, to entertain yourself, to have fun and laugh daily can be almost as harmful to your health as smoking or drinking. If you enjoy yourself, you exercise your heart muscles, ease stress and tension and keep a positive mind. If you don’t, you increase your risk of depression, illness, and complications associated with stress such as heart attacks. Continue Reading…

Doug Dahmer, CEO and founder of www.RetirementNavigator.ca has been a regular guest contributor to the Hub since its inception in November 2014. His focus is on Canada Pension Plan optimization, avoidance of retirement tax traps, and the creation of drawdown strategies during the decumulation side of financial planning. Some of these ideas have been used (with proper attribution) in various columns I’ve written in other media outlets, generally summarized here at the Hub.

However, Dahmer has been noticeably quiet lately. This blog explains why.

As the headline says and the adjacent image suggests, Doug is about to turn financial planning on its head. How? By democratizing access to financial planning, in the same way that Robo-Advisors democratized investing. This disruption of the planning industry is built upon a new planning platform called Better Money Choices.

Asked what motivated him to launch this venture Dahmer said more than 70% of Canadians say their greatest worries in life are centred around their financial futures. “Yet at the same time it is estimated that fewer than 15% of Canadians have a formal financial plan in place.”

As he talked to clients about this disconnect — why they resisted the idea of financial planning as an Rx to their financial stress — he discovered most people have no idea what true financial planning looks like.

Doug Dahmer, creator of BetterMoneyChoices.com

“The financial services industry has twisted the planning process into a tedious, time-consuming, onerous task that’s heavily biased toward the sale of financial products. What they hated most about planning, is that, more often than not, the conclusion to the process was always the same: spend less, save more, work longer, work harder. These recommendations were made while providing little in the way of understanding of the specific rewards these sacrifices would deliver.”

In short, Planning did not relieve their level of stress, it actually increased it!

Money doesn’t buy stuff, it buys choices

True planning was never meant to promote the sale of financial products. It’s supposed to be a process that allows you to explore the lifestyle choices you are thinking about, so you can discover their future financial implications before you need to commit to them. “Armed with this insight, you can then decide whether you’re willing to make the necessary sacrifices to bring them to fruition.”

Your most valuable asset isn’t money. It’s Time — and how you choose to spend it

Dahmer’s financial planning philosophy is based on the belief our lives are defined by the choices we make: the more good choices we make, the better our lives will be. His new site, BetterMoneyChoices.com, lets people quickly, easily and securely explore their lifestyle choices so they can better determine what outcomes they should focus on.

Everyone’s personal resources – time, money, energy, relationships and talents – are limited in some way. That forces each of us to make choices to accept less of one thing in order to obtain more of the things that are most important to us. However, seldom is “more money” what we are seeking.

It’s time the financial planning sector evolved with the times

Dahmer says technology has given us many low cost/no-cost, self-serve tools that make almost all aspects of our lives easier, but not yet financial planning. “My mission is to change this. By putting the focus on how you want to live your life instead of how much money you can accumulate, and making it easy for you to determine which set of choices will bring you closer to what you value most, the technology behind the Better Money Choices process will revolutionize planning.”

His goal is to make it a quick, easy and engaging process to determine the trajectory our lives are tracking. “I want to convert the misnomers that planning is an event that translates into an exact science to the reality that planning is an ongoing, never ending process of making a set of best guesses – projecting those best guesses into the future – then re-engaging with life to learn more.”

Such a process requires frequently returning to our ever-living planning platform to check our progress and improve upon our guesses. “Once people understand what true planning looks like and the huge benefits that can accrue by adopting this approach for directing them to better choices, their disdain for planning will finally disappear and they will rely on their planning tools with the same natural inclination they reach for their google maps when it comes time to choose how best to arrive at their desired destination.”

Exact pricing has yet to be determined, but Dahmer’s goal is to have a monthly subscription that is comparable to Netflix or Spotify.

Beta Testing

Dahmer is currently running a beta test to get user feedback, prior to it being released publicly (currently scheduled for April 1st, 2018, coincidentally a week before I myself turn 65).

Doug has asked me to participate as one of the early beta testers and I have agreed to do so. In the past week, I have been “playing” with the software with our own personal data and I can tell you already it’s an eye opener. Over the next few weeks on the Hub, I’ll report back to you on my experiences with the software and the impact this novel approach to planning has had on my own plans for the second half of my life.

After all, I’m hardly unique in turning 65 this year: some 1,100 other Canadians now do so each day. (Incidentally, I’ll be collecting my first Old Age Security cheque late in May but, as per the guidance of Doug and his new software, I’ve elected to wait until age 70 to collect the Canada Pension Plan. This too has been reported in my columns in the country’s two major daily newspapers or MoneySense.ca )

If you’d like to be one of the first to know when the site officially launches, you can sign up at www.BetterMoneyChoices.com.

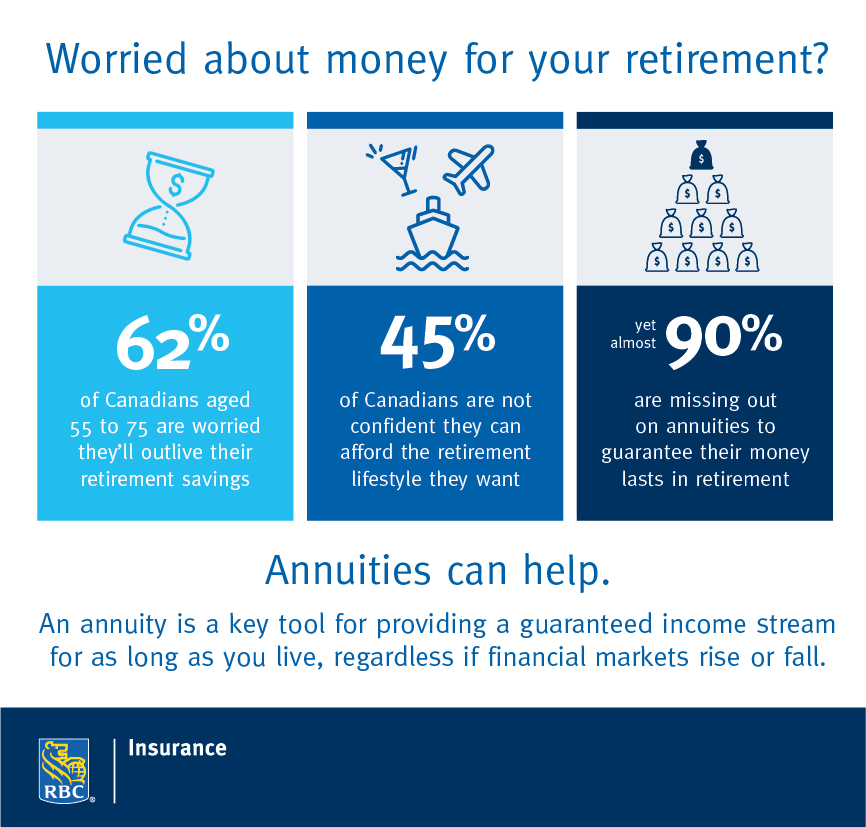

The reason why retirement planning is so difficult is because the one variable we need to know – how long we have to live – is impossible to predict. Sure, we have mortality tables and family history to help guide us, but statistically speaking, half the population will outlive their median life expectancy.

That makes longevity risk – the risk of running out of money before you die – a very real threat to your retirement. And yet many Canadians ignore this threat by not saving enough during their working years; retiring before they’re financially ready, taking Canada Pension Plan benefits too early, withdrawing too much from their RRSPs, and so on.

Nearly half of Canadians are worried they won’t have enough money to live a full lifestyle in retirement, according to a recent survey by RBC Insurance. They interviewed 1,000 Canadians aged 55 to 75 about their retirement readiness and came out with some interesting findings.

The retirees, or soon-to-be-retirees seem to want it all, according to the poll, yet many will lack the savings to do so:

80 per cent want to live at home for as long as they can

72 per cent said it’s important to own a car.

68 per cent said it’s important for them to be able to travel at least once a year

53 per cent want to go out for lunch or dinner a few times a week

Having enough money to support their desired lifestyle is a real concern, highlighted by the fact that 62 per cent of those surveyed are worried about outliving their retirement savings.

The one retirement income tool that didn’t appear on the radar was an annuity. Just 12 per cent said they are using or plan to use one in retirement.

How Annuities Can Help In Retirement

An annuity provides a predictable income stream for life – much like how a defined benefit pension, CPP, and OAS pays benefits for as long as you live. Nothing protects you from longevity risk quite like a guaranteed lifetime income.

It’s puzzling why more Canadians don’t choose to turn even a portion of their savings into an annuity – to pensionize their nest egg, to borrow a phrase coined by financial authors Moshe Milevsky and Alexandra Macqueen.

Lack of knowledge around annuities definitely plays a role. While nine in 10 Canadians polled by RBC know they don’t need to invest their entire retirement savings into an annuity, just 28 per cent know that an annuity doesn’t have to be managed once it has been purchased. Continue Reading…

Duke University conducted a two-year study of 218 healthy adults of normal weight to determine if a modest, sustained calorie reduction would show appreciable benefits. The plan was to reduce calories consumed by 25 per cent, but participants were unable to achieve that much.

Duke University conducted a two-year study of 218 healthy adults of normal weight to determine if a modest, sustained calorie reduction would show appreciable benefits. The plan was to reduce calories consumed by 25 per cent, but participants were unable to achieve that much. It’s a no brainer that poor dietary habits would exacerbate internal inflammation. But very often this is an invisible menace (see my article ‘The Truth About Inflammation’, October 2015). Most of us remain blissfully unaware of any chronic inflammation cascading throughout our bodies. Yet this exposes us to chronic health risks as a result of knocking the body out of whack. In my case, I had the aforesaid silent inflammation and observable inflammation, which I felt in my poor old joints. And I am pretty convinced that chronic inflammation was one factor in my developing cancer.

It’s a no brainer that poor dietary habits would exacerbate internal inflammation. But very often this is an invisible menace (see my article ‘The Truth About Inflammation’, October 2015). Most of us remain blissfully unaware of any chronic inflammation cascading throughout our bodies. Yet this exposes us to chronic health risks as a result of knocking the body out of whack. In my case, I had the aforesaid silent inflammation and observable inflammation, which I felt in my poor old joints. And I am pretty convinced that chronic inflammation was one factor in my developing cancer.